Motorola 2006 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2006 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

78

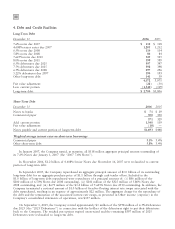

Motorola, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

(Dollars in millions, except as noted)

1. Summary of Significant Accounting Policies

Principles of Consolidation: The consolidated financial statements include the accounts of the Company and

all majority-owned subsidiaries. All intercompany transactions and balances have been eliminated. The Company's

investments in non-controlled entities in which it has the ability to exercise significant influence over operating and

financial policies are accounted for by the equity method. The Company's investments in other entities are

accounted for using the cost method.

Revenue Recognition: The Company recognizes revenue when persuasive evidence of an arrangement exists,

delivery has occurred, the sales price is fixed or determinable, and collectibility of the sales price is reasonably

assured. In addition to these general revenue recognition criteria, the following specific revenue recognition policies

are followed:

Products and Equipment Ì For product and equipment sales, delivery generally does not occur until the

products or equipment have been shipped, risk of loss has transferred to the customer, and objective evidence exists

that customer acceptance provisions have been met. The Company records revenue when allowances for discounts,

price protection, returns and customer incentives can be reliably estimated. Recorded revenues are reduced by these

allowances. The Company bases its estimates on historical experience taking into consideration the type of products

sold, the type of customer, and the type of transaction specific in each arrangement.

Long-Term Contracts Ì For long-term contracts that involve customization or modification of the Company's

equipment or software, the Company generally recognizes revenue using the percentage of completion method

based on the percentage of costs incurred to date compared to the total estimated costs to complete the contract.

In certain instances, when revenues or costs associated with long-term contracts cannot be reliably estimated or the

contract involves unproven technologies or other inherent hazards, revenues and costs are deferred until the project

is complete and customer acceptance is obtained.

Services Ì Revenue for services is generally recognized ratably over the contract term as services are

performed.

Software and Licenses Ì Revenue from pre-paid perpetual licenses is recognized at the inception of the

arrangement, presuming all other relevant revenue recognition criteria are met. Revenue from non-perpetual licenses

or term licenses is recognized ratably over the period that the licensee uses the license. Revenue from software

maintenance, technical support and unspecified upgrades is generally recognized over the period that these services

are delivered.

Multiple Element Arrangements Ì Arrangements with customers may include multiple deliverables, including

any combination of products, equipment, services and software. If multiple element arrangements include software

or software related elements, the Company applies the provisions of AICPA Statement of Position No. 97-2,

""Software Revenue Recognition,'' to determine separate units of accounting and the amount of the arrangement fee

to be allocated to those separate units of accounting. Multiple element arrangements that include software are

separated into more than one unit of accounting if the functionality of the delivered element(s) is not dependent

on the undelivered element(s), there is vendor-specific objective evidence of the fair value of the undelivered

element(s), and general revenue recognition criteria related to the delivered element(s) have been met. For all

other deliverables, elements are separated into more than one unit of accounting if the delivered element(s) have

value to the customer on a stand-alone basis, objective and reliable evidence of fair value exists for the undelivered

element(s), and delivery of the undelivered element(s) is probable and substantially in the control of the

Company. Revenue is allocated to each unit of accounting based on the relative fair value of each accounting unit

or using the residual method if objective evidence of fair value does not exist for the delivered element(s). The

revenue recognition criteria described above are applied to each separate unit of accounting. If these criteria are not

met, revenue is deferred until the criteria are met or the last element has been delivered.

Cash Equivalents: The Company considers all highly-liquid investments purchased with an original maturity of

three months or less to be cash equivalents.