Napa Auto Parts 2002 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2002 Napa Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

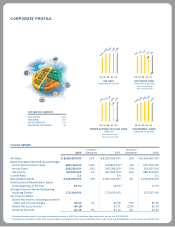

Total sales reached $8.25 billion in 2002, up slightly compared

to the previous year. Net earnings were $367 million, an increase

of 2%. Earnings on a per share basis were $2.10 compared to

the $2.08 produced in 2001. The earnings number for 2002 is

before the cumulative effect of a change in accounting principle

and the 2001 earnings figure excludes the effect of non–recur-

ring charges taken in the final quarter of that year. After the

cumulative effect adjustment described in the next paragraph,

we had a net loss in 2002 of $27.6 million and in 2001, net

income of $297.1 million including the effect of the non-recur-

ring charges.

As we mentioned in our 2002 first quarter report, we recorded

a non-cash charge of $395 million as of January 1, 2002 related

to our goodwill impairment. This adjustment resulted from the

completion of impairment testing in conjunction with the new

Statement of Financial Accounting Standard No. 142, “Goodwill

and Other Intangible Assets”. The charge was recorded as a

cumulative effect of a change in accounting. The majority of

the goodwill written down related to acquisitions made in

1998 and 1999 and under prior accounting standards would

have been amortized over an extended period of time. Our core

U.S. operations for NAPA, Motion and S.P. Richards were

not affected by this change and we continue to have a positive

outlook on the operations that were affected by this change.

Financial Strength

The Company’s financial condition is excellent and our balance

sheet remains strong. Our current assets were 3.1 times current

liabilities at the end of the year. To fund our cash requirements

we generated $498 million in cash flow from operations.

Capital expenditures of $65 million were in our normal range

and included funds to maintain and improve our facilities,

equipment, systems and technology projects. We also used cash

to reduce our total debt in 2002 by approximately $100 mil-

lion, decreasing our total debt to total capitalization ratio to

27% compared to 28% at the end of 2001. Continued reduc-

tion of our debt will remain a priority for us again in 2003.

During the year the Company also purchased approximately

400,000 shares of our Company stock, leaving a balance of 7.2

million shares authorized to be repurchased. We believe that a

gradual share repurchase plan combined with a meaningful

cash dividend will add value for our shareholders over time.

Dividends

2002 was our 46th consecutive year of dividend increases, with

dividends of $1.16 per share. We are proud of our dividend

record, and are pleased that on February 17, 2003, the Board of

Directors increased the cash dividend payable April 1, 2003 to

an annual rate of $1.18 per share. This equals 56% of our 2002

earnings before the effect of a change in accounting principle

and becomes our 47th consecutive year of dividend increases.

Progress in Operations

As we mentioned earlier in our remarks we were able to show

improvement in both sales and earnings for the year. At mid year

our results in sales and earnings trailed the previous year and it

was apparent that our economy was showing little change to

stimulate business activity. We feel fortunate that our operations

found a way in the second half of the year to generate an

improved picture with revenue gains in both the third and

fourth quarters.

For the year, revenues in our Automotive Group were up

2% for the year and presented our most consistent picture with

sales showing some increase in all four quarters. While this level

of growth does not meet our expectations for the longer term,

we believe the fundamentals are in place to support a gradual

Larry L. Prince

Chairman of the Board

Thomas C. Gallagher

President

5