Pep Boys 2006 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2006 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

27

market price of our underlying stock on the date of the grant. The pricing model and generally

accepted valuation techniques require management to make assumptions and to apply judgment to

determine the fair value of our awards. These assumptions and judgments include the expected life

of stock options, expected stock price volatility, future employee stock option exercise behaviors

and the estimate of award forfeitures. We do not believe there is a reasonable likelihood there will

be a material change in the future estimates or assumptions we use to determine stock-based

compensation expense. However, if actual results are different from these assumptions, the share-

based compensation expense reported in our financial statements may not be representative of the

actual economic cost of the share-based compensation. In addition, significant changes in these

assumptions could materially impact our share-based compensation expense on future awards.

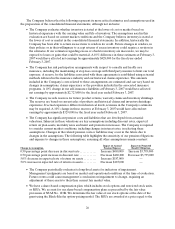

A 10% change in our share-based compensation expense for the fiscal year ended February 3,

2007 would have affected net income by approximately $97,000 for the fiscal year ended

February 3, 2007.

•The Company is required to estimate its income taxes in each of the jurisdictions in which it

operates. This requires the Company to estimate its actual current tax exposure together with

assessing temporary differences resulting from differing treatment of items, such as depreciation of

property and equipment and valuation of inventories, for tax and accounting purposes. The

Company determines its provision for income taxes based on federal and state tax laws and

regulations currently in effect, some of which have been recently revised. Legislation changes

currently proposed by certain states in which we operate, if enacted, could increase our transactions

or activities subject to tax. Any such legislation that becomes law could result in an increase in our

state income tax expense and our state income taxes paid, which could have a material effect on our

net income.

The temporary differences between the book and tax treatment of income and expenses result in

deferred tax assets and liabilities, which are included within our consolidated balance sheets. We must then

assess the likelihood that our deferred tax assets will be recovered from future taxable income. To the

extent we believe that recovery is not more likely than not, we must establish a valuation allowance. To the

extent we establish a valuation allowance or change the allowance in a future period, income tax expense

will be impacted. Actual results could differ from this assessment if adequate taxable income is not

generated in future periods. Net deferred tax liabilities as of February 3, 2007 and January 28, 2006 totaled

$28,931,000 and $18,354,000, respectively, representing approximately 2.4% and 1.5% of liabilities,

respectively.

RECENT ACCOUNTING STANDARDS

In February 2006, the FASB issued SFAS No. 155, “Accounting for Certain Hybrid Financial

Instruments—an amendment of FASB Statements No. 133 and 140.” This statement simplifies accounting

for certain hybrid instruments currently governed by SFAS No. 133, “Accounting for Derivative

Instruments and Hedging Activities,” or SFAS No. 133, by allowing fair value remeasurement of hybrid

instruments that contain an embedded derivative that otherwise would require bifurcation. SFAS No. 155

also eliminates the guidance in SFAS No. 133 Implementation Issue No. D1, “Application of Statement

133 to Beneficial Interests in Securitized Financial Assets,” which provides such beneficial interests are not

subject to SFAS No. 133. SFAS No. 155 amends SFAS No. 140, “Accounting for Transfers and Servicing of

Financial Assets and Extinguishments of Liabilities—a Replacement of FASB Statement No. 125,” by

eliminating the restriction on passive derivative instruments that a qualifying special-purpose entity may

hold. SFAS No. 155 is effective for financial instruments acquired or issued after the beginning of our

fiscal year 2007. We are currently evaluating the impact of SFAS No. 155 and will adopt the standard

February 4, 2007.