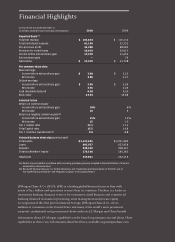

JP Morgan Chase 2010 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2010 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

|

|

8

been focusing on recently. Consumers are

getting stronger, spending at levels similar to

those two-and-a-half years ago, but, instead of

spending more than their income, they now

are saving 5% of their income. And consumer

debt service costs, i.e., how much they spend

of their income to service their debt, have

returned to levels seen in the 1990s (due to

debt repayment, charge-os and debt forgive-

ness,lowerinterestrates,etc.).

Businesses, large and small, are getting

stronger. Large companies have plenty of

cash. Medium sized and small businesses are

in better financial condition and are starting

to borrow again. Global trade is growing –

U.S.exportswereup16%in2010.Jobgrowth

seems to have begun. Financial markets are

wide open – and banks are lending more

freely.U.S.businesses,largeandsmall,are

investing more than $2 trillion a year in

capital expenditures and research and devel-

opment. They have the ability to do more,

and, at the end of the day, the growth in the

economy ultimately is driven by increased

capital investment.

The biggest negative that people point

to is that home prices are continuing to

decline, new home sales are at record lows

and foreclosures are on the rise. Our data

indicates that the rate of foreclosures will

start to come down later this year. Approxi-

mately 30% of the homes in America do

not have mortgages – and of those that do,

approximately 90% of mortgage-holding

homeowners are paying their loans on time.

Housingaordabilityisatanall-timehigh.

TheU.S.populationisgrowingatover3

million a year, and those people eventually

will need housing. Additionally, the fact

that fewer homes are being built means that

supply and demand will come into balance

sooner than it otherwise would have. That

said, housing prices likely will continue to

go down modestly because of the contin-

uous high levels of homes for sale. The ulti-

mate recovery of the housing market and

housing prices likely will follow job growth

and a general recovery in the economy.

Yes, America still is facing headwinds and

uncertainties – including abnormal monetary

policy and looming fiscal deficits. And while

we can’t really predict what the economy will

do in the next year or two (though we think

itisgettingstronger),wearecondentthat

the world’s greatest economy will regain its

footing and grow over the ensuing decade.

But we must take serious action to ensure our

success in the decades ahead

Whileourcondenceinthenextdecade

is high, for America to thrive after that,

it soon must confront some of the serious

issuesfacingit.Weneedtoredoubleour

eorts to develop an immigration policy

and a real, sustainable energy policy;

protect our environment; improve our

education and health systems; rebuild

our infrastructure for the future; and find

solutions for our still-unbalanced trade

and capital flows.

The sooner we address these issues, the

better – America does not have a divine

right to success, and it can’t rely on wishful

thinking and its great heritage alone to

get the country where it needs to go. But

I remain, perhaps naively, optimistic. As

WinstonChurchilloncesaid,“Youcan

always count on Americans to do the right

thing – after they’ve tried everything else.”

Will the Role of Banks Change in This New

Environment?

Banks serve a critical function in society,

but it often is dicult to describe that func-

tioninbasicterms.WhenIwastravelingin

Ghana with one of our daughters (yes, the

same daughter who asked me what a finan-

cialcrisiswasthreeyearsago),shepointed

out all the buildings and projects that had

been started but never finished.

All the money that went into Ghana’s

unfinished buildings was needlessly wasted

and, in fact, had damaged the citizens of

the country. This sorry sight provided me

with a concrete example of how to describe

what banks actually should do. I explained

to our daughter that had banks (or inves-

tors)beendoingtheirjob,theywouldhave

made sure that before money was invested

in a project or enterprise, it had good pros-

pects of success: It would be built for good