Dominion Power 2010 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2010 Dominion Power annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

|

|

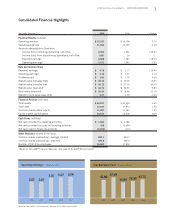

6XPPDU\ $QQXDO 5HSRUW'20,1,21 5(6285&(6

assets that did not or were not expected to produce ad-

equate returns on invested capital (ROIC). This would

support a strong balance sheet, stable credit ratings,

and the ability to provide investors with competitive

utility dividends.

(;(&87,1* 7+( 3/$1

To execute our plan, the company in 2007 divested

our non-Appalachian E&P assets for nearly $14 bil-

lion. The after-tax proceeds reduced outstanding debt

by $3.3 billion and also allowed us to repurchase more

than $5.8 billion of common stock, more than 18

percent of the total shares outstanding as of December

31, 2006. Further, as theVirginia General Assembly

passed legislation in 2007 to reregulate the state’s elec-

tric utilities and provide premium returns on equity

for critical infrastructure investments, the company

focused its efforts on a build-out to serve our

customers’ needs.

Management continued to reduce commodity and

merchant risk and evaluate remaining business lines to

ensure that they met our targets for actual and poten-

tial ROIC.

As a result, last year we sold the remainder of our

E&P operations in the Appalachian region for nearly

$3.5 billion, including hundreds of thousands of acres

holding Marcellus Shale, one of the largest recoverable

gas discoveries in recent years. Because of our pipeline

and storage system’s strong presence throughout the

Marcellus Shale region, we believed it made better

business sense to sell our production interests there

and instead renew our focus on energy infrastructure.

Shareholder capital, we concluded, had more value in

improving existing infrastructure and building new

products extraction facilities, gathering, storage, and

transmission pipelines — infrastructure that would

help producers more effectively and efficiently get

natural gas to demand centers.

The Appalachian E&P transaction reduced our

overall, companywide commodity exposure by an ad-

ditional 20 percent and annual capital expenditures by

$250 million. We used the after-tax proceeds to offset

2010 and 2011 equity needs, buy back common stock,

pay down debt and make a contribution to our pen-

sion plan.

Based on ROIC considerations, we also closed on

the sale of Dominion Peoples, a gas local distribution

company serving parts of Pennsylvania, for $780 mil-

lion and reduced debt with the proceeds. Dominion

also divested its interest in Rumford and Morgantown,

two small merchant coal-fired power stations in Maine

and West Virginia, respectively.

5(68/76 2) 285 5(326,7,21,1*

We have been pleased with the success of our trans-

formation to date. I must admit, however, that timing

and, to some extent, luck have played their part. Back

in 2006, when we decided to market our non-Appala-

chian E&P business, we did not know that natural gas

and oil prices would plummet or that the Gulf of Mex-

ico would be home to history’s largest oil spill. And at

'20,1,21 5(6285&(6 6XPPDU\ $QQXDO 5HSRUW

32:(5,1*9,5*,1,$

3/($6( /,)7

'20,1,21·6

75$16)250$7,21

*52:7+ ²

6XPPDU\ $QQXDO 5HSRUW'20,1,21 5(6285&(6