Lifetime Fitness 2007 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2007 Lifetime Fitness annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

5

Our Growth Strategy

Our growth strategy is driven by three primary elements:

Open new centers.

We intend to expand our base of centers. In 2007, we opened ten centers, of which we designed and constructed

eight current model centers, we purchased an existing large format center and we assumed the operations of one

large format center. We expect to open eleven centers in 2008, ten of which are current model centers and one of

which is a large format center. One of these centers opened in January and the remaining ten are currently under

construction. We plan to open eleven current model centers in 2009. The new centers we plan to open in 2008 and

2009 will be built in both new and existing markets.

Increase membership and optimize membership dues.

Of our 70 open centers at December 31, 2007, 32 had not yet reached maturity, which we define as the 37th month of

operations. These 32 centers averaged 66% of targeted membership capacity as of December 31, 2007. We expect

the continuing increase in memberships at these centers to contribute significantly to our future growth as these

centers move toward our goal of 90% of targeted membership capacity by the end of their third year of operations.

We also plan to continue to drive membership growth at mature centers that are not yet at targeted capacity.

In addition to increasing membership levels, we focus on optimizing our membership dues by offering four different

types of centers and membership types: Bronze, Gold, Platinum and Onyx, which are based on center amenities,

services, location and capacity. Each membership type offers a distinctive pricing level, single, couple and family

types and associated center access and membership privileges, along with affinity partner benefits outside of our

centers. In order to achieve these goals, we focus on demographics, center usage and membership trends, and

employ marketing programs to effectively communicate our value proposition to existing and prospective members.

Increase in-center products and services revenue.

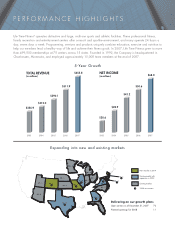

From 2003 to 2007, revenue from the sale of in-center products and services grew from $55.6 million to $182.2

million (34.5% compound annual growth rate) and we increased in-center revenue per membership from $242 to

$387. We believe the revenue from sales of our in-center products and services will continue to grow at a faster rate

than membership dues or enrollment fees. Our centers offer a variety of in-center programs, products and services,

including individual and group sessions with certified professional personal trainers and registered dieticians,

LifeSpa services, member activities programs, wellness programs, Pilates and yoga, tennis programs and healthy

food at our quick-service LifeCafe restaurant. We expect to continue to drive in-center revenue by increasing sales

of our current in-center products and services and introducing new products and services to our members.

Our Industry

We participate in the large and growing U.S. health and wellness industry, which we define to include health and

fitness centers, fitness equipment, athletics, physical therapy, wellness education, nutritional products, athletic

apparel, spa services and other wellness-related activities. According to International Health, Racquet & Sportclub

Association (“IHRSA”), the estimated market size of the U.S. health club industry, which is a relatively small part

of the health and wellness industry, was approximately $17.6 billion in revenues for 2006 and 42.7 million

memberships with approximately 29,000 clubs as of January 2007. Based on IHRSA membership data, the

percentage of the total U.S. population with health club memberships increased from 14.1% in 2002 to 16.0% in

2006. Over this same period, total U.S. health club industry revenues increased from $13.1 billion to $17.6 billion.