Visa 2009 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2009 Visa annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

Table of Contents

Competition

We compete in the global payment marketplace against all forms of payment, including paper-based forms (principally cash and checks), card-based

payments (including credit, charge, debit, ATM, prepaid, private-label and other types of general-purpose and limited-use cards) and other electronic

payments (including wire transfers, electronic benefits transfers, automatic clearing house, or ACH, payments and electronic data interchange).

Within the general purpose payment card industry, we face substantial and intense competition worldwide in the provision of payments services to

financial institution customers and their cardholder merchants. The leading global card brands in the general purpose payment card industry are Visa,

MasterCard, American Express and Diners Club. Other general-purpose card brands are more concentrated in specific geographic regions, such as JCB in

Japan and Discover in the United States. In certain countries, our competitors have leading positions, such as China UnionPay in China, which is the sole

domestic inter-bank bankcard processor and operates the sole domestic bankcard acceptance mark in China due to local regulation. We also compete against

private-label cards, which can generally be used to make purchases solely at the sponsoring retail store, gasoline retailer or other merchant.

In the debit card market segment, Visa and MasterCard are the primary global brands. In addition, our Interlink and Visa Electron brands compete with

Maestro, owned by MasterCard, and various regional and country-specific debit network brands. In addition to our PLUS brand, the primary cash access card

brands are Cirrus, owned by MasterCard, and many of the online debit network brands referenced above. In many countries, local debit brands are the primary

brands, and our brands are used primarily to enable cross-border transactions, which typically constitute a small portion of overall transaction volume. See

Item 8—Financial Statements and Supplementary Data for financial information about geographic areas.

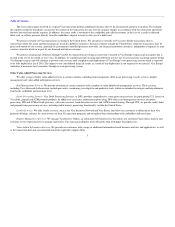

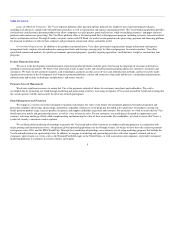

Based on payments volume, total volume, number of transactions and number of cards in circulation, Visa is the largest retail electronic payments

network in the world. The following chart compares our network with those of our major general-purpose payment network competitors for calendar year

2008:

Company

Payments

Volume

Total

Volume

Total

Transactions Cards

(billions) (billions) (billions) (millions)

Visa Inc.(1) $ 2,727 $ 4,346 56.7 1,717

MasterCard 1,900 2,533 29.9 981

American Express 673 683 5.3 92

Discover 106 120 1.6 57

JCB 63 68 0.7 60

Diners Club 30 31 0.2 7

(1) Visa Inc. figures as reported on form 8-K filed with the SEC on April 29, 2009.

Source: The Nilson Report, issue 924 (April 2009) and issue 925 (May 2009).

Note: Visa Inc. figures exclude Visa Europe. Figures for competitors include their respective European operations. Visa figures include Visa, Visa Electron,

and Interlink brands. The Visa card figure includes PLUS-only cards (with no Visa logo) in all regions except the United States, but PLUS cash volume is not

included. Domestic China figures including commercial funds transfers are excluded. MasterCard includes PIN-based debit card figures on MasterCard cards,

but not Maestro or Cirrus figures. American Express includes business from third-party issuers. JCB figures are for April 2007 through March 2008, but cards

are as of September 2008. Transaction figures are estimates. Figures include business from third-party issuers.

13