Dell 2002 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2002 Dell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

Table of Contents

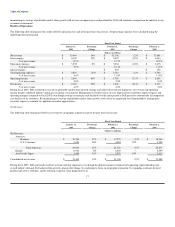

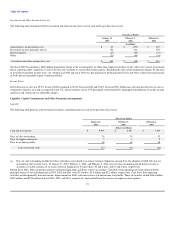

Dell's estimates further impacting revenue recognition relate primarily to customer returns and allowance for doubtful accounts. Both estimates are relatively

predictable based on historical experience. The primary factors affecting Dell's accrual for estimated customer returns include estimated return rates as well as

the number of units shipped that still have rights of return as of the balance sheet date. Customer returns historically have represented approximately 2% of

gross revenues. Factors affecting Dell's allowance for doubtful accounts include historical and anticipated customer default rates at the various aging

categories of accounts receivable. Each quarter, Dell reevaluates its estimates to assess the adequacy of its recorded accruals for customer returns and

allowance for doubtful accounts and adjusts the amounts as necessary.

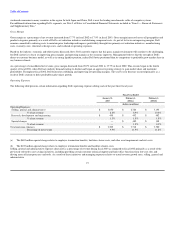

Warranty — Dell records warranty liabilities for the estimated costs that may be incurred under its basic limited warranty as well as under separately priced

extended warranty and service contracts for which Dell is obligated to perform. These liabilities are accrued at the time product revenue is recognized. The

specific warranty terms and conditions vary depending upon the product sold and country in which Dell does business, but generally includes technical

support, repair parts and labor and a period ranging from 90 days to three years. Factors that affect Dell's warranty liability include the number of installed

units currently under warranty, historical and anticipated rates of warranty claims on those units and cost per claim to satisfy Dell's warranty obligation. The

anticipated rate of warranty claims is the primary factor impacting Dell's estimated warranty obligation. The other factors are relatively insignificant because

the average remaining aggregate warranty period of the covered installed base is approximately 20 months, repair parts are generally already in stock or

available at pre-determined prices, and labor rates are generally arranged at pre-established amounts with service providers. Warranty claims are relatively

predictable based on historical experience of failure rates. Each quarter, Dell reevaluates its estimates to assess the adequacy of its recorded warranty

liabilities and adjusts the amounts as necessary.

Recently Issued Accounting Pronouncements

In June 2002, the FASB issued Statement of Financial Accounting Standard ("SFAS") No. 146, Accounting for Costs Associated with Exit or Disposal

Activities. SFAS 146 provides guidance on the accounting for recognizing, measuring and reporting of costs associated with exit and disposal activities,

including restructuring activities. SFAS 146 adjusts the timing of when a liability for termination benefits is to be recognized based on whether the employee

is required to render future service. A liability for costs to terminate an operating lease or other contract before the end of its term is to be recognized when the

entity terminates the contract or ceases using the rights conveyed by the contract. All other costs associated with an exit or disposal activity are to be expensed

as incurred. SFAS 146 requires the liability to be measured at its fair value with subsequent changes in fair value to be recognized each reporting period

utilizing an interest allocation approach. The pronouncement is effective for exit or disposal activities initiated after December 31, 2002 and is not expected to

have a material impact on Dell's consolidated results of operations or financial position.

In November 2002, the Emerging Issues Task Force ("EITF") reached a consensus regarding EITF Issue 00-21, Accounting for Revenue Arrangements with

Multiple Deliverables. The consensus addresses not only when and how an arrangement involving multiple deliverables should be divided into separate units

of accounting but also how the arrangement's consideration should be allocated among separate units. The pronouncement is effective for Dell commencing

with its fiscal year 2004 and is not expected to have a material impact on Dell's consolidated results of operations or financial position.

In November 2002, FASB issued Interpretation No. 45 ("FIN 45"), Guarantor's Accounting and Disclosure Requirements for Guarantees, Including Indirect

Guarantees of Indebtedness of Others. FIN 45 requires certain guarantees to be measured at fair value upon issuance and recorded as a liability. In addition,

FIN 45 expands current disclosure requirements regarding guarantees issued by an entity, including tabular presentation of the changes affecting an entity's

aggregate product warranty liability. The recognition and measurement requirements of the interpretation are effective

27