Valero 2005 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2005 Valero annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

|

|

VA L E R O E N E R G Y C O R P O R AT I O N 15

Never afraid to take a calculated risk,

Valero executives made a fortuitous bet when

the company entered the refining business

more than 20 years ago.

They predicted that as global oil consump-

tion rose, it would be met with more plentiful

heavy, sour feedstocks. Seeing an opportunity

to gain a competitive advantage, Valero config-

ured its refining system to process these harder-

to-refine feedstocks that sell at a discount to

sweet crude oil.

Over the years, this bet has paid off hand-

somely!

As oil demand has continued to grow, the

incremental demand has been increasingly

met by medium and heavier sour crude oils.

Because of the limited refining capacity capable

of upgrading these crudes, demand hasn’t been

as strong for sour crude oils and as a result,

supplies have been increasingly more plentiful,

resulting in big discounts for complex refiners

like Valero.

At the same time, demand for sweet crude oils

– fueled by the ongoing domestic and global

movement toward cleaner fuels – has been on

the rise. To meet the new low-sulfur specifica-

tions for fuel, many refiners are relying on

sweet crudes, which has further widened the

sweet/sour price differential.

And, of course, these bullish fundamentals

have played right into Valero’s hands!

“With a focus on the harder-to-refine sour

types of crude oil, Valero’s profits are being

boosted by a glut in supplies of sour crude,

which means its feedstock is relatively

cheap…If I had to pick one (to invest in out

of all refiners), given its scale, ambition, and

lower valuation, it would be Valero.”

-- BusinessWeek, October 24, 2005

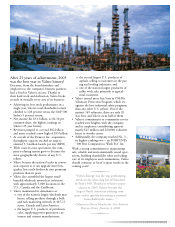

RESID

MAYA

ARAB LIGHT/MEDIUM

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

2002 2003 2004 2005

RECORD DISCOUNTS

RESIDUAL FUEL AND SOUR CRUDE OIL DISCOUNTS

TO WEST TEXAS INTERMEDIATE CRUDE

Wade Upton, Senior Vice

President – Transportation

Services [left], and Bob

Beadle, Senior Vice President

– Crude & Feedstock Supply

& Trading [center], work

together to secure and

ship the most economical

crude oils and feedstocks

to Valero’s 18 refineries.

Processing deeply discounted

feedstocks was a big advan-

tage in 2005 as discounts

reached record levels.

The discounts for the heavier, sour feedstocks

– which make up over 60 percent of Valero’s

feedstock slate – widened to record levels in

2005 and early 2006.

Recent acquisitions and internal projects have

given Valero even more leverage to these dis-

counts. For example, the company estimates

that it will process an additional 250,000 BPD

of medium and heavy crude in 2006 as a result

of its acquisition of the Port Arthur refinery

alone.

Internal projects like the 2003 construction of

the 45,000-BPD coker at the Valero Texas City

Refinery have strengthened this advantage. The

coker’s original economics were based upon

an historic $6-7 Maya discount (compared to

the benchmark West Texas Intermediate), but

in 2005 that discount actually averaged nearly

$16!

Valero’s bet should continue to pay off as dis-

counts for heavy, sour feedstocks are expected

to stay wide. Because Valero has the most con-

version capacity of any U.S. refiner, this advan-

tage should continue to give the company a

real hand up on the competition!