Fifth Third Bank 2007 Annual Report Download

Download and view the complete annual report

Please find the complete 2007 Fifth Third Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

Building on the past to

future

1 8 5 8 —200 8

www.53.com

Table of contents

-

Page 1

future 1 8 5 8 - 2 0 0 8 sHaPE tHE Building on the past to 2 0 07 a n n ua l R E P O R t -

Page 2

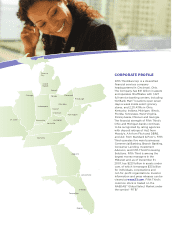

...The Company has $111 billion in assets and operates 18 affi liates with 1,227 full-service banking centers, including 102 Bank Mart locations open seven days a week inside select grocery stores, and 2,211 ATMs in Ohio, Kentucky, Indiana, Michigan, Illinois, Florida, Tennessee, West Virginia... -

Page 3

...10 1 - actuals Common Shares Outstanding Banking Centers Full-Time Equivalent Employees 532,672 1,227 21,683 556,253 1,150 21,362 (4) 7 2 Deposit and Debt Ratings Fifth third Bancorp Commercial Paper Senior Debt Moody's standard & Poor's Fitch... -

Page 4

... a significant presence. Investor concerns related to rising loan defaults in subprime lending and other areas related to real estate led to significant decreases in the market valuation of virtually every major U.S. bank. Fifth Third's total return in 2007 - the change in our stock price plus... -

Page 5

... one of our Bank-Owned Life Insurance (BOLI) policies, to reflect losses experienced on the underlying investments due to significant disruptions in the financial markets. Additionally, Fifth Third and a number of other banks were required to accrue expenses related to current and future legal... -

Page 6

...415 million in losses related to fourth quarter balance sheet actions. Otherwise, noninterest income increased 9 percent from 2006. We continued to see strong growth in our electronic payments processing revenue, which increased 15 percent to $826 million in 2007. Corporate banking revenue also... -

Page 7

...Orlando. First Charter, the fourth largest bank by deposits in the Charlotte, North Carolina market, offered us a sizeable entry point into this rapidly growing state, while also giving us a small presence in Atlanta. Once this transaction closes, Fifth Third will have strong positions in both... -

Page 8

.... Our new Fifth Third Goal-Setter Savings account allows customers to target a dollar amount and specific date for reaching their target, simplifying their day-to-day money management. In addition, we sold 58,000 stored value cards after introducing gift card centers into our branch network... -

Page 9

... valuable to Fifth Third, as they are twice as likely to stay with us over the long term, hold higher account balances, and purchase more products and services. We're working to increase customer loyalty in a number of ways. In 2007, we significantly improved our sales and service strategy... -

Page 10

.... This has enormous implications for the organic growth prospects of our Company in the future and, when coupled with our expertise at opening new banking centers, offers a lot of opportunity. We use sophisticated software programs that enable us to pinpoint locations 8 | FiFtH tHiRD BancORP -

Page 11

... banking centers have a targeted internal rate of return in excess of 20 percent, which produces a strong return on capital. We continue to refine and improve this process, as we believe that our ability to generate organic growth is vital to our Company's future. Our current plan is to build... -

Page 12

... to Fifth Third's success. Overlaying the affiliate structure are our lines of business. These are essentially areas of expertise - Branch Banking, Consumer Lending, Commercial Banking, Processing Solutions, and Investment Advisors - whose products and services are delivered to customers... -

Page 13

... saving for a home, a child's education, planning for retirement or building a business, our associates consult with our customers, help determine their needs, and provide solutions that meet their goals both today and tomorrow. strategy • Fifth Third opened 66 new banking centers in 2007... -

Page 14

... dealers who originate loans and leases on the Bank's behalf, otherwise known as Indirect Lending. Additionally, Consumer Lending provides loan products to individuals, including real estate-secured mortgages and home equity loans and lines, as well as federal and private student education... -

Page 15

...build and manage their wealth, Fifth Third Investment Advisors provides integrated solutions to meet the financial goals of individuals, families and institutional investors. Investment Advisors provides wealth planning, banking services, customized lending, asset management, trust, insurance... -

Page 16

... offerings, our products and services include global cash management, foreign exchange and international trade finance, derivatives and capital markets services, assetbased lending, real estate finance, public finance, commercial leasing and syndicated finance. customer Focus • Fifth Third... -

Page 17

... to customer Focus • Fifth Third Processing demonstrate exceptional value by Solutions operates three primary leveraging our in-house expertise and businesses - Merchant Services, Financial working with clients to help them Institution Services and Card Services. efficiently manage their... -

Page 18

... services. The Foundation funded 17 college scholarships of $2,500 each to children of Fifth Third Bank employees and matched more than $118,400 in employees' personal gifts to institutions of higher education. Fifth Third's Community Development Corporation (CDC) invests in lowincome housing... -

Page 19

...and Reporting Policies Business Combinations Securities Loans and Leases and Allowance for Loan and Lease Losses Loans Acquired in a Transfer Bank Premises and Equipment Goodwill Intangible Assets Sales of Receivables and Servicing Rights Derivatives Other Assets Short-Term Borrowings Long-Term Debt... -

Page 20

... other real estate owned Average Balances Loans and leases, including held for sale Total securities and other short-term investments Total assets Transaction deposits (b) Core deposits (c) Wholesale funding (d) Shareholders' equity Regulatory Capital Ratios Tier I capital Total risk-based capital... -

Page 21

...227 full-service Banking Centers including 102 Bank Mart® locations open seven days a week inside select grocery stores and 2,211 Jeanie® ATMs in Ohio, Kentucky, Indiana, Michigan, Illinois, Florida, Tennessee, West Virginia, Pennsylvania, Missouri and Georgia. The Bancorp reports on five business... -

Page 22

... banking center network. During 2007, the Bancorp opened 77 additional banking centers. In 2008, banking center expansion will be focused in high growth markets, such as Florida, Chicago, Tennessee, Georgia and North Carolina. RECENT ACCOUNTING STANDARDS In July 2006, the Financial Accounting... -

Page 23

... to Consolidated Financial Statements. Valuation of Securities Securities are classified as held-to-maturity, available-for-sale or trading on the date of purchase. Only those securities classified as held-to-maturity are reported at amortized cost. Available-for-sale and trading securities are... -

Page 24

... portion of Fifth Third's residential mortgage and commercial real estate loan portfolios are comprised of borrowers in Michigan, Northern Ohio and Florida, which markets have been particularly adversely affected by job losses, declines in real estate value, declines in home sale volumes, and... -

Page 25

... cash flows and funding costs. allowance, nor that it will not recognize a significant provision for impairment of its mortgage servicing rights. If Fifth Third's allowance for loan and lease losses is not adequate, Fifth Third's business, financial condition, including its liquidity and capital... -

Page 26

... risk of fraud or theft by employees, customers or outsiders, unauthorized transactions by employees or operational errors. Negative public opinion can result from Fifth Third's actual or alleged conduct in activities, such as lending practices, data security, corporate governance and acquisitions... -

Page 27

... on debt securities, loans and leases (including yield-related fees) and other interest-earning assets less the interest paid for core deposits (which includes transaction deposits plus other time deposits) and wholesale funding (which includes certificates $100,000 and over, other foreign office... -

Page 28

... accounts, such as savings and time deposits. During 2007, interest checking accounts comprised 31% of interest-bearing core deposits compared to 36% during 2006. During the third quarter of 2007, the Bancorp reclassified certain foreign office deposits as transaction deposits. The interest rates... -

Page 29

...due to real estate price deterioration in some the Bancorp's key lending markets, the increase in automobile loans and credit card balances and a modest decline in economic conditions. As of December 31, 2007, the allowance for loan and lease losses as a percent of loans and leases increased to 1.17... -

Page 30

...financial services to large and middle-market businesses and continues to further seek opportunities to expand its product offerings. Mortgage banking net revenue decreased to $133 million in Fifth Third Funds investments are: NOT INSURED BY THE FDIC or any other government agency, are not deposits... -

Page 31

...31 2007 2006 ($ in millions) Bank owned life insurance $(106) 86 Cardholder fees 56 49 Consumer loan and lease fees 46 47 Insurance income 32 28 Operating lease income 32 26 Banking center fees 29 22 Gain on loan sales 25 17 Other 39 24 Total other noninterest income $153 299 Mortgage net servicing... -

Page 32

... through de novo growth with plans to open approximately 50 new banking centers in 2008, in addition to 57 new banking centers as a result of the pending acquisition with First Charter. Payment processing expense includes third-party processing expenses, card management fees and other bankcard... -

Page 33

... mortgage loans in parts of its footprint, specifically eastern Michigan and northeastern Ohio. Fifth Third Bancorp 31 For the years ended December 31 ($ in millions) Income Statement Data Commercial Banking Branch Banking Consumer Lending Investment Advisors Processing Solutions General Corporate... -

Page 34

... a full range of deposit and loan and lease products to individuals and small businesses through 1,227 full-service banking centers. Branch Banking offers depository and loan products, such as checking and savings accounts, home equity loans and lines of credit, credit cards and loans for TABLE 14... -

Page 35

.... Net charge-offs increased to 73 bp in 2007, an increase from 47 bp in 2006, due to greater severity of loss on residential mortgages and automobile loans related to declining real estate prices and a market surplus of used automobiles, respectively. The segment is focusing on managing credit risk... -

Page 36

...Fifth Third Processing Solutions provides electronic funds transfer, debit, credit and merchant transaction processing, operates the Jeanie® ATM network and provides other data processing services to affiliated and unaffiliated customers. Table 18 contains selected financial data for the Processing... -

Page 37

... lower earnings credits on commercial deposit accounts and fee growth associated with new product and service offerings. Investment advisory revenue of $94 million decreased one percent sequentially and increased four percent over fourth quarter of 2006. Private banking revenue increased two percent... -

Page 38

... mortgage, automobile and credit card balances mitigated by a decline in home equity loans and consumer automobile leases. The Bancorp experienced its largest growth in the Chicago affiliate, an increase of $254 million, or nine percent. Additionally, the Bancorp saw growth of 11% in the Florida... -

Page 39

.... (d) Other securities consist of Federal Home Loan Bank ("FHLB") and Federal Reserve Bank restricted stock holdings that are carried at cost, Federal Home Loan Mortgage Corporation ("FHLMC") preferred stock holdings, certain mutual fund holdings and equity security holdings. Fifth Third Bancorp 37 -

Page 40

... competitive rates. At December 31, 2007, core deposits represented 59% of the Bancorp's asset funding base, compared to 62% at December 31, 2006. In 2007, the Bancorp expanded its deposit product line by offering an equity-linked certificate of deposit and a new savings account to help customers... -

Page 41

... risks and controls. These committees include the Market Risk Committee, the Corporate Credit Committee, the Credit Policy Committee, the Operational Risk Committee and the Executive Asset Liability Committee. There are also new products and initiatives processes applicable to every line of business... -

Page 42

... AND CONSTRUCTION LOANS AND LEASES BY STATE As of December 31 ($ in millions) 2007 2006 Michigan $4,692 4,637 Ohio 4,167 4,072 Florida 2,790 2,543 Illinois 1,425 1,337 Indiana 1,298 1,294 Kentucky 791 794 Tennessee 496 399 All other states 1,131 1,066 Total $16,790 16,142 40 Fifth Third Bancorp As... -

Page 43

...an agency flow sale agreement. Home Equity Portfolio The home equity portfolio is characterized by 86% of outstanding balances within the Bancorp's Midwest footprint of Ohio, Michigan, Kentucky, Indiana and Illinois. The portfolio has an average FICO score of 734 as of December 31, 2007, comparable... -

Page 44

... increased foreclosure rates in the Bancorp's key lending markets and the related increase in severity of loss on mortgage loans. During 2007, Florida, Michigan and Ohio were ranked among the top states in total mortgage foreclosures. These foreclosures not only added to the volume of charge... -

Page 45

... FICO and average line outstanding, the Bancorp does expect the charge-off ratio to increase as the portfolio matures. The Bancorp employs a riskadjusted pricing methodology to ensure adequate compensation is received for those products that have higher credit costs. Allowance for Credit Losses The... -

Page 46

... in real estate values increased the expected loss once a loan becomes delinquent, particularly for home equity loans with high loan-to-value ratios. During 2007, the Bancorp grew credit card balances as part of an initiative to more fully develop relationships with its current customers. In... -

Page 47

...of the product lines offered by the Bancorp as well as other pertinent assumptions. Actual results will differ from these simulated results due to timing, magnitude and frequency of interest rate changes as well as changes in market conditions and management strategies. The Bancorp's Executive Asset... -

Page 48

...available-for-sale securities, assetdriven liquidity is provided by the Bancorp's ability to sell or securitize loan and lease assets. In order to reduce the exposure to interest rate fluctuations and to manage liquidity, the Bancorp has developed securitization and sale procedures for several types... -

Page 49

...and shareholders' equity funded 70% of its average total assets during 2007. In addition to core deposit funding, the Bancorp also accesses a variety of other short-term and long-term funding sources, which include the use of various regional Federal Home Loan Banks as a funding source. Certificates... -

Page 50

... process of residential mortgage loans, certain floating-rate home equity lines of credit, certain automobile loans and other consumer loans. The cash flows to and from the securitization trusts are principally limited to the initial proceeds from the securitization trust at the time of sale... -

Page 51

... Letters of credit (j) 2,759 3,419 1,849 495 8,522 Total other commitments by expiration period $31,330 24,636 1,849 495 58,310 (a) Includes demand, interest checking, savings, money market, other time, certificates $100,000 and over and foreign office deposits. For additional information, see the... -

Page 52

... reporting. Based on this evaluation, there has been no such change during the year covered by this report. Kevin T. Kabat President and Chief Executive Officer February 22, 2008 Christopher G. Marshall Executive Vice President and Chief Financial Officer February 22, 2008 50 Fifth Third Bancorp -

Page 53

... the year ended December 31, 2007 of the Bancorp and our report dated February 22, 2008 expressed an unqualified opinion on those consolidated financial statements. Cincinnati, Ohio February 22, 2008 To the Shareholders and Board of Directors of Fifth Third Bancorp: We have audited the accompanying... -

Page 54

... for Loan and Lease Losses 2,381 Noninterest Income Electronic payment processing revenue 826 Service charges on deposits 579 Investment advisory revenue 382 Corporate banking revenue 367 Mortgage banking net revenue 133 Other noninterest income 153 Securities gains (losses), net 21 Securities gains... -

Page 55

... checking Savings Money market Other time Certificates - $100,000 and over Foreign office Total deposits Federal funds purchased Other short-term borrowings Accrued taxes, interest and expenses Other liabilities Long-term debt Total Liabilities Shareholders' Equity Common stock (c) Preferred stock... -

Page 56

... stock-based compensation Employee stock ownership through benefit plans Impact of diversification of nonqualified deferred compensation plan Other Balance at December 31, 2007 $1,295 9 See Notes to Consolidated Financial Statements Accumulated Other Capital Retained Comprehensive Treasury Surplus... -

Page 57

... other short-term investments Net increase in loans and leases Proceeds from sales of loans (Increase) decrease in operating lease equipment Purchases of bank premises and equipment Proceeds from disposal of bank premises and equipment Net cash (paid) acquired in business combination Net Cash (Used... -

Page 58

...placed on nonaccrual status, all previously accrued and unpaid Fifth Third Bancorp ("Bancorp"), an Ohio corporation, conducts its principal lending, deposit gathering, transaction processing and service advisory activities through its banking and non-banking subsidiaries from banking centers located... -

Page 59

... fair value based on the present value of future expected cash flows using management's best estimates for the key assumptions, including credit losses, prepayment speeds, forward yield curves and discount rates commensurate with the risks involved. Gain or loss on sale or securitization of loans is... -

Page 60

... stock-based awards. Other Securities and other property held by Fifth Third Investment Advisors, a division of the Bancorp's banking subsidiaries, in a fiduciary or agency capacity are not included in the Consolidated Balance Sheets because such items are not assets of the subsidiaries. Investment... -

Page 61

... classes of servicing assets and liabilities at amortized cost subsequent to initial recognition at fair value. The adoption of this Statement did not have a material effect on the Bancorp's Consolidated Financial Statements. In July 2006, the FASB issued FSP No. FAS 13-2, "Accounting for a Change... -

Page 62

..., upon adoption of this Statement, the Bancorp will elect to prospectively measure at fair value, residential mortgage loans originated on or after January 1, 2008 that have a designation as held for sale. In December 2007, the FASB issued SFAS No. 141(R), "Business Combinations" which replaces SFAS... -

Page 63

...the periods presented. Fifth Third Bancorp 61 2. BUSINESS COMBINATIONS On November 2, 2007, the Bancorp acquired 100% of the outstanding stock in R-G Crown Bank, FSB from R&G Financial Corporation. Crown operated 30 branches in Florida and three in Augusta, Georgia. The acquisition strengthened the... -

Page 64

...uncertain economic and interest rate environment. At December 31, 2007, 85% of the unrealized losses in the available-for-sale securities portfolio were comprised of debt securities issued by the U.S. Government sponsored agencies and agency mortgage-backed securities. The Bancorp believes the price -

Page 65

..., trust funds and for other purposes as required or permitted by law. Unrealized gains and losses on trading securities held at December 31, 2007 and 2006 were not material to the Consolidated Financial Statements. 4. LOANS AND LEASES AND ALLOWANCE FOR LOAN AND LEASE LOSSES A summary of the total... -

Page 66

...as of December 31, 2007 Commercial Banking $871 871 124 $995 Branch Banking 798 (1) 797 153 950 Consumer Lending 182 182 182 Investment Advisors 127 11 138 138 Processing Solutions 191 14 205 205 Total 2,169 13 11 2,193 277 2,470 The Bancorp completed its most recent annual goodwill impairment test... -

Page 67

... of residential mortgage loans for other investors. The value of servicing assets is subject to credit, prepayment and interest rate risks on the sold financial assets. At December 31, 2007, the sensitivity of the current fair value of residual cash flows to immediate 10% and 20% adverse changes in... -

Page 68

... and interest rate swaps) and various available-for-sale securities (primarily principal-only strips). The interest income, mark-to-market adjustments and gain or loss on sales activities associated with these portfolios are expected to economically hedge a portion of the change in value of the... -

Page 69

...and interest rate swaps) to economically hedge prepayment volatility. Principal-only swaps are total return swaps based on changes in the value of the underlying mortgage principal-only trust. Foreign currency volatility occurs as the Bancorp enters into certain foreign denominated loans. Derivative... -

Page 70

...corporate banking revenue in the Consolidated Statements of Income. In 2007, the Bancorp began offering its customers an equitylinked certificate of deposit that has a return linked to equity indices. Under SFAS No. 133, a certificate of deposit that pays interest based on changes on an equity index... -

Page 71

... related to held for sale mortgages Derivative instruments related to MSR portfolio Derivative instruments related to foreign currency risk Derivative instruments related to interest rate risk other noninterest income in the Consolidated Statements of Income. The net gains (losses) recorded in the... -

Page 72

...widening of credit spreads between U.S. treasuries/swaps versus municipal bonds and bank trust preferred securities, and illiquidity in the asset-backed securities market. These factors caused the decline in the cash surrender value to exceed the protection provided by the stable value agreement. As... -

Page 73

... prior to their scheduled maturity. During the first quarter of 2007, the Bancorp called the 8.14% junior subordinated debentures due in 2027 to Fifth Third Capital Trust I. Subsidiary Long-Term Borrowings The senior fixed-rate bank notes due from 2008 to 2019 are the obligations of a subsidiary... -

Page 74

... Kent Capital Trust I. In addition, all of the issued and outstanding shares of preferred stock related to the mandatorily redeemable securities of Fifth Third Real Estate Investment Trust, Inc. were purchased by a wholly-owned subsidiary of the parent company during the third quarter of 2007. 14... -

Page 75

...used an approach that is consistent with its overall approach in estimating credit losses for various categories of residential mortgage loans held in its loan portfolio. At the end of the third quarter of 2007, the Bancorp began purchasing asset-backed commercial paper from the QSPE due to widening... -

Page 76

... as employee-stock purchase loans, personal lines of credit, residential secured loans, overdrafts, letters of credit and increases in indebtedness. Such transactions are subject to the Bancorp's normal underwriting and approval procedures. Prior to the loan closing, Compliance Risk Management must... -

Page 77

... service cost Net actuarial loss Total pension and other postretirement obligations Total 2006 Gains on available-for-sale securities Reclassification adjustment for net losses recognized in net income Unrecognized gains (losses) on available-for-sale securities Reclassification adjustment for cash... -

Page 78

... Bancorp's stock repurchase program is an important element of its capital planning activities and the Bancorp views share repurchases as an effective means of delivering value to shareholders. On May 21, 2007, the Bancorp announced that its Board of Directors had authorized management to purchase... -

Page 79

... of a portion of the performance shares that are to be settled in cash. The Bancorp has historically used treasury stock to settle stock-based awards, when available. Stock options, issued at fair market value based on the closing price of the Bancorp's common stock on the date of grant, have up to... -

Page 80

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2007 WeightedAverage Grant-Date Fair Value $40.28 38.19 48.28 40.95 $40.80 2006 WeightedAverage Grant-Date Fair Value $46.16 38.93 44.91 40.76 $40.28 2005 WeightedAverage Grant-Date Fair Value $54.01 42.31 50.62 48.19 $46.16 Restricted Stock (shares in ... -

Page 81

...) Other noninterest income: Bank owned life insurance Cardholder fees Consumer loan and lease fees Insurance income Operating lease income Banking center fees Gain on loan sales Other Total Other noninterest expense: Loan processing Marketing Affordable housing investments Travel Postal and courier... -

Page 82

...) Deferred tax assets: Allowance for credit losses Deferred compensation Other comprehensive income State net operating losses Other Total deferred tax assets Deferred tax liabilities: Lease financing State deferred taxes Bank premises and equipment Mortgage servicing rights Other Total deferred tax... -

Page 83

..., of plan assets were managed by Fifth Third Bank, a subsidiary of the Bancorp, through common trust and mutual funds and included $9 million and $15 million, respectively, of Bancorp common stock. Plan assets are not expected to be returned to the Bancorp during 2008. Fifth Third Bancorp 81 -

Page 84

... in the portfolio's value are tolerated in an effort to achieve real capital growth. Prohibited asset classes of the plan include precious metals, venture capital, short sales and leveraged transactions. Per the Employee Retirement Income Security Act ("ERISA"), the Bancorp's common stock cannot... -

Page 85

... due from banks Available-for-sale and other securities Held-to-maturity securities Trading securities Other short-term investments Loans held for sale Portfolio loans and leases, net Derivative assets Financial liabilities: Deposits Federal funds purchased Other short-term borrowings Long-term debt... -

Page 86

... TO CONSOLIDATED FINANCIAL STATEMENTS 25. CERTAIN REGULATORY REQUIREMENTS AND CAPITAL RATIOS The principal source of income and funds for the Bancorp (parent company) are dividends from its subsidiaries. During 2007, the amount of dividends the bank subsidiaries could pay to the Bancorp without... -

Page 87

... Earnings of Subsidiaries 800 546 Increase in undistributed earnings of subsidiaries 276 642 Net Income $1,076 1,188 Condensed Balance Sheets (Parent Company Only) As of December 31 Assets Cash Loans to subsidiaries Investment in subsidiaries Goodwill Other assets Total Assets Liabilities Commercial... -

Page 88

..., Consumer Lending, Investment Advisors and Processing Solutions. Commercial Banking offers banking, cash management and financial services to large and middle-market businesses, government and professional customers. Branch Banking provides a full range of deposit and loans and lease products to... -

Page 89

... for loan and lease losses Noninterest income: Electronic payment processing Service charges on deposits Investment advisory revenue Corporate banking revenue Mortgage banking net revenue Other noninterest income Securities gains (losses), net Total noninterest income Noninterest expense: Salaries... -

Page 90

... Address: 38 Fountain Square Plaza Cincinnati, Ohio 45263 Telephone: (513) 534-5300 Securities registered pursuant to Section 12(b) of the Act: Common Stock , Without Par Value 7.25% Trust Preferred Securities of Fifth Third Capital Trust V 7.25% Trust Preferred Securities of Fifth Third Capital... -

Page 91

...of financial products and services to the retail, commercial, financial, governmental, educational and medical sectors, including a wide variety of checking, savings and money market accounts, and credit products such as credit cards, installment loans, mortgage loans and leases. Each of the banking... -

Page 92

...debt issuer ratings (if applicable) and various financial ratios derived from the Consolidated Report of Condition and Income ("Call Report"). In 2007, the FDIC set the Deposit Insurance Fund' s designated reserve ratio at 1.25% and the Risk Category I assessment rates range from 5 to 7 basis points... -

Page 93

... anti-money laundering, compliance, suspicious activity and currency transaction reporting and due diligence on customers. The Patriot Act and its underlying regulations also permit information sharing for counter-terrorist purposes between federal law enforcement agencies and financial institutions... -

Page 94

... information regarding regulatory matters is included in Note 25 of the Notes to Consolidated Financial Statements. ITEM 2. PROPERTIES The Bancorp' s executive offices and the main office of Fifth Third Bank are located on Fountain Square Plaza in downtown Cincinnati, Ohio in a 32-story office... -

Page 95

... Banking Division, Fifth Third Bank (Northwestern Ohio) since March 2001. Christopher G. Marshall, 48. Executive Vice President and Chief Financial Officer of the Bancorp since May 2006. Previously, Mr. Marshall was a senior executive for Bank of America and served in various management capacities... -

Page 96

... return experienced by the Bancorp's shareholders over the years 2003 through 2007, and 1998 through 2007, respectively, compared to the S&P 500 Stock, the S&P Banks, and the NASDAQ Banks indices. Beginning with the 2008 Annual Report on Form 10-K, the performance graph will no longer compare Fifth... -

Page 97

...among Fifth Third Bancorp, as Depositor, Wilmington Trust Company, as Property Trustee, and the Administrative Trustees named therein. Incorporated by reference to Registrant' s Current Report on Form 8-K filed with the Securities and Exchange Commission on March 26, 1997. Guarantee Agreement, dated... -

Page 98

... Capital Covenant of Fifth Third Bancorp dated as of October 30, 2007. Incorporated by reference to Registrant' s Current Report on Form 8-K filed with the Securities and Exchange Commission on October 31, 2007. 10.1 Fifth Third Bancorp Unfunded Deferred Compensation Plan for Non-Employee Directors... -

Page 99

... Ratios of Earnings to Combined Fixed Charges and Preferred Stock Dividend Requirements. 14 Code of Ethics. Incorporated by reference to Exhibit 14 of the Registrant' s Current Report on Form 8-K filed with the Securities and Exchange Commission on January 23, 2007. 21 Fifth Third Bancorp... -

Page 100

..., thereunto duly authorized. FIFTH THIRD BANCORP Registrant Kevin T. Kabat President and CEO Principal Executive Officer February 22, 2008 Pursuant to requirements of the Securities Exchange Act of 1934, this report has been signed on February 22, 2008 by the following persons on behalf of the... -

Page 101

... 3,179 135 (58) 5,390 (a) Federal funds sold and interest-bearing deposits in banks are combined in other short-term investments in the Consolidated Financial Statements. (b) Adjusted for stock splits in 2000 and 1998. Allowance Book Value for Loan Per and Lease Share (b) Losses $17.20 $937 18.02... -

Page 102

...McHugh Louisville Jordan A. Miller, Jr. Central Ohio John E. Pelizzari Central Indiana Robert A. Sullivan Cincinnati Michelle L. VanDyke Western Michigan Raymond J. Webb Western Ohio Charles N. Reeves Chicago FIFTH THIRD BANCORP BOARD COMMITTEES Executive Committee George A. Schaefer, Jr., Chairman... -

Page 103

... common stock of Fifth Third Bancorp is traded in the over-the-counter market and is listed under the symbol "FITB" on the NASDAQ Global Select Market System. Press Releases For copies of current press releases, please visit .53.com. our Web site at Fifth Third Bank 2008 Member FDIC - Federal... -

Page 104

www.53.com