Food Lion 2008 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2008 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

|

|

Intangible Assets

Intangible assets include trade names and favorable lease rights that have been acquired in business combinations, computer software, various licenses and

prescription files separately acquired. Separately acquired intangible assets are initially recognized at cost, while intangible assets acquired as part of a busi-

ness combination are measured initially at fair value (see “Business Combinations and Goodwill”). Expenditure on advertising or promotional activities, training

activities and start-up activities, and on relocating or reorganizing part or all of an entity are recognized as an expense as incurred, i.e. when Delhaize Group has

access to the goods or has received the services in accordance with the underlying contract. Intangible assets are subsequently carried at cost less accumulated

amortization and accumulated impairment losses. Amortization begins when the asset is available for use, as intended by management. Residual values of

intangible assets are assumed to be zero and are reviewed at each financial year-end.

Costs associated with maintaining computer software programs are recognized as an expense as incurred. Development costs that are directly attributable to

the design and testing of identifiable and unique “for-own-use-software” controlled by the Group are recognized as intangible assets when the following criteria

are met:

• itistechnicallyfeasibletocompletethesoftwareproductsothatitwillbeavailableforuse;

• managementintendstocompletethesoftwareproductanduseit;

• thereisanabilitytousethesoftwareproduct;

• itcanbedemonstratedhowthesoftwareproductwillgenerateprobablefutureeconomicbenefits;

• adequatetechnical,financialandotherresourcestocompletethedevelopmentandtousethesoftwareproductareavailable;and

• theexpenditureattributabletothesoftwareproductduringitsdevelopmentcanbereliablymeasured.

Directly attributable costs capitalized as part of the software product include software development employee costs and directly attributable overhead costs.

Other development expenditures that do not meet these criteria are recognized as an expense as incurred. Development costs previously recognized as an

expense are not recognized as an asset in a subsequent period.

Intangible assets with definite lives are amortized on a straight-line basis over their estimated useful lives. The useful lives of intangible assets with definite lives

are reviewed annually and are as follows:

• Prescriptionfiles 15years

• Favorableleaserights Remainingleaseterm

• Computersoftware 3to5years

• Other intangible assets 3 to 15 years

Intangible assets with indefinite useful lives are not amortized, but are annually tested for impairment and when there is an indication that the asset may be

impaired. The Group believes that acquired and used trade names have indefinite lives because they contribute directly to the Group’s cash flows as a result

of recognition by the customer of each banner’s characteristics in the marketplace. There are no legal, regulatory, contractual, competitive, economic or other

factors that limit the useful life of the trade names. The assessment of indefinite life is reviewed annually to determine whether the indefinite life assumption

continues to be supportable. Changes, if any, would result in prospective amortization.

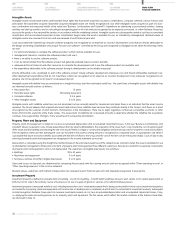

Property, Plant and Equipment

Property, plant and equipment is stated at cost less accumulated depreciation and accumulated impairment losses, if any (see “Business Combinations and

Goodwill” above). Acquisition costs include expenditures that are directly attributable to the acquisition of the asset. Such costs include the cost of replacing part

of the asset and dismantling and restoring the site of an asset if there is a legal or constructive obligation and borrowing costs for long-term construction projects

if the recognition criteria are met. Subsequent costs are included in the asset’s carrying amount or recognized as a separate asset, as appropriate, only when it

is probable that future economic benefits associated with the item will flow to the Group and the cost of the item can be measured reliably. Costs of day-to-day

servicing of property, plant and equipment are recognized in the income statement as incurred.

Depreciation is calculated using the straight-line method based on the estimated useful lives of the related assets and starts when the asset is available for use

as intended by management. When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate components

of property, plant and equipment. Land is not depreciated. The useful lives of tangible fixed assets are as follows:

• Buildings 33to40years

• Machineryandequipment 3to14years

• Furnitures,vehiclesandothertangiblefixedassets 5to10years

Gains and losses on disposals are determined by comparing the proceeds with the carrying amount and are recognized within “Other operating income” or

“Other operating expenses” in the income statement.

Residual values, useful lives and method of depreciation are reviewed at each financial year-end, and adjusted prospectively, if appropriate.

Investment Property

Investment property is defined as property (land or building - or part of a building - or both) held by Delhaize Group to earn rentals or for capital appreciation or

both, but not for sale in the ordinary course of business or for use in supply of goods or services or for administrative purposes.

Investment property is measured initially at cost, including transaction costs. Investment property that is being constructed for future use as investment property is

accounted for as property, plant and equipment until construction or development is completed, at which time it is reclassified to investment property. Subsequent

to initial recognition, Delhaize Group elects to measure investment property at cost, less accumulated depreciation and accumulated impairment losses, if any,

i.e. applying the same accounting policies as for property, plant and equipment. The fair values, which reflect the market conditions at the balance sheet date,

are disclosed in Note 10.

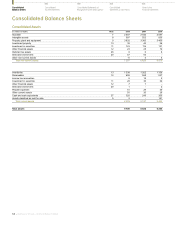

Consolidated

Balance Sheets

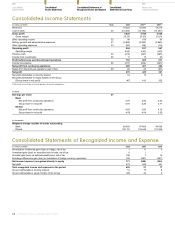

Consolidated

Income Statements

Consolidated Statements of

Recognized Income and Expense

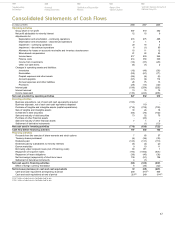

Consolidated

Statements of Cash Flows

70 - Delhaize Group - Annual Report 2008

Notes to the

Financial Statements