Freddie Mac 2008 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2008 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

|

|

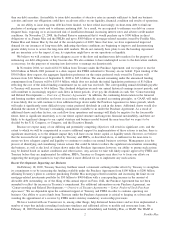

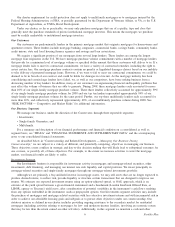

The following diagram illustrates how we create PCs through mortgage securitizations that can be sold to investors or

held by us to provide liquidity to the mortgage market:

Cash

Mortgage

Homeowners Our Customers:

Originate Loans with

Homeowners

Sell or Exchange

Mortgages for PCs or Cash

Invest in PCs or Sell

to Investors

Investors

Freddie Mac:

Guarantees PCs

Retains Investments

in PCs and Mortgages

Sells PCs to

Investors

Cash

PC

PC or Cash

Mortgage

PC

Mortgage

PC Trusts

Mortgage Securitizations

Cash

PC

We guarantee the payment of principal and interest of PCs created in this process in exchange for a combination of

monthly management and guarantee fees and initial upfront cash payments referred to as delivery fees. Our guarantee

increases the marketability of the PCs, providing liquidity to the mortgage market. Various other participants also play

significant roles in the residential mortgage market. Mortgage brokers advise prospective borrowers about mortgage products

and lending rates, and they connect borrowers with lenders. Mortgage servicers administer mortgage loans by collecting

payments of principal and interest from borrowers as well as amounts related to property taxes and insurance. They remit the

principal and interest payments to us, less a servicing fee, and we pass these payments through to mortgage investors, less a

fee we charge to provide our guarantee (i.e., the management and guarantee fee). In addition, private mortgage insurance

companies and other financial institutions sometimes provide third-party insurance for mortgage loans or pools of loans. Our

charter generally requires third-party insurance or other credit protections on some loans that we purchase. Most mortgage

insurers increased premiums and tightened underwriting standards during 2008. These actions may impair our ability to

purchase loans made to borrowers who do not make a down payment at least equal to 20% of the value of the property at

the time of loan origination.

Our charter generally prohibits us from purchasing first-lien conventional (not guaranteed or insured by any agency or

instrumentality of the U.S. government) single-family mortgages if the outstanding principal balance at the time of purchase

exceeds 80% of the value of the property securing the mortgage unless we have one of the following credit protections:

• mortgage insurance from a mortgage insurer that we determine is qualified on the portion of the outstanding principal

balance above 80%;

• a seller’s agreement to repurchase or replace (for periods and under conditions as we may determine) any mortgage

that has defaulted; or

• retention by the seller of at least a 10% participation interest in the mortgages.

In addition, on February 18, 2009, the Obama Administration announced the HASP, which includes an initiative

pursuant to which FHFA allowed mortgages currently owned or guaranteed by us to be refinanced without obtaining

additional credit enhancement in excess of that already in place for that loan. For more information, see “Conservatorship

and Related Developments — Homeownership Affordability and Stability Plan.”

5Freddie Mac