Health Net 2014 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2014 Health Net annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

|

|

3

In addition, we believe that economic pressures have caused customers (both individuals and employer groups)

increasingly to make health insurance purchasing decisions based on “value versus choice.” We believe that many

customers are choosing health plans that offer better financial value over health plans that may offer broader networks

that require higher premiums. We have developed and are selling products using tailored networks to meet this need.

These tailored network products use dedicated provider networks that share our commitment to quality health care and

affordability. These products also incorporate benefit levels that help ensure our members have access to the care they

need.

We offer tailored network HMO, EPO or HSP products throughout our Western Region Operations segment.

These products are structured in a variety of ways. They may include a tiered provider option, be organized in

conjunction with a strategic provider partner or be created specifically for particular populations and geographically

proximate networks. For example, our HMO CommunityCareSM product offers a network of HMO doctors, specialists

and hospitals designed to meet the unique needs of the individual exchange markets. Our Salud Con Health NetSM

product line is a suite of affordable plans developed for the Latino community. In addition, we have developed tailored

network products with strategic provider partners in California, Arizona, Oregon and Washington, and we have

developed customized products for large employer groups with a large geographic distribution within a particular state.

We believe our strength in tailored network products has been an important factor in the enrollment growth that we

experienced in 2014 in both our on-exchange and off-exchange HMO, EPO or HSP plans that utilize tailored networks.

We assume both underwriting and administrative expense risk in return for the premium revenue we receive from

our HMO, POS, PPO/EOA and HSP products. In California, under a capitation payment model, we pay a provider

group a fixed amount per member on a regular basis, usually monthly, and the provider group accepts the risk of the

frequency and cost of member utilization of professional services. We believe that capitation payment models

incentivize providers to focus more on preventive care and cost management. Under these payment models, we believe

members are more likely to receive a comprehensive array of appropriate and timely preventive services than in fee-

for-service models, thereby helping to improve members’ health, reduce the need for more costly acute care

interventions and, in so doing, lower the rate of growth of health care costs. With its focus on improving patient care

through shared risk amongst providers and health insurers, the capitation payment model shares certain similarities with

the Accountable Care Organization (“ACO”) model that is one of the ACA’s primary initiatives for improving the

quality and efficiency of health care delivery systems. See “—Provider Relationships” for additional information about

our capitation fee arrangements and “Item 1A. Risk Factors-If we fail to develop and maintain satisfactory relationships

on competitive terms with the hospitals, provider groups and other providers that provide services to our members, our

profitability could be adversely affected” for additional information on the challenges we face with providers in the

changing health care environment. As of December 31, 2014, approximately 67% of our California commercial

membership was enrolled in capitated medical groups. In addition, approximately 70% of our Medicare, 73% of our

Medicaid and all of our dual eligibles businesses are linked to capitated provider groups.

As of December 31, 2014, 63% of our commercial members in our Western Region Operations segment were

covered by conventional HMO products, 34% were covered by POS and PPO products, and 3% were covered by other

related products.

Membership in our tailored network products was approximately 50% of total commercial membership as of

December 31, 2014, compared with 38% as of December 31, 2013. As of December 31, 2014, approximately 64% of

our California commercial capitated membership was enrolled in tailored network products.

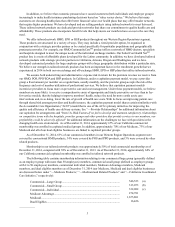

The following table contains membership information relating to our commercial large group (generally defined

as an employer group with more than 50 employees) members, commercial small group (defined as employer groups

with 2 to 50 employees) members, commercial individual members, Medicare Advantage members, Medicaid

members, and dual eligibles members as of December 31, 2014 (our Medicare, Medicaid and dual eligibles businesses

are discussed below under “—Medicare Products,” “—Medicaid and Related Products” and “—California Coordinated

Care Initiative," respectively):

Commercial—Large Group................................................................................. 546,523 (a)

Commercial—Small Group................................................................................. 313,073 (b)

Commercial—Individual..................................................................................... 332,082 (c)

Medicare Advantage............................................................................................ 274,781

Medicaid.............................................................................................................. 1,675,801

Dual Eligibles...................................................................................................... 16,426

___________