Chesapeake Energy 2002 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2002 Chesapeake Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13

|

|

acquisitions without disrupting the normal flow of our

work. We also have a team of acquisition experts that

focuses on purchasing smaller working and mineral

interest owners in the company’s existing wells. Because

Chesapeake operates 5,700 wells and has more than

33,000 co-owners, we find numerous opportunities

each year to consolidate ownership in the company’s

wells at very attractive acquisition costs.

Given that further consolidation among public compa-

nies in our industry is likely and that smaller private

companies will continue experiencing more challenging

operational and financial environments, Chesapeake

expects to continue making value-added Mid-Continent

gas acquisitions in the years ahead. One of the keys to

success in this industry is the ability to generate bal-

anced growth. Sometimes it is more advantageous to

drill, and sometimes it is better to acquire. Chesapeake’s

historical performance demonstrates that its excellence

in both areas is a key competitive advantage.

Chesapeake’s History

As Chesapeake’s co-founders, we would like to put into

historical context the company’s achievements of the

past ten years. Chesapeake’s roots go back to 1983

when we were 24-year-old landmen competing for

leases in a hot play near the Oklahoma City airport.

We were both native Oklahomans with third genera-

tion roots who had recently left the companies we were

working for to go out on our own.

From 1983 to 1989, we operated a small 50/50 part-

nership on a handshake, generating oil and gas

prospects for sale to the industry and participating as

non-operators in the drilling of wells by others.

Around the time of our 30th birthdays in 1989, we

decided to start operating wells and incorporated

Chesapeake with a $50,000 investment.

Our first drilling efforts focused on the Golden Trend

and Sholem Alechem fields in southern Oklahoma and

on the Giddings field in south Texas. As a result of ini-

tial drilling successes in these three fields, the company

grew quickly, and in February 1993 Chesapeake com-

pleted its IPO at the split-adjusted price of $1.33 per

share. This valued the company at approximately $70

million and reduced our common stock ownership

position to just under 60% from 100%.

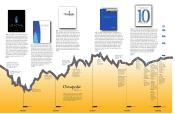

After a rocky start in 1993 (the stock declined 65%),

Chesapeake began to grow rapidly from 1994 through

1996 through a series of major natural gas discoveries

in the Giddings Field in southeast Texas. During this

extraordinary three-year period, the company’s stock

price increased 73-fold from $0.47 per share to $34.44

per share, making Chesapeake the #1 performing stock

in America. During this time, the company’s enterprise

value soared from a low of $35 million in early 1994 to

a peak of $2.7 billion in late 1996. However, because

of a failed effort to extend the company’s success in

the Austin Chalk trend from Texas into Louisiana

and a dramatic collapse in oil and natural gas prices,

Chesapeake’s stock fell during 1997 through early

1999 reaching a low of $0.63 per share.

Facing the need to redefine Chesapeake’s strategy and

underpin the company with longer-lived assets and

lower-risk drilling opportunities, we decided to return

to our roots in Oklahoma as Mid-Continent natural

gas producers. We were convinced that supply-con-

strained U.S. natural gas prices would outperform oil

prices in the years ahead and that tremendous opportu-

nities existed in the Mid-Continent for producing

property acquisitions and corporate consolidations and

Chesapeake 2002 Annual Report

4