Tiscali 2007 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2007 Tiscali annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

|

|

18

Broadband: 2007, focus on organic growth

Wholesale

model: OLOs resell broadband access provided by the former incumbents. In this market,

operators are unable to exploit the competitive advantage of owning proprietary networks - which squeezes

margins - and they also have no control over the product offered to the end-user.

Bit-stream

model: the interconnection to the network of the national telecoms operators is charged at

cost. Bit-stream allows alternative operators such as Tiscali to use their own networks, which means they

only have to pay the national carrier for access to the local loop and backhauling services (transmission

of traffic to the interconnection point).

Unbundling

model: OLOs can access the local loop by investing in local networks. Unbundled services

allow operators to expand their margins to over 70% and to control the quality of the service provided to

final customers.

IMPATTO POSITIVO SU ARPU E PROFITABILITÀ

19%

25%

56%

ULL

Bit-stream

Wholesale

70%

30%Gross Margin

% of ADSL revenues YE 2006

GROSS MARGIN IMPROVEMENTULL: A SUSTAINABLE STRATEGY

46%

26%

28%

ULL

Bit-stream

Wholesale

70%

30%Gross Margin

% of ADSL revenues YE 2007

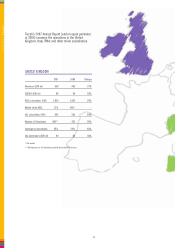

As of 31 December 2007, Tiscali had reached:

3486 co-locations in Italy,

reaching a 50% market coverage

3800 co-locations in the UK,

with a 55% market coverage

TISCALI GROUP