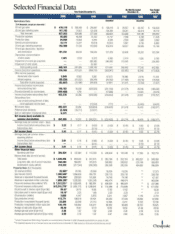

Chesapeake Energy 2000 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2000 Chesapeake Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

|

|

In addition, for the energy industry to generate greater supplies,

more atfention will have to be paid to the cost-benefit relationship of

environmental regulations. For years, our country's policies of favor-

ing a pristine environment while demanding cheap energy have been

on a collision course. A more rational approach is required. We

believe that both environmentalists and policymakers will have to

realize that natural gas is the only fuel that can quickly deliver much

needed new supplies of energy in an environmentally friendly manner.

Natural gas has numerous natural advantages over coal, oil and

renewables and we believe that it can continue to trade at a BTU

premium to competing fuels. By extension, we believe that over time

natural gas producers' stock prices will also be valued at much high-

er multiples in the market. As this summer rolls on and higher elec-

tricity and natural gas prices spread from California throughout the

interconnected western U.S. and on to the Midwest and East Coast,

we believe investors will increasingly appreciate how well

Chesapeake is prepared for this opportunity and is positioned to

profit from these trends.

Chesapeake's Primary Objective

and Business Strategy

Chesapeake primary objective is simple: we desire to be the most

profitable producer of natural gas in the U.S. on a per-unit-of-pro-

duction basis in order to generate the industry's highest returns to

shareholders. Of the more than 200 publicly traded producers listed

on U.S. stock exchanges, Chesapeake is already among the 10 most

profitable by this important measure. As we continue to grow our

asset base and further improve our capital structure, we will continue

advancing toward our goal of being the best in the industry at explor-

ing for, developing, acquiring and producing onshore natural gas.

Chesapeake's strategy for achieving its goal is also straightforward:

using our extensive geological and operational expertise created

through having drilled or acquired over 6,700 wells during the past

12 years, our company will continue to conduct one of the most

technologically sophisticated searches for onshore natural gas in the

U.S. In addition, we will continue to increase our two million acre

leasehold inventory, which contains more than 1,500 additional

drilling opportunities. It is the backbone of our ability to create future

shareholder value. Furthermore, we will continue to aggressively and

economically consolidate smaller asset packages in each of our tour

major core operating areas, with particular emphasis on the key Mid-

Continent area. The combination of these efforts should enable us to

achieve Chesapeake's goal of generating industry-leading returns.

Chesapeake's P4ewest Exploration Project

The Georgetown in Deep Giddings

During the past three years, Chesapeake has transformed itself from

a high-risk, exploration oriented operator in fractured carbonate for-

mations into a low-risk driller and acquirer of Mid-Continent natural

gas reserves. However, just because we have focused on lowering

our risk profile, it would be a mistake to assume we no longer have

an inventory of exciting drilling projects with the opportunity for sig-

nificant production growth. In tact, Chesapeake is one of the top 10

drillers in the U.S. and has a number of high-potential drilling proj-

ects in both the Anadarko and Arkoma Basins of Oklahoma. Typically

drilled to below 15,000', these deep projects in Oklahoma have the

potential to find more than 10 bcte per well.

Chesapeake's project area that is today generating more industry

attention than any other is the Georgetown play in the Deep Giddings

Field in Texas. Many of you may recall that the springboard for

Chesapeake's phenomenal returns to shareholders during 1994-96

(when Chesapeake increased in value by 90-fold and was the best

A

Chesapeake 4