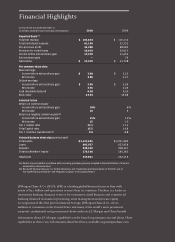

JP Morgan Chase 2010 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2010 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

|

|

10

• Globalgrossdomesticproductisexpected

to grow by approximately $50 trillion in

nominal terms ($25 trillion in real 2010

dollar-valueterms)overthenext10years,

an approximately 80% increase.

• Annualcorporateinvestmentsinplantand

equipment (globally running at approxi-

mately$8trillionayear)shouldatleast

double over the next 10 years – our multi-

national clients account for approximately

50% of this.

Eectivelydeliveringonthisgrowing

demand requires strong, healthy financial

institutions. This bodes well for JPMorgan

Chase – we are in exactly the right place.

What will not change: Banks will continue to need

to earn adequate market-demanded returns on

capital

Like all businesses, banks must continue

to earn adequate returns on capital – inves-

tors demand it. Some argue, however, that if

regulation results in better capitalized banks

and a more stable financial system, returns

demanded on capital would be lower to reflect

the lower risk involved. This probably is true

but not likely to be materially significant.

What will change: New regulation will aect prod-

ucts and their pricing

A likely outcome of the new regulations is

that products and their pricing will change.

Some products will go away, some will be

redesigned and some will be repriced.

Last year, we spoke about how we would

adjust our products and services for the new

credit card pricing rules and new overdraft

rules. So I will not repeat them here. In a

later section, I will talk about how we will

adjust to the new restrictions on the pricing

of debit cards.

Highercapitalandliquiditystandardsthat

are required under Basel III likely will aect

the pricing of many products and services.

Two examples come to mind:

Current Basel III rules require banks to hold

more capital and maintain more liquidity to

support the revolving credit they provide to

both middle market and large institutions. In

some cases, the liquidity rules alone require

us to hold 100% of highly liquid assets to

support a revolver. For example, to support a

$100 million revolver, we would be required

to own $100 million of highly liquid securi-

tieswithveryshortmaturities.Weestimate

this would increase our incremental cost on

a three-year revolver by approximately 60

basis points a year. That leaves us with three

options:1)passthecostontothecustomer,

2)losemoneyonthatrevolver,or3)not

make the loan. In the real world, the likely

outcome is that some borrowers will have

less or no access to credit, some borrowers

will pay a lot more for credit, some would

pay only a little bit more and some highly

rated companies might find it cheaper to

provide liquidity on their own, i.e., hold

more excess cash on their balance sheet

as opposed to relying on banks for credit

liquidity backup.

Certain products may disappear completely

because they simply are too expensive to

provide.(Some,likethe“CDO-squares”will

notbemissed.)Forexample,capitalcharges

on certain securitizations will be so high

for banks that either these transactions no

longer will be done or they will migrate to

other credit intermediaries (think hedge

funds)thatcanmorecheaplyinvestinthem.

I will have more to say on regulation in the

fourth section of this letter.

What we don’t know (and we have a healthy fear

of unintended consequences)

Around the world and all at once, policy-

makers and regulators are making countless

changes, from guidelines around market-

making, derivatives rules, capital and liquidity

standards, and more. Many of the rules have

yet to be defined in detail, and it is likely

that they will not be applied evenly around

the world. The combined impact of so much

change – so much unknown about the inter-

play among all these factors and an uneven