Petsmart 2008 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2008 Petsmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

|

|

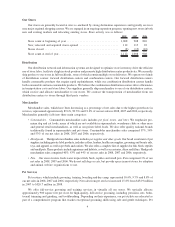

in the United States own a pet. In total, there are approximately 88 million cats and 75 million dogs owned as pets in

the United States.

The pet industry can be divided into the following categories: food and treats, supplies and medicines,

veterinary care, pet services (such as grooming and boarding) and purchases of pets. The APPA estimates that food

and treats for dogs and cats are the largest volume categories of pet-related products and, in calendar year 2008,

approximated $16.8 billion in sales, or 38.9% of the market.

Pet supplies and medicine sales account for approximately 23.1%, or $10.0 billion, of the market. These sales

include dog and cat toys, collars and leashes, cages and habitats, books, vitamins and supplements, shampoos, flea

and tick control and aquatic supplies. Veterinary care, pet services, and purchases of pets represent approximately

25.7%, 7.4% and 4.9%, respectively, of the market.

Competition

Based on total net sales, we are North America’s leading specialty retailer of products, services and solutions

for the lifetime needs of pets. The pet products retail industry is highly competitive and can be organized into eight

different categories:

• Warehouse clubs and other mass merchandisers;

• Supermarkets (grocery stores);

• Specialty pet supply stores;

• Independent pet stores;

• Veterinarians;

• General retail merchandisers;

• Catalog retailers; and

• E-commerce retailers.

We believe the principal competitive factors influencing our business are product selection and quality,

convenience of store locations, store environment, customer service, price and availability of other services. Many

premium pet food brands, which offer higher levels of nutrition than non-premium brands, are not currently sold

through supermarkets, warehouse clubs and other mass and general retail merchandisers due to manufacturers’

restrictions, but are sold primarily through specialty pet supply stores, veterinarians and farm and feed stores. We

believe our pet services business is a competitive advantage that cannot be easily duplicated. We believe we

compete effectively in our various markets; however, some of our supermarket, warehouse club and other mass and

general retail merchandise competitors are much larger in terms of overall sales volume and may have access to

greater capital.

Our Strategy

Our strategy is to be the preferred provider for the lifetime needs of pets. Our primary initiatives include:

Add stores in existing multi-store, new multi-store and new single-store markets. Our expansion strategy

includes increasing our share in existing multi-store markets, penetrating new multi-store and single-store markets

and achieving operating efficiencies and economies of scale in distribution, information systems, procurement,

marketing and store operations. During 2008, we opened 104 net new stores, and in 2009, we expect to open

approximately 40 net new stores. In 2009, we plan to slow our store growth by about 60% as we work to balance

investing for the future and maximizing our greatest opportunity to deliver consistent stockholder returns.

Provide the right store format to meet the needs of our customers. We completed the conversion of our store

base to a specialty store format in 2003. We believe our reformatted stores, combined with our other strategic

initiatives, contribute to higher comparable store sales growth, profitability and return on investment. We

continually evaluate our store format to ensure we are meeting the needs and expectations of our customers,

2