Fifth Third Bank 2003 Annual Report Download

Download and view the complete annual report

Please find the complete 2003 Fifth Third Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

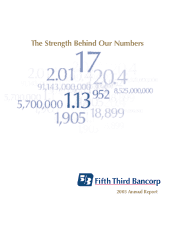

The Strength Behind Our Numbers

2003 Annual Report

Table of contents

-

Page 1

The Strength Behind Our Numbers 2003 Annual Report -

Page 2

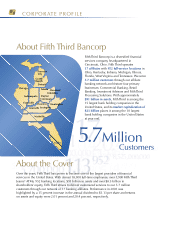

... Toledo Cleveland Columbus Dayton Cincinnati Florence Huntington Lexington Louisville Nashville Fifth Third Bancorp is a diversified financial services company headquartered in Cincinnati, Ohio. Fifth Third operates 17 affiliates with 952 full-service locations in Ohio, Kentucky, Indiana, Michigan... -

Page 3

... Number of Full-Time Equivalent Employees Shareholders of Record Debt Ratings Moody's Fifth Third Bancorp Commercial Paper Senior Debt Fifth Third Bank and Fifth Third Bank (Michigan) Short-Term Deposit Long-Term Deposit Prime-1 Aa2 Standard & Poor's A-1+ AAFitch F1+ AA2003 2002 Percent Change... -

Page 4

... focused loan and deposit sales effort and continued growth from our service businesses. We also invested significantly in strengthening your investment in Fifth Third for the years to come by adding new banking center locations in vibrant growth markets, increasing automation of processes, building... -

Page 5

...department, and build an enterprise-wide risk management function that will help ensure the scalability and strength of your company. These improvements in processes and infrastructure complement our local market operating model and meet the needs of a larger and growing financial institution. Fifth... -

Page 6

... business lines in our five principal states, so we have a tremendous opportunity in all of our markets. In terms of The primary driver of shareholder value at Fifth Third is consistent and strong growth in earnings per diluted share. The industry will fall in and out of favor with investors... -

Page 7

... by the ability to place experienced Fifth Third managers in these markets? I think we will continue to focus on what we do best: Retail and Commercial Banking, Investment Advisors and Electronic Payment Processing. We like the businesses we're in and believe our operating model is the best in the... -

Page 8

... former executive at Old Kent Financial. The affiliate was formed from the April 2001 purchase of Old Kent and conversion to Fifth Third's affiliate operating platform of banking operations in Grand Rapids, Lansing, Kalamazoo, and the Lakeshore areas of Western Michigan. Today, the Western Michigan... -

Page 9

Western Michigan $6.9 billion in deposits $9.3 billion in assets 136 banking locations Mark Michon Investment Advisors Michelle VanDyke Retail Banking Increased advertising and a broader product set, combined with a best-in-class sales management process that brings individual accountability to the... -

Page 10

... mortgage banking and time deposit driven platform. Demand deposits have grown at a ten year annualized rate of 43 percent and now represent over 26 percent of the total deposits in the market from just one percent at formation. By aggressively adding commercial relationship managers, Louisville... -

Page 11

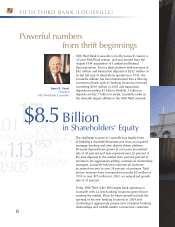

... in deposits $2.7 billion in assets 43 banking locations Aubrey Hayden Retail Banking In the last three years, Louisville has earned $142 million in net income, or $16 million more than the total stock and cash consideration paid for the acquisition that provided entry into the market. Louisville... -

Page 12

... sheet and improving the profitability of acquired thrifts and banking centers in the market, as well as building new full-service banking centers and building out other business lines. During this time, Cleveland has seen service revenues increase to over 43 percent of total revenues and commercial... -

Page 13

...in assets 76 banking locations Don Graham Consumer Lending In 2003, Cleveland delivered 27 percent growth in demand deposits, 35 percent growth in interest checking accounts, 48 percent growth in service revenues, and 28 percent growth in total revenues over the prior year. Net income per employee... -

Page 14

... with an additional 73 banking centers from the 2001 acquisition of Old Kent. Today, Chicago has 109 banking locations and is the third largest affiliate in the Fifth Third network and comprises 14 percent of the Bancorp's deposits and 10 percent of its total assets. Since the conversion to... -

Page 15

... of savings banks in the Chicagoland area. With over 150 new sales hires, Chicago has seen total revenue increase by 18 percent in 2003. In deposit and loan campaigns conducted throughout the year, the Chicago affiliate was responsible for 26 percent of new Bancorp checking account balances... -

Page 16

...grants for Arts & Culture, Community Development, Education, and Health & Human Services, while the Fifth Third Community Development Corporation invests in low-income housing, historic tax credit and economic development projects to support community revitalization. Our Community Affairs department... -

Page 17

... Fifth Third Bancorp's Supplier Diversity Business Opportunities Program. "We're looking for highquality companies to partner with, and we are committed to enhancing and ensuring the diversity of our supplier base." Ms. Zuberi is responsible for managing market analyses, identifying purchasing... -

Page 18

... of Changes in Shareholders' Equity Consolidated Statements of Cash Flows Notes to Consolidated Financial Statements Independent Auditors' Report Management's Discussion and Analysis of Financial Condition and Results of Operations Consolidated Ten Year Comparison Directors and Officers Corporate... -

Page 19

... Short-Term Investments ...Total Interest Income ...Interest Expense Interest on Deposits: Interest Checking ...Savings ...Money Market ...Other Time ...Certificates-$100,000 and Over ...Foreign Office ...Total Interest on Deposits ...Interest on Federal Funds Purchased ...Interest on Other Short... -

Page 20

... Assets...Servicing Rights ...Other Assets...Total Assets ...Liabilities Deposits: Demand ...Interest Checking ...Savings ...Money Market ...Other Time ...Certificates-$100,000 and Over...Foreign Office...Total Deposits ...Federal Funds Purchased ...Short-Term Bank Notes ...Other Short-Term... -

Page 21

...and Nonowner Changes in Equity, Net of Tax: Net Income ...Change in Unrealized Gains (Losses) on Securities Available-for-Sale, Net ...Change in Unrealized Losses on Qualifying Cash Flow Hedges ...Net Income and Nonowner Changes in Equity Cash Dividends Declared: Fifth Third Bancorp: Common Stock at... -

Page 22

...Cash (Used in) Provided by Investing Activities ...Financing Activities Increase in Core Deposits ...Increase (Decrease) in Certificates - $100,000 and Over, including Foreign Office ...Increase in Federal Funds Purchased ...Increase (Decrease) in Short-Term Bank Notes...Increase (Decrease) in Other... -

Page 23

... Accounting and Reporting Policies Nature of Operations Fifth Third Bancorp (Bancorp), an Ohio corporation, conducts its principal activities through its banking and non-banking subsidiaries from 952 banking centers located throughout Ohio, Indiana, Kentucky, Michigan, Illinois, Florida, West... -

Page 24

... of Income. Servicing rights resulting from residential mortgage and home equity line of credit loan sales are amortized in proportion to and over the period of estimated net servicing revenues and are reported as a component of mortgage banking net revenue and other service charges and fees... -

Page 25

...a fee charged on the market value of ending account balances associated with individual contracts. The Bancorp recognizes revenue from its electronic payment processing services as such services are performed, recording revenues net of certain costs (primarily interchange fees charged by credit card... -

Page 26

...15, 2002. As permitted by SFAS No. 148, during 2003 the Bancorp continued to apply the provisions of APB Opinion No. 25, "Accounting for Stock-Based Compensation," for all employee stock option grants and has elected to disclose pro forma net income and earnings per share amounts as if the fairvalue... -

Page 27

... of December 31, 2003, the outstanding balance of leased autos sold was approximately $767 million. Consolidation of these operating lease assets did not impact risk-based capital ratios or bottom line income statement trends; however lease payments on the operating lease assets are now reflected as... -

Page 28

... Unrealized Gains Losses Fair Value At December 31, 2003, 95% of the unrealized losses in the available-for-sale security portfolio were comprised of securities issued by U.S. Government agencies, U.S. Government sponsored agencies and investment grade municipalities. The Bancorp believes that... -

Page 29

... have entered into a number of noncancelable lease agreements with respect to bank premises and equipment. A summary of the minimum annual rental commitments under noncancelable lease agreements for land and buildings at December 31, 2003, exclusive of income taxes and other charges payable by the... -

Page 30

... manage a portion of the risk associated with changes in impairment on the mortgage servicing rights (MSR) portfolio. This strategy includes the purchase of various securities (primarily FHLMC and FNMA agency bonds, U.S. treasury bonds and principal only (PO) strips) and the purchase of various free... -

Page 31

... lock commitments and changes in fair value of its largely fixed rate MSR portfolio. PO swaps are total return swaps based on changes in the value of the underlying PO trust. The Bancorp also enters into foreign exchange contracts, interest rate swaps, floors and caps for the benefit of customers... -

Page 32

... entered into for the benefit of customers by entering into offsetting third-party forward contracts with approved reputable counterparties with matching terms and currencies that are generally settled daily. Interest rate lock commitments issued on residential mortgage loan commitments that will be... -

Page 33

... 2003, the Bancorp had issued $4 million in commercial paper, with unused lines of credit of $96 million available to support commercial paper transactions and other corporate requirements. The 8.136% Junior Subordinated Debentures due in 2027 were issued by the Bancorp to Fifth Third Capital Trust... -

Page 34

...interest rate floors and caps, principal only swaps, purchased and sold options and interest rate lock commitments. These instruments 32 Commitments to extend credit are agreements to lend, generally having fixed expiration dates or other termination clauses that may require payment of a fee. Since... -

Page 35

... 2003, eight putative class action complaints were filed in the United States District Court for the Southern District of Ohio against the Bancorp and certain of its officers alleging violations of federal securities laws related to disclosures made by the Bancorp regarding its integration of Old... -

Page 36

... provided including commercial real estate, physical plant and property, inventory, receivables, cash and marketable securities. Through December 31, 2003, the Bancorp had transferred, subject to credit recourse, certain primarily fixed-rate and short-term investment grade commercial loans to an... -

Page 37

... Plan, the Bancorp's total overhang is approximately eight percent. The following provides detail of the number of shares to be issued upon exercise of outstanding options and remaining shares available for future issuance under all of the Bancorp's equity compensation plans, as of December 31, 2003... -

Page 38

... and lease fees ...Commercial banking revenue ...Bank owned life insurance income ...Insurance income ...Gain on sale of branches...Gain on sale of property and casualty insurance product lines...Other ...Total Other Service Charges and Fees ...Other Operating Expenses: Marketing and communications... -

Page 39

... lower yielding loan assets and at the same time maintain these customer relationships. These commercial loans are transferred at par with no gain or loss recognized. The Bancorp receives rights to future cash flows arising after the investors in the securitization trust have received the return for... -

Page 40

...Balance Sheets and are comprised of the following temporary differences at December 31: ($ in millions) Lease financing ...Reserve for credit losses ...Bank premises and equipment ...Net unrealized gains on securities available-for-sale and hedging instruments . Mortgage servicing and other ...Total... -

Page 41

... service cost ...Settlement ...Net periodic pension cost ...2003 2003 $ (41) (1) 4 103 $ 65 2002 (66) (4) 5 98 33 Plan assets consist primarily of common trust and mutual funds (equities and fixed income) managed by Fifth Third Bank, an affiliate of the Bancorp, and Bancorp common stock securities... -

Page 42

... subordinated debentures due 2028, net of tax ...Dividends on convertible preferred stock ...Income from continuing operations plus assumed conversions ...Income from discontinued operations, net of tax ...Cumulative effect of change in accounting principle, net of tax ...Net income available... -

Page 43

... ...Securities available-for-sale ...Securities held-to-maturity ...Trading securities ...Other short-term investments ...Loans held for sale ...Total loans and leases, net ...Derivative assets ...Bank owned life insurance assets ...Financial Liabilities: Deposits ...Federal funds purchased ...Short... -

Page 44

... costs ...20 Loss on portfolio sales ...29 Net loss on sales of subsidiaries and outof-market line of business operations ...15 Other ...16 Merger-related charges ...$349 29. Regulatory Requirements and Capital Ratios The principal source of income and funds for the Bancorp (parent company... -

Page 45

... Third Bank (Ohio)...Fifth Third Bank (Michigan) ...Amount $8,844 4,444 3,771 7,656 3,592 3,269 7,656 3,592 3,269 Ratio 13.51% 11.68 12.00 11.70 9.44 10.40 9.73 7.93 8.58 Ratio 13.38% 11.59 11.03 10.94 9.76 9.43 9.11 7.57 8.50 Condensed Balance Sheets (Parent Company Only) At December 31 2003 Assets... -

Page 46

... transactions, principally EFT services from Fifth Third Processing Solutions to the banking segments, are generally charged at rates available to and transacted with unaffiliated customers. The performance measurement of the operating segments is based on the management structure of the Bancorp... -

Page 47

...Taxes (c) ...Minority Interest, Net ...Discontinued Operations, Net ...Cumulative Effect, Net ...Dividends on Preferred Stock ...Net Income Available to Common Shareholders ...Selected Financial Information Identifiable Assets ... Commercial Banking $ 1,086 187 899 435 489 845 (276) - 44 - - $ $ 613... -

Page 48

...' Report To the Shareholders and Board of Directors of Fifth Third Bancorp: We have audited the consolidated balance sheets of Fifth Third Bancorp and subsidiaries ("Bancorp") as of December 31, 2003 and 2002, and the related consolidated statements of income, changes in shareholders' equity, and... -

Page 49

... report. Net income for 2003 also includes after-tax income from discontinued operations of $44 million, or $.08 per diluted share. In December 2003, the Bancorp completed the sale of its corporate trust business enabling the Bancorp to refine its focus and reinvest in core middle market business... -

Page 50

......$18,679 Savings ...8,020 Money Market...3,189 Other Time Deposits ...7,168 Certificates-$100,000 and Over . 3,090 Foreign Office Deposits ...3,862 Federal Funds Purchased ...7,001 Short-Term Bank Notes ...22 Other Short-Term Borrowings . . 5,350 Long-Term Debt ...8,747 Total Interest-Bearing... -

Page 51

... (2) Total Interest Income Change ...662 (800) Increase (Decrease) in Interest Expense: Interest Checking ...40 (147) Savings ...(21) (73) Money Market ...27 (22) Other Time Deposits ...(75) (68) Certificates - $100,000 and over ...30 (40) Foreign Office Deposits ...24 (15) Federal Funds Purchased... -

Page 52

...with notable growth in Chicago, Columbus, Cleveland, Cincinnati, Detroit and Grand Rapids. Retail based deposit revenue increased 11% in 2003 compared to 2002, driven by the success of sales campaigns and direct marketing programs in generating new account relationships. Mortgage banking net revenue... -

Page 53

... in Southern Illinois. The commercial banking revenue component of other service charges and fees grew 13% to $178 million in 2003, led by strong growth in international department revenue which includes foreign currency exchange revenue and letter of credit fee revenue. Compared to 2002, total... -

Page 54

...the yield of a portfolio of high quality fixed-income instruments that have a similar duration to the Plan's liabilities. The discount rate determined on this basis has decreased from 6.75% at December 31, 2002 to 6% at December 31, 2003. Lowering the expected long-term rate of return on Plan assets... -

Page 55

...) Commercial, financial and agricultural loans...Real estate - construction loans ...Real estate - mortgage loans ...Consumer loans ...Lease financing...Loans and leases, net of unearned income...Reserve for credit losses...Loans and leases, net of reserve . . Loans held for sale ...2003 Amount... -

Page 56

... 31, 2003 consisted of Federal Home Loan Bank, Federal Reserve Bank and FHLMC stock holdings totaling approximately $650 million and certain mutual fund holdings and equity security holdings totaling approximately $313 million. The estimated average life of the available-for-sale portfolio increased... -

Page 57

... sale of $903 million in home equity lines of credit in the third quarter of 2003. The sale of certain home equity lines of credit was undertaken to limit balance sheet leverage due to the exceptionally strong demand experienced in this asset class during 2003 relative to the entire loan and lease... -

Page 58

... lease balances, net of unearned income, and exposure reflects total commercial customer lending commitments. To maintain balance sheet flexibility and enhance liquidity during 2003 and 2002, the Bancorp transferred, with servicing retained, certain primarily fixed-rate, short-term investment grade... -

Page 59

... credit improvement and certain charge-off outflows in several markets including Chicago, Columbus, Grand Rapids, Evansville and Cincinnati. Table 16 provides a breakout of the commercial nonaccrual loans and leases by loan size, further illustrating the granularity of the Bancorp's commercial loan... -

Page 60

... - construction loans ...Real estate - residential mortgage loans ...Consumer loans ...Lease financing...Total net losses charged off ...Reserve for credit losses, January 1 ...Net losses charged off ...Reserve of acquired institutions and other...Provision charged to operations ...Merger-related... -

Page 61

... 31 ($ in millions) Commercial, financial and agricultural loans ...Real estate - commercial mortgage loans ...Real estate - construction loans ...Real estate - residential mortgage loans ...Consumer loans ...Lease financing ...Unallocated reserve ...Total reserve for credit losses ...2003 $292.6 77... -

Page 62

...-term borrowings primarily fund short-term, rate-sensitive earning-asset growth. As part Table 22-Distribution of Average Deposits ($ in millions) Demand ...Interest checking...Savings ...Money market ...Other time...Certificates-$100,000 and over ...Foreign office ...Total ...2003 Amount $10,482... -

Page 63

...'s management, corporate governance, internal audit, account reconciliation procedures and policies, information technology and strategic planning. The Bancorp has submitted all documentation and information currently required by the Written Agreement, including all independent third-party reviews... -

Page 64

...'s affiliate structure or operating model. Legal Proceedings During 2003, eight putative class action complaints were filed in the United States District Court for the Southern District of Ohio against the Bancorp and certain of its officers alleging violations of federal securities laws related to... -

Page 65

... upon origination. Periodically, additional assets such as jumbo fixed-rate residential mortgages, certain floating rate short-term commercial loans and certain floating rate home equity loans are also securitized, sold or transferred off-balance sheet. During 2003 and 2002, a total of $15.9 billion... -

Page 66

... their effect on loan demand, credit losses, mortgage origination fees, the value of mortgage servicing rights and other sources of the Bancorp's earnings. Consistency of the Bancorp's net interest income is largely dependent upon the effective management of interest rate risk. The Bancorp employs... -

Page 67

... loans and historical loss rates are reviewed quarterly and adjusted as necessary based on changing borrower and/or collateral conditions and actual collection and charge-off experience. The Bancorp's primary market areas for lending are Ohio, Kentucky, Indiana, Florida, Michigan, Illinois, West... -

Page 68

...." This Statement addresses financial accounting and reporting for obligations associated with the retirement of tangible long-lived assets and the associated asset retirement costs. This Statement amends SFAS No. 19, "Financial Accounting and Reporting by Oil and Gas Producing Companies," and was... -

Page 69

... of December 31, 2003, the outstanding balance of leased autos sold was approximately $767 million. Consolidation of these operating lease assets did not impact risk-based capital ratios or bottom line income statement trends; however lease payments on the operating lease assets are now reflected as... -

Page 70

... an estimated credit loss reserve of approximately $14 million relating to these residential mortgage loans sold. Through December 31, 2003, the Bancorp, through its electronic payment processing division, processed approximately 89.3 billion of VISA® and MasterCard® merchant card transactions... -

Page 71

... ($ in millions) Total 1 Year Years Years Years Total Deposits ...$57,095 53,776 2,298 472 549 Long-Term Borrowings ...9,063 668 1,345 3,608 3,442 Short-Term Borrowings ...13,170 13,170 - - - Annual Rental/Purchase Commitments Under Noncancelable Leases/Contracts ...341 72 86 69 114 Total ...$79,669... -

Page 72

.... Table 31-Condensed Consolidated Balance Sheet Information As of December 31 ($ in millions) Securities ...Loans and Leases...Loans Held for Sale...Assets ...Deposits ...Short-Term Borrowings ...Long-Term Debt and Convertible Subordinated Debentures . . Shareholders' Equity ...2003 $29,189 52,308... -

Page 73

... Ten Year Comparison Average Assets ($ in millions) Loans and Leases $52,414 45,539 44,888 42,690 38,652 36,014 33,850 30,742 27,598 22,849 Federal Funds Sold (a) $ 92 155 69 118 224 241 327 325 494 340 Interest-Earning Assets Interest-Bearing Deposits in Banks (a) Securities $215 $28,640 184... -

Page 74

... Northwestern Ohio FIFTH THIRD BANCORP BOARD COMMITTEES Samuel G. Barnes Lexington, Kentucky Todd F. Clossin Tennessee John N. Daniel Southern Indiana Robert M. Eversole Central Ohio Patrick J. Fehring, Jr. Eastern Michigan James R. Gaunt Louisville, Kentucky Kevin T. Kabat Western Michigan Robert... -

Page 75

... President & Investor Relations Officer (513) 534-0983 (513) 534-0629 (fax) Independent Auditor Deloitte & Touche LLP 250 East Fifth Street Cincinnati, OH 45202 Transfer Agent Computershare Investor Services LLC PO Box 2388 Chicago, IL 60690-2388 (888) 294-8285 Investordirect.53.com Stock Trading... -

Page 76

www.53.com