Bridgestone 2002 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2002 Bridgestone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

|

|

03

lot of the equipment at those plants will

be inadequate to serve future demand.

Writing down that equipment reduces the

depreciation burden at our European sub-

sidiary and aligns the cost structure there

with the company’s actual circumstances.

The European write-downs are therefore

similar to write-downs of fixed assets in

the Americas in 2001.

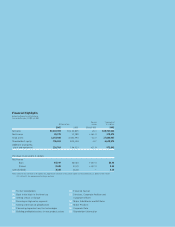

Unit sales of tires by Bridgestone

Corporation and its subsidiaries in 2002

increased in the Americas, in Europe and

in other markets besides Japan, and they

were basically unchanged in Japan. Sales

and operating income increased overall in

the tire segment. In diversified products,

operating income increased solidly on a

small gain in sales. You will find a detailed

account of our sales and earnings perfor-

mance and projections by business segment

and by geographical segment on pages 18

to 23 of this report.

In 2003, we expect to achieve an

increase of more than 50% in net

income while maintaining sales at approxi-

mately the same level as in 2002. Our

expectation of earnings growth is on the

basis of our American subsidiary’s continu-

ing progress in revitalizing its operations,

our European subsidiary’s progress in

strengthening its competitive position,

our progress improving our earnings struc-

ture in Japan and our progress in expand-

ing operations profitably in emerging

markets.

Continuing Recovery in the Americas

The return to profitability at our American

subsidiary in 2002 vindicated the sweeping

measures taken there in 2001. Those

measures included (1) reorganizing North

American operations to sharpen the focus

on management responsibility for prof-

itability in different sectors, such as North

American tire operations, retail operations

and diversified products operations;

(2) closing the Decatur, Illinois, tire

plant—our subsidiary’s oldest North

American plant—which has reduced fixed

costs and raised overall capacity utiliza-

tion; (3) writing down fixed assets, which

has reduced depreciation expense; and

(4) using an infusion of capital from the

parent company to place North and Latin

American operations on a stronger finan-

cial footing, which has included repaying

a great deal of interest-bearing debt and

thereby reducing interest expense greatly.

The core challenge for our American

subsidiary is to achieve sustainable prof-

itability in its North American tire manu-

facturing and wholesaling operations.

Those operations remain the weakest link

in an otherwise robust portfolio of busi-

nesses. Our subsidiary’s North American

network of more than 2,200 company-

owned stores—the world’s largest tire and

automotive service network—remains prof-

itable. The North America–based diversi-

fied products operations—including roofing

materials and air springs—are profitable

and growing. The Latin American tire

operations are—notwithstanding the recent

economic instability in Argentina and

Venezuela—fundamentally profitable and

extremely promising.

Raising profitability in our subsidiary’s

North American tire operations will

depend on several factors, including ensur-

ing that those operations develop a more

globally competitive cost structure through

heightened productivity and the effective

management of medical and pension

costs. In addition, the subsidiary needs

to maximize revenues by shifting its sales

portfolio toward higher-value products. It

is doing that by adopting an increasingly

selective approach in original equipment

business and by promoting high-end prod-

ucts effectively in the replacement market.

A New Beginning in Europe

We have abided by a policy of insisting

that our subsidiary operations in each

region pay their own way—that they

finance their investment programs with

internally generated cash flow. In retro-

spect, that policy has been unrealistic

in regard to our European subsidiary’s

operations. That subsidiary serves the

world’s most competitive tire market.

For our European subsidiary to fulfill its

immense potential, it needed and deserved

a boost from the parent company. We

provided that boost at the end of 2002.

In December, we furnished our

European subsidiary with a capital infusion

of E400 million ($416 million) to fund

We expect net income to increase

more than 50% in 2003.