Harley Davidson 2012 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2012 Harley Davidson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

77

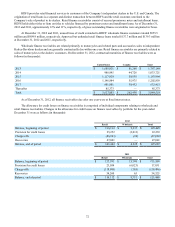

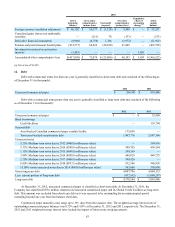

Conduit also provides for an unused commitment fee based on the unused portion of the total aggregate commitment of

$600.0 million. There is no amortization schedule; however, the debt is reduced monthly as available collections on the

related finance receivables are applied to outstanding principal. Upon expiration of the U.S. Conduit, any outstanding

principal will continue to be reduced monthly through available collections. Unless earlier terminated or extended by

mutual agreement of HDFS and the lenders, the U.S. Conduit has an expiration date of September 13, 2013.

The SPE had no borrowings outstanding under the U.S. Conduit at December 31, 2012 or 2011; therefore, these

assets are restricted as collateral for the payment of fees associated with the unused portion of the total aggregate

commitment of $600.0 million.

For the years ended December 31, 2012 and 2011, the SPE recorded interest expense of $1.4 million and $1.5

million, respectively, related to the unused portion of the total aggregate commitment of $600.0 million. Interest

expense on the U.S. Conduit is included in financial services interest expense. There was no weighted average interest

rate at December 31, 2012 or 2011 as HDFS had no outstanding borrowings under the U.S. Conduit during 2012 or

2011.

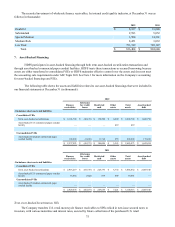

Asset-Backed Canadian Commercial Paper Conduit Facility

In 2012, HDFS entered into an agreement with a Canadian bank-sponsored asset-backed commercial paper

conduit facility (Canadian Conduit). Under the agreement, the Canadian Conduit is contractually committed, at HDFS'

option, to purchase from HDFS eligible Canadian retail motorcycle finance receivables for proceeds up to C$200

million. The terms for this debt provide for interest on the outstanding principal based on prevailing market interest

rates plus a specified margin. The Canadian Conduit also provides for a program fee and an unused commitment fee

based on the unused portion of the total aggregate commitment of C$200 million. There is no amortization schedule;

however, the debt is reduced monthly as available collections on the related finance receivables are applied to

outstanding principal. Upon expiration of the Canadian Conduit, any outstanding principal will continue to be reduced

monthly through available collections. Unless earlier terminated or extended by mutual agreement of HDFS and the

lenders, the Canadian Conduit expires on August 30, 2013. The contractual maturity of the debt is approximately 5

years.

During 2012, HDFS transferred $230.0 million of Canadian retail motorcycle finance receivables for proceeds of

$201.3 million This transaction is treated as a secured borrowing, and the transferred assets are restricted as collateral

for payment of the debt.

For the year ended December 31, 2012, HDFS recorded interest expense of $1.1 million on the secured notes.

Interest expense on the Canadian Conduit is included in financial services interest expense. The weighted average

interest rate of the outstanding Canadian Conduit was 1.95% at December 31, 2012.

As HDFS participates in and does not consolidate the Canadian bank-sponsored, multi-seller conduit VIE, the

maximum exposure to loss associated with this VIE, which would only be incurred in the unlikely event that all the

finance receivables and underlying collateral have no residual value, is $27.2 million at December 31, 2012. The

maximum exposure is not an indication of the Company's expected loss exposure.

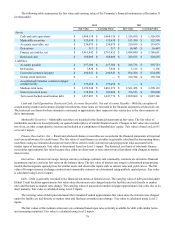

8. Fair Value Measurements

Certain assets and liabilities are recorded at fair value in the financial statements; some of these are measured on a

recurring basis while others are measured on a non-recurring basis. Assets and liabilities measured on a recurring basis are

those that are adjusted to fair value each time a financial statement is prepared. Assets and liabilities measured on a non-

recurring basis are those that are adjusted to fair value when a significant event occurs. In determining fair value of assets and

liabilities, the Company uses various valuation techniques. The availability of inputs observable in the market varies from

instrument to instrument and depends on a variety of factors including the type of instrument, whether the instrument is

actively traded, and other characteristics particular to the transaction. For many financial instruments, pricing inputs are readily

observable in the market, the valuation methodology used is widely accepted by market participants, and the valuation does not

require significant management discretion. For other financial instruments, pricing inputs are less observable in the market and

may require management judgment.

The Company assesses the inputs used to measure fair value using a three-tier hierarchy. The hierarchy indicates the

extent to which inputs used in measuring fair value are observable in the market. Level 1 inputs include quoted prices for

identical instruments and are the most observable.