KeyBank 2008 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2008 KeyBank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

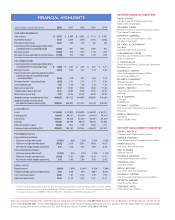

interest on the disputed tax balances.

Also impacting financial results in 2008 were significant

increases in our loan loss provisions during the year, reflect-

ing the difficult operating environment. At December 31, our

allowance for loan losses stood at $1.803 billion, representing

2.36 percent of total loans. Finally, in the fourth quarter, we

reported an after-tax noncash accounting charge of $420

million to mark down the goodwill value of our National

Banking unit due to unfavorable market conditions.

Were there management decisions made by Key in the

run-up to the economic crisis that are now a source of

regret? What might have been done differently?

While we curtailed our condominium lending more than

two years ago, we regret that we didn’t foresee earlier the

swift and dramatic impact of the downturn on our home-

builder loan portfolio, and our balance sheet was hurt by that.

While we didn’t foresee the severity of the downturn, we did

move aggressively to build reserves and sell a significant

portfolio of nonperforming loans. As mentioned earlier, we

made substantial progress on that front in 2008.

So, if you were asked to broadly describe Key’s actions and

your communications to investors, clients and employees

concerning strength and confidence in Key’s future, how

would you respond?

We have fortified Key for tough times in four critical areas:

We’ve raised capital so that we can operate from a solid

position of strength; increased loan loss reserves to deal with

a continuing slowdown in the credit markets; reduced our

dividend payout to further conserve capital; and taken steps

to closely manage expenses and deploy our capital efficiently

by exiting certain lending categories and focusing on those

with more predictable returns.

In addition to those measures, we continue to invest in core

banking and deposit-gathering businesses. We are fortunate

to be a long-standing, multi-regional bank with strong rela-

tionships with individuals and small and midsize businesses

in four regions of the country, and a branch network that was

in position to capitalize on disruptions among competitors in

several parts of the country.

Henry, on the subject of the dividend, you have pointed

out that reducing it was among the tough and necessary

decisions made last year. Would you provide your perspec-

tive on the dividend cuts?

Cutting our dividend, particularly in light of the long history

of dividend increases we had established, was a very difficult

decision for the Board and me. We realize that our dividend

payout made our stock attractive for some investors. However,

along with our other steps to buttress capital in 2008, we

believed these actions were required under the conditions we

faced, and continue to encounter.

A company’s dividend is the most accessible and least ex-

pensive source of capital, so to ignore this alternative while

taking the other steps we believed necessary would not have

been good business judgment. Maintaining a high dividend

payout when earnings are reduced is costly, as well.

MANAGING CAPITAL EFFECTIVELY

You noted that Key bolstered its capital position twice

during 2008. Could you elaborate on the balance sheet

significance of these infusions of capital?

In times such as these, our most important strategic advan-

(left to right) Peter Hancock, Vice Chair, National Banking; Thomas E. Helfrich, Chief Human Resources Officer; Beth E. Mooney, Vice Chair,

Community Banking; Henry L. Meyer III, Chairman and CEO; and Charles S. Hyle, Chief Risk Officer.

Key 2008 • 5