Tyson Foods 2005 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2005 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

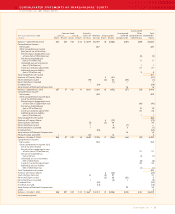

>> NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

TYSON FOODS, INC. 2005 ANNUAL REPORT

>>>>>>>>>>>>>>>>

>>>>>>>>>>>>>>>>

Tyson Foods, Inc. >> 43

affects earnings (for grain commodity hedges when the chickens

that consumed the hedged grain are sold). The remaining cumula-

tive gain or loss on the derivative instrument in excess of the

cumulative change in the present value of the future cash flows

of the hedged item, if any, is recognized in earnings during the

period of change. Ineffectiveness recorded related to the

Company’s cash flow hedges was not significant during

fiscal years 2005, 2004 or 2003.

Derivative products related to grain procurement, such as futures

and option contracts that meet the criteria for SFAS No. 133 hedge

accounting, are considered cash flow hedges, as they hedge against

changes in the amount of future cash flows related to commodities

procurement. The Company applies SFAS No. 133 hedge accounting

to derivative products related to grain procurement that are hedg-

ing physical grain contracts that have previously been purchased. The

Company does not purchase derivative products related to grain

procurement in excess of its physical grain consumption require-

ments. The Company’s grain procurement hedging activities are

for the grain commodity purchase price only and do not hedge

other components of grain cost such as basis differential and

freight costs. The after tax losses recorded in other comprehensive

income (loss) at October 1, 2005, related to cash flow hedges, were

$5 million. These losses will be recognized within the next 12 months.

The Company generally does not hedge cash flows related to com-

modities beyond 12 months. Of this amount, the portion resulting

from the Company’s open mark-to-market SFAS No. 133 hedge

positions was not significant as of October 1, 2005.

Fair value hedges: The Company designates certain futures

contracts as fair value hedges of firm commitments to purchase

livestock for slaughter and natural gas for the operation of its

plants. From time to time, the Company also enters into foreign

currency forward contracts to hedge changes in fair value of

receivables and purchase commitments arising from changes in

the exchange rates of foreign currencies; however, the Company

has not entered into any material contracts in fiscal years 2005

and 2004. Changes in the fair value of a derivative that is highly

effective and that is designated and qualifies as a fair value hedge,

along with the loss or gain on the hedged asset or liability that is

attributable to the hedged risk (including losses or gains on firm

commitments), are recorded in current period earnings. Ineffec-

tiveness results when the change in the fair value of the hedge

instrument differs from the change in fair value of the hedged

item. Ineffectiveness recorded related to the Company’s fair value

hedges was not significant during fiscal 2005, 2004 or 2003.

Undesignated positions: The Company holds positions as part of

its risk management activities, primarily certain grain, livestock and

natural gas futures for which it does not apply SFAS No. 133 hedge

accounting, but instead marks these positions to fair value through

earnings at each reporting date. Changes in market value of deriva-

tives used in the Company’s risk management activities surrounding

inventories on hand or anticipated purchases of inventories or

supplies are recorded in cost of sales. Changes in market value

of derivatives used in the Company’s risk management activities

surrounding forward sales contracts are recorded in sales. The

Company generally does not enter into undesignated positions

beyond 12 months.

Based on the Company’s evaluation of the grain markets, the Com-

pany has at times entered into a portion of its derivative products

related to grain procurement prior to purchasing the physical grain

contracts. The Company has not applied SFAS No. 133 hedge

accounting treatment for these derivative positions. In connection

with these risk management activities, the Company recognized

pretax net gains of approximately $2 million and $58 million in cost

of sales for fiscal years ended October 1, 2005, and October 2, 2004,

respectively. The prior year derivative gains were primarily due to

the increase in grain futures prices during the second quarter of

fiscal 2004 and the Company having a higher number of derivative

positions in place at that time as compared to the current year.

Additionally, the Company enters into certain forward sales of

boxed beef and pork at fixed prices and has positions in livestock

futures to mitigate the market risk associated with these fixed price

forward sales. The fixed price sales contract locks in the proceeds

from a sale in the future, although, the cost of the livestock and the

related boxed beef and pork market prices at the time of the sale

will vary from this fixed price, creating market risk. Therefore, as

fixed forward sales are entered into, the Company also enters

into the appropriate number of livestock futures positions. The

Company believes this is an effective economic hedge; however,

the correlation does not qualify for SFAS No. 133 hedge accounting.

Consequently, changes in market value of the open livestock futures

positions are marked to market and reported in earnings at each

reporting date even though the economic impact of the Company’s

fixed sales price being above or below the market price is only real-

ized at the time of sale. In connection with these livestock futures,

the Company recorded net losses of $4 million for the fiscal year

ended October 1, 2005, which included an unrealized pretax gain on

open mark-to-market futures positions of approximately $17 million.

The Company recorded net gains of $5 million for the fiscal year

ended October 2, 2004.