Chesapeake Energy 2010 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2010 Chesapeake Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

vs. an asset gatherer — namely, lower debt and higher returns on capi-

tal. The market has received this plan with favor to date as our stock

price is already up 30% in the first quarter of 2011. In addition, having

recently closed the sale of our Fayetteville Shale assets to BHP Billiton

and recently initiated tender offers for repayment of at least $2.0 billion

of our long-term debt, we are already close to accomplishing the 25%

long-term debt reduction portion of our 25/25 Plan. Now we will focus

on delivering the other part of the equation, 25% growth in production

by year-end 2012.

Beyond the next two years, there will be many other benefits of the

three-way transition we began in 2010. In fact, we are increasingly con-

fident that we can double our cash flow and net income by year-end

2015. By accomplishing these goals and also having our historic trading

multiples expand a bit, we are hopeful that we can achieve a $100 stock

price by year-end 2015, perhaps creating the need for a “100/15” plan in

the process! Clearly it would be an ambitious goal, and to achieve it we

will need the world’s economy to continue growing, China and other

emerging economies to continue their rapidly growing thirst for oil and

natural gas, our new plays to meet expectations, oil prices to remain

strong and natural gas prices not to weaken from where they are today.

However, Chesapeake’s growth from here on will be very mechanical

with our “factories” (meaning both our individual wells and our large

plays) needing only four inputs for success: land, science, people and

capital. We now have gathered enough of these four inputs so that our

factories can run in harvest mode for decades to come, which hopefully

can lead to a $100 stock price by year-end 2015. Again, this would be a

very considerable achievement, but your management team enjoys big

challenges and we look forward to discussing it further with you in the

quarters ahead.

Great Assets = A Great Future

The very significant upward trajectory of value creation that Chesapeake

is on today is primarily driven by the quality of our assets, which feature

dominant positions in 16 of the 20 most important major unconvention-

al natural gas and liquids plays in the U.S. — the Barnett, Haynesville,

Bossier, Marcellus, Eagle Ford, Pearsall, Niobrara and Utica shales

and the Granite Wash, Cleveland, Tonkawa, Mississippian, Bone Spring,

Avalon, Wolfcamp and Wolfberry tight sands and fractured carbonates.

Having only missed the Bakken Shale play in the Williston Basin, having

passed on the Cana Shale play in Oklahoma and having sold out of

the Woodford and Fayetteville shale plays in Oklahoma and Arkansas

(for overall value creation of $5.4 billion), Chesapeake’s unrivaled posi-

tion in the 16 other major U.S. unconventional plays is remarkable and

unprecedented and should form the foundation of further substantial

value creation for Chesapeake’s shareholders for decades to come.

The gathering of these assets has been hard work for our employ-

ees and management team, and during 2010 it stretched our balance

sheet and tested the patience of some of our shareholders. What is

clear now, however, is that we have created a tremen-

dous storehouse of value and an abundance of oppor-

tunities for bountiful harvests for years to come for our

shareholders.

Given the importance of these 16 unconventional

plays, I have provided below a brief summary of our posi-

tion in each of them:

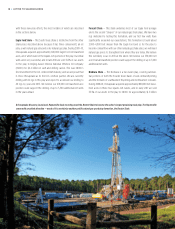

Barnett Shale — Discovered in the 1990s, the Barnett is the

granddaddy of all U.S. shale plays. Chesapeake acquired

its first assets in the Barnett in 2001, and in 2005 we began

aggressively leasing in the core of the play in Johnson and

Tarrant counties. Today we own approximately 220,000

net leasehold acres, on which we estimate we could drill

up to 2,300 future net wells in addition to our 965 net

wells currently producing. We are currently using 18 rigs to

develop this inventory of drillsites and our gross operated

production in the Barnett recently set a record of more

than 1.3 bcfe per day.

Our most important development in the Barnett Shale

during 2010 was closing the joint venture agreement on

25% of our assets in the Barnett to Paris-based Total,

the fifth-largest oil company in the world. Total paid

6 | LETTER TO SHAREHOLDERS

The knowledge and experience Chesapeake gained in the Barnett Shale, the granddaddy

of all U.S. shale plays, has been instrumental in the company’s successful development

of all subsequent unconventional natural gas and liquids plays.