IBM 2006 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2006 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

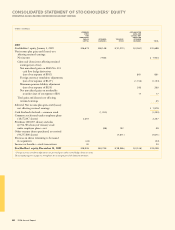

Liquidity and Capital Resources

Global Financing is a segment of the company and as such, is supported

by the company’s liquidity position and access to capital markets.

Cash generated from operations in 2006 was deployed to reduce

intercompany payables and pay dividends to the company in order to

maintain an appropriate debt-to-equity ratio.

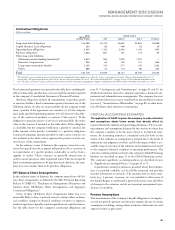

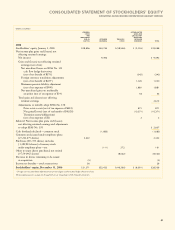

RETURN ON EQUITY

(Dollars in millions)

AT DECEMBER 31: 2006 2005

Numerator:

Global Financing after tax income(a)* $ $,

Denominator:

Average Global Financing equity(b)** $, $,

Global Financing Return on Equity(a)/(b) .% .%

* Calculated based upon an estimated tax rate principally based on Global

Financing’s geographic mix of earnings as IBM’s provision for income taxes is

determined on a consolidated basis.

** Average of the ending equity for Global Financing for the last five quarters.

CRITICAL ACCOUNTING ESTIMATES

As discussed in the section, “Critical Accounting Estimates,” on

pages 45 to 47, the application of GAAP requires the company to

make estimates and assumptions about future events that directly

affect its reported financial condition and operating performance.

The accounting estimates and assumptions discussed in this section

are those that the company considers to be the most critical to Global

Financing. The company’s significant accounting policies are described

in note A, “Significant Accounting Policies,” on pages 62 to 71.

Financing Receivables Reserves

Global Financing reviews its financing receivables portfolio at least

quarterly in order to assess collectibility. A description of the meth-

ods used by management to estimate the amount of uncollectible

receivables is included on page 70. Factors that could result in actual

receivable losses that are materially different from the estimated

reserve include sharp changes in the economy or a significant change

in the economic health of a particular industry segment that repre-

sents a concentration in Global Financing’s receivables portfolio.

To the extent that actual collectibility differs from management’s

estimates by 5 percent, Global Financing after-tax income would be

higher or lower by an estimated $12 million (using 2006 data),

depending upon whether the actual collectibility was better or worse,

respectively, than the estimates.

Residual Value

Residual value represents the estimated fair value of equipment under

lease as of the end of the lease. Residual value estimates impact the

determination of whether a lease is classified as operating or sales type.

Global Financing estimates the future fair value of leased equipment

by using historical models, analyzing the current market for new and

used equipment and obtaining forward-looking product information

such as marketing plans and technological innovations. Residual value

estimates are periodically reviewed and “other than temporary”

declines in estimated future residual values are recognized upon

identification. Anticipated increases in future residual values are not

recognized until the equipment is remarketed. Factors that could

cause actual results to materially differ from the estimates include

severe changes in the used-equipment market brought on by unfore-

seen changes in technology innovations and any resulting changes in

the useful lives of used equipment.

To the extent that actual residual value recovery is lower than

management’s estimates by 5 percent, Global Financing’s after-tax

income would be lower by an estimated $19 million (using 2006 data).

If the actual residual value recovery is higher than management’s

estimates, the increase in after-tax income will be realized at the end

of lease when the equipment is remarketed.

MARKET RISK

See pages 47 and 48 for discussion of the company’s overall

market risk.

LOOKING FORWARD

Given Global Financing’s primary mission of supporting IBM’s

hardware, software and services businesses, originations for both

client and commercial financing businesses will be dependent upon

the overall demand for IT hardware, software and services, as well as

client participation rates.

As a result of the company divesting its Personal Computing

business to Lenovo, Global Financing is supporting Lenovo’s per-

sonal computer business through an exclusive, five-year agreement

covering all Global Financing lines of business effective since May 1,

2005. These participations with Lenovo are external revenue to

Global Financing.

Interest rates and the overall economy (including currency fluc-

tuations) will have an effect on both revenue and gross profit. The

company’s interest rate risk management policy, however, combined

with the Global Financing funding strategy (see page 52), should

mitigate gross margin erosion due to changes in interest rates. The

company’s policy of matching asset and liability positions in foreign

currencies will limit the impacts of currency fluctuations.

The economy could impact the credit quality of the Global

Financing receivables portfolio and therefore the level of provision

for bad debts. Global Financing will continue to apply rigorous credit

policies in both the origination of new business and the evaluation of

the existing portfolio.

As discussed previously, Global Financing has historically been able

to manage residual value risk both through insight into the product

cycles, as well as through its remarketing business.

Global Financing has policies in place to manage each of the key

risks involved in financing. These policies, combined with product

and client knowledge, should allow for the prudent management of

the business going forward, even during periods of uncertainty with

respect to the economy.

MANAGEMENT DISCUSSION

INTERNATIONAL BUSINESS MACHINES CORPORATION AND SUBSIDIARY COMPANIES

53

Black

MAC

2718 CG10