AT&T Uverse 2006 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2006 AT&T Uverse annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

42 : :

2006 AT&T Annual Report

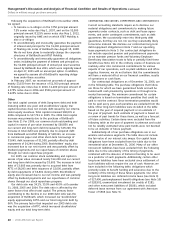

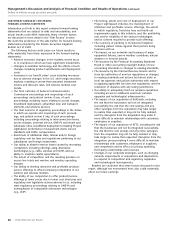

Maturity

After Fair Value

2007 2008 2009 2010 2011 2011 Total 12/31/06

Interest Rate Derivatives

Interest Rate Swaps:

Receive Fixed/Pay Variable Notional Amount — — — — $1,250 $2,000 $3,250 $(36)

Variable Rate Payable1 6.3% 6.1% 6.1% 6.2% 6.2% 6.0%

Weighted-Average Fixed Rate Receivable 6.0% 6.0% 6.0% 6.0% 6.0% 5.9%

1Interest payable based on current and implied forward rates for Three or Six Month LIBOR plus a spread ranging between approximately 64 and 170 basis points.

We had fair value interest rate swaps with a notional value of

$5,050 at December 31, 2006, and $4,250 at December 31,

2005, with a net carrying and fair value liability of $80 and

$16, respectively. In 2006, we had $1,000 of swaps mature

related to our repayment of the underlying security. The net

fair value liability at December 31, 2006, was comprised of a

liability of $86 and an asset of $6. The net fair value liability

at December 31, 2005, was comprised of a liability of $33 and

an asset of $17.

Included in the fair value interest rate swap notional value

for 2006 were interest rate swaps with a notional amount of

$1,800, which was acquired as a result of our acquisition of

BellSouth on December 29, 2006. These swaps were unwound

in January 2007 and are therefore excluded from the

sensitivity table above.

Foreign Exchange Forward Contracts The fair value of

foreign exchange contracts is subject to changes in foreign

currency exchange rates. For the purpose of assessing specific

risks, we use a sensitivity analysis to determine the effects

that market risk exposures may have on the fair value of our

financial instruments and results of operations. To perform the

sensitivity analysis, we assess the risk of loss in fair values

from the effect of a hypothetical 10% change in the value

of foreign currencies (negative change in the value of the

U.S. dollar), assuming no change in interest rates. See Note 8

to the consolidated financial statements for additional

information relating to notional amounts and fair values

of financial instruments.

For foreign exchange forward contracts outstanding at

December 31, 2006, assuming a hypothetical 10% depreciation

of the U.S. dollar against foreign currencies from the prevailing

foreign currency exchange rates, the fair value of the foreign

exchange forward contracts (net liability) would have decreased

approximately $30. Because our foreign exchange contracts

are entered into for hedging purposes, we believe that these

losses would be largely offset by gains on the underlying

transactions.

The risk of loss in fair values of all other financial instru-

ments resulting from a hypothetical 10% change in market

prices was not significant as of December 31, 2006.

QUAL I TATIV E I NFO RMATI ON AB OUT MA RKET RISK

Foreign Exchange Risk From time to time, we make invest-

ments in businesses in foreign countries, are paid dividends

and receive proceeds from sales or borrow funds in foreign

currency. Before making an investment, or in anticipation of

a foreign currency receipt, we often will enter into forward

foreign exchange contracts. The contracts are used to provide

currency at a fixed rate. Our policy is to measure the risk of

adverse currency fluctuations by calculating the potential

dollar losses resulting from changes in exchange rates that

have a reasonable probability of occurring. We cover the

exposure that results from changes that exceed acceptable

amounts. We do not speculate in foreign exchange markets.

We have also entered into foreign currency contracts to

minimize our exposure to risk of adverse changes in currency

exchange rates. We are subject to foreign exchange risk for

foreign currency-denominated transactions, such as debt

issued, recognized payables and receivables and forecasted

transactions. At December 31, 2006, our foreign currency

exposures were principally Euros, British pound sterling,

Danish krone and Japanese Yen.

Interest Rate Risk We issue debt in fixed and floating

rate instruments. Interest rate swaps are used for the purpose

of controlling interest expense by managing the mix of fixed

and floating rate debt. Interest rate forward contracts are

utilized to hedge interest expense related to debt financing.

We do not seek to make a profit from changes in interest

rates. We manage interest rate sensitivity by measuring

potential increases in interest expense that would result from

a probable change in interest rates. When the potential

increase in interest expense exceeds an acceptable amount,

we reduce risk through the issuance of fixed rate (in lieu of

variable rate) instruments and the purchase of derivatives.

Management’s Discussion and Analysis of Financial Condition and Results of Operations (continued)

Dollars in millions except per share amounts

Interest Rate Sensitivity The principal amounts by

expected maturity, average interest rate and fair value of our

liabilities that are exposed to interest rate risk are described

in Notes 7 and 8. Following are our interest rate derivatives,

subject to interest rate risk as of December 31, 2006.

The interest rates illustrated in the interest rate swaps

section of the table below refer to the average expected

rates we would receive and the average expected rates we

would pay based on the contracts. The notional amount is

the principal amount of the debt subject to the interest rate

swap contracts. The net fair value asset (liability) represents

the amount we would receive or pay if we had exited the

contracts as of December 31, 2006.