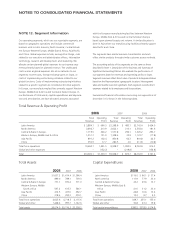

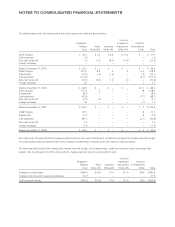

Avon 2008 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2008 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

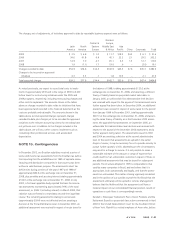

Weighted-average assumptions used to determine net cost recorded in the Consolidated Statements of Income for the years ended

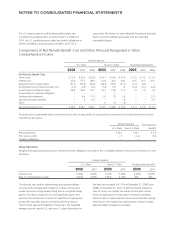

December 31 were as follows:

Pension Benefits

U.S. Plans Non-U.S. Plans Postretirement Benefits

2008 2007 2006 2008 2007 2006 2008 2007 2006

Discount rate 6.20% 5.90% 5.50% 5.56% 4.93% 5.01% 6.26% 5.90% 6.33%

Rate of compensation increase 4.00 5.00 6.00 3.10 2.99 3.14 N/A N/A N/A

Rate of return on assets 8.00 8.00 8.00 7.31 6.85 6.97 N/A N/A N/A

In determining the net cost for the year ended December 31,

2008, the assumed rate of return on assets globally was 7.66%,

which represents the weighted-average rate of return on all plan

assets, including the U.S. and non-U.S. plans.

The majority of our pension plan assets relate to the U.S. pension

plan. The assumed rate of return for determining 2008 net costs for

the U.S. plan was 8.0%. Historical rates of return for the U.S. plan

for the most recent 10-year and 20-year periods were 2.0% and

7.6%, respectively. In the U.S plan, our asset allocation policy has

favored U.S. equity securities, which have lost .7% and returned

8.4%, respectively, over the ten-year and 20-year period.

In addition, the current rate of return assumption for the U.S.

plan was based on an asset allocation of approximately 35% in

corporate and government bonds and mortgage-backed

securities (which are expected to earn approximately 4% to 6%

in the long term) and 65% in equity securities (which are

expected to earn approximately 8% to 10% in the long term).

Similar assessments were performed in determining rates of re-

turn on non-U.S. pension plan assets, to arrive at our weighted-

average rate of return of 7.66% for determining 2008 net cost.

Plan Assets

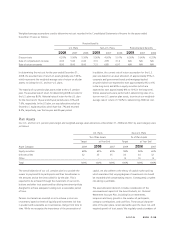

Our U.S. and non-U.S. pension plans target and weighted-average asset allocations at December 31, 2008 and 2007, by asset category were

as follows:

U.S. Plans Non-U.S. Plans

% of Plan Assets % of Plan Assets

Target at Year End Target at Year End

Asset Category 2009 2008 2007 2009 2008 2007

Equity securities 68% 65% 65% 58% 56% 60%

Debt securities 32 35 35 34 34 32

Other – – – 8 10 8

Total 100% 100% 100% 100% 100% 100%

The overall objective of our U.S. pension plan is to provide the

means to pay benefits to participants and their beneficiaries in

the amounts and at the times called for by the plan. This is

expected to be achieved through the investment of our contri-

butions and other trust assets and by utilizing investment policies

designed to achieve adequate funding over a reasonable period

of time.

Pension trust assets are invested so as to achieve a return on

investment, based on levels of liquidity and investment risk that

is prudent and reasonable as circumstances change from time to

time. While we recognize the importance of the preservation of

capital, we also adhere to the theory of capital market pricing

which maintains that varying degrees of investment risk should

be rewarded with compensating returns. Consequently, prudent

risk-taking is justifiable.

The asset allocation decision includes consideration of the

non-investment aspects of the Avon Products, Inc. Personal

Retirement Account Plan, including future retirements,

lump-sum elections, growth in the number of participants,

company contributions, and cash flow. These actual character-

istics of the plan place certain demands upon the level, risk, and

required growth of trust assets. We regularly conduct analyses of

A V O N 2008 F-23