Carnival Cruises 2004 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2004 Carnival Cruises annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

|

|

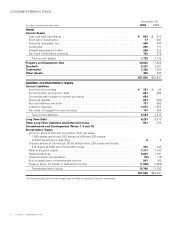

and assets of one company are required to be used to

pay the obligations of the other company, if necessary.

Given the DLC structure as described above, we

believe that providing separate financial statements for

each of Carnival Corporation and Carnival plc would not

present a true and fair view of the economic realities

of their operations. Accordingly, separate financial state-

ments for both Carnival Corporation and Carnival plc

have not been presented.

Simultaneously with the completion of the DLC trans-

action, a partial share offer (“PSO”) for 20% of Carnival

plc’s shares was made and accepted, which enabled

20% of Carnival plc shares to be exchanged for 41.7

million Carnival Corporation shares. The 41.7 million

shares of Carnival plc held by Carnival Corporation as

a result of the PSO, which cost $1.05 billion, are being

accounted for as treasury stock in the accompanying

balance sheets. The holders of Carnival Corporation

shares, including the new shareholders who exchanged

their Carnival plc shares for Carnival Corporation shares

under the PSO, now own an economic interest equal to

approximately 79%, and holders of Carnival plc shares

now own an economic interest equal to approximately

21%, of Carnival Corporation & plc.

The management of Carnival Corporation and

Carnival plc ultimately agreed to enter into the DLC

transaction because, among other things, the creation

of Carnival Corporation & plc would result in a company

with complementary well-known brands operating glob-

ally with enhanced growth opportunities, benefits of

sharing best practices and generating cost savings,

increased financial flexibility and access to capital markets

and a DLC structure, which allows for continued partici-

pation in an investment in the global cruise industry

by Carnival plc’s shareholders who wish to continue to

hold shares in a UK-listed company.

Carnival plc was the third largest cruise company in

the world and operated many well-known global brands

with leading positions in the U.S., UK, Germany and

Australia. The combination of Carnival Corporation with

Carnival plc under the DLC structure has been accounted

for under U.S. generally accepted accounting principles

(“GAAP”) as an acquisition of Carnival plc by Carnival

Corporation pursuant to SFAS No. 141. The purchase

price of $25.31 per share was based upon the average of

the quoted closing market price of Carnival Corporation’s

shares beginning two days before and ending two days

after January 8, 2003, the date the Carnival plc board

agreed to enter into the DLC transaction. The number

of additional shares effectively issued in the combined

entity for purchase accounting purposes was 209.6 million.

In addition, Carnival Corporation incurred $60 million of

direct acquisition costs, which have been included in

the purchase price. The aggregate purchase price of

$5.36 billion, computed as described above, was allo-

cated to the assets and liabilities of Carnival plc as follows

(in millions):

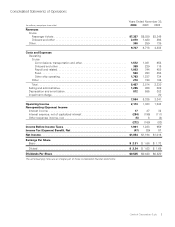

Ships. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 4,669

Ships under construction . . . . . . . . . . . . . . . . . . . . . 233

Other tangible assets . . . . . . . . . . . . . . . . . . . . . . . 866

Goodwill . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,387

Trademarks(a) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,237

Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (2,939)

Other liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . (1,095)

$ 5,358

(a) Trademarks are non-amortizable and represent the Princess,

P&O Cruises, P&O Cruises Australia and AIDA trademarks’

estimated fair values.

The information presented below gives pro forma

effect to the DLC transaction between Carnival Corporation

and Carnival plc. Management has prepared the pro

forma information based upon the companies’ reported

financial information and, accordingly, the pro forma

information should be read in conjunction with the com-

panies’ financial statements.

As noted above, the DLC transaction has been

accounted for as an acquisition of Carnival plc by Carnival

Corporation, using the purchase method of accounting.

Carnival plc’s accounting policies have been conformed

to Carnival Corporation’s policies. Carnival plc’s reporting

period has been changed to Carnival Corporation’s report-

ing period, and the pro forma information presented below

covers the same periods of time for both companies.

Carnival Corporation & plc 15