Chesapeake Energy 2000 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2000 Chesapeake Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

|

|

Company Strengths

We believe our past performance and future growth potential are primarily attributable to five

characteristics that distinguish us from other independent oil and natural gas producers:

High-Quality Asset Base. Our properties are characterized by long-lived reserves, established

production profiles and an emphasis on natural gas. Based upon 2000 production and our year-end

reserves, our proved reserves-to-production ratio, or reserve life, is more than ten years. In each of our

four core operating areas, our properties are concentrated in locations that enable us to establish

substantial economies of scale in drilling and production operations and facilitate the application of more

effective reservoir management practices. We intend to continue concentrating our acquisition and

drilling efforts in our four core operating areas, with particular emphasis on the Mid-Continent region

where approximately 74% of our proved reserves, including Gothic's reserves, are located.

Low-Cost Producer. Our high-quality asset base has enabled us to achieve a low operating cost

structure. During 2000, our cash operating costs per unit of production, which consist of general and

administrative expenses and production expenses and taxes, were $0.66 per mcfe. We believe this is one

of the lowest operating cost structures among publicly traded independent oil and natural gas producers.

We operate approximately 71% of our proved reserves, including Gothic's reserves, providing a high

degree of operating flexibility and cost control.

Successful Acquisition Program. Our acquisition program is focused primarily in the Mid-

Continent region. This region is characterized by long-lived natural gas reserves, low lifting costs,

multiple geological targets that provide substantial drilling potential, favorable basis differentials to

benchmark commodity prices, a well-developed oil and gas transportation infrastructure and considerable

potential for further consolidation of assets. Since 1998, we have successfully completed $1.2 billion in

acquisitions at an average cost of $0.98 per mcfe. We believe we are well positioned to continue this

consolidation as a result of our large existing asset base, our corporate presence in Oklahoma City and our

knowledge and expertise in the Mid-Continent.

Large Inventory of Drilling Projects. During the past 12 years, we believe we have been one of the

ten most active drillers in the United States, especially of deep vertical and horizontal wells in challenging

reservoir conditions. As a result of our land acquisition strategy, we have developed an onshore leasehold

position of approximately 2.5 million net acres. In addition, our technical teams have identified over 1,500

exploratory and developmental drillsites, representing more than five years of future drilling opportunities

at our current rate of drilling.

Entrepreneurial Management. Our management team formed Chesapeake in 1989 with an initial

capitalization of $50,000. Through the following years, our management team has guided the company

through operational challenges and extremes of oil and gas prices to create one of the ten largest

independent natural gas producers in the United States with an enterprise value at March 15, 2001 of

$2.7 billion. In addition, through its ownership of approximately 23 million shares of our common stock,

our management has a strong interest in increasing shareholder value.

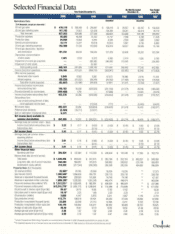

2000 Highlights

Chesapeake's operating results for the year ended December 31, 2000 established several records for our

company:

net income of $456 million (including a $265 million reversal of a tax valuation allowance),

compared to net income of $33 million in 1999,

operating cash flow of $305 million, compared to operating cash flow of $138 million in 1999,

production of 134 bcfe, of which 86% was natural gas, and

proved oil and gas reserves of 1,656 bcfe pro forma for the Gothic acquisition, an increase of 37%

from the year ended December 31, 1999.

During 2000, we also replaced 585 bcfe of proved reserves at a replacement cost of $1.07 per mcfe, pro

forma for the Gothic acquisition.

-2-