Kodak 2011 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2011 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

|

|

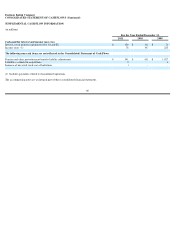

Diluted earnings per share calculations could also reflect shares related to the assumed conversion of approximately $315 million of convertible senior

notes due 2017, if dilutive. The Company’s diluted (loss) earnings per share excludes the effect of these convertible securities, as they were anti-

dilutive for all periods presented. Refer to Note 9, “Short-Term Borrowings and Long-Term Debt.”

RECENTLY ADOPTED ACCOUNTING PRONOUNCEMENTS

In December 2010, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2010-28, “When to Perform Step 2

of the Goodwill Impairment Test for Reporting Units with Zero or Negative Carrying Amounts,” which amends Accounting Standards Codification (ASC)

Topic 350, “Intangibles – Goodwill and Other.” ASU No. 2010-28 amends the ASC to require entities that have a reporting unit with a zero or negative

carrying value to assess whether qualitative factors indicate that it is more likely than not that an impairment of goodwill exists, and if an entity concludes

that it is more likely than not that an impairment exists, the entity must measure the goodwill impairment. The changes to the ASC as a result of this update

were effective for annual and interim reporting periods beginning after December 15, 2010 (January 1, 2011 for the Company). The adoption of this

guidance did not impact the Company’s Consolidated Financial Statements.

In October 2009, the FASB issued ASU No. 2009-13, “Multiple-Deliverable Revenue Arrangements,” which amends ASC Topic 605, “Revenue

Recognition.” ASU No. 2009-13 amends the ASC to eliminate the residual method of allocation for multiple-deliverable revenue arrangements, and

requires that arrangement consideration be allocated at the inception of an arrangement to all deliverables using the relative selling price method. The

ASU also establishes a selling price hierarchy for determining the selling price of a deliverable, which includes: (1) vendor-specific objective evidence if

available, (2) third-party evidence if vendor-specific objective evidence is not available, and (3) estimated selling price if neither vendor-specific nor

third-party evidence is available. Additionally, ASU No. 2009-13 expands the disclosure requirements related to a vendor's multiple-deliverable revenue

arrangements. The changes to the ASC as a result of this update were effective prospectively for revenue arrangements entered into or materially

modified in fiscal years beginning on or after June 15, 2010 (January 1, 2011 for the Company). The adoption of this guidance did not have a material

impact on the Company’s Consolidated Financial Statements.

In October 2009, the FASB issued ASU No. 2009-14, “Certain Revenue Arrangements That Include Software Elements,” which amends ASC Topic

985, “Software.” ASU No. 2009-14 amends the ASC to change the accounting model for revenue arrangements that include both tangible products and

software elements, such that tangible products containing both software and non-software components that function together to deliver the tangible

product's essential functionality are no longer within the scope of software revenue guidance. The changes to the ASC as a result of this update were

effective prospectively for revenue arrangements entered into or materially modified in fiscal years beginning on or after June 15, 2010 (January 1, 2011

for the Company). The adoption of this guidance did not have a material impact on the Company’s Consolidated Financial Statements.

RECENTLY ISSUED ACCOUNTING PRONOUNCEMENTS

In December 2011, the FASB issued ASU No. 2011-10, “Derecognition of in Substance Real Estate – a Scope Clarification,” which amends ASC Topic

360, “Property, Plant and Equipment.” ASU No. 2011-10 states that when an investor ceases to have a controlling financial interest in an entity that is in-

substance real estate as a result of a default on the entity’s nonrecourse debt, the investor should apply the guidance under ASC Subtopic 360-20, Property,

Plant and Equipment – Real Estate Sales (formerly FAS 66) to determine whether to derecognize the entity’s assets (including real estate) and liabilities

(including the nonrecourse debt). The changes to the ASC as a result of this update are effective prospectively for deconsolidation events occurring during

fiscal years, and interim periods within those years, beginning on or after June, 15, 2012 (January 1, 2013 for the Company). Adoption of this guidance will

not impact the Company’s Consolidated Financial Statements.

In December 2011, the FASB issued ASU No. 2011-11, “Balance Sheet (ASC Topic 210): Disclosures about Offsetting Assets and Liabilities.” ASU

No. 2011

-11 creates new disclosure requirements about the nature of an entity’s rights of setoff and related arrangements

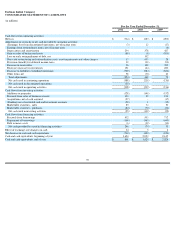

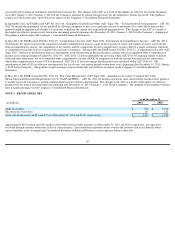

(in millions of shares)

For the Year Ended December 31,

2011

2010

2009

Employee stock options

13.6

18.0

23.5

Detachable warrants to purchase common shares

40.0

40.0

40.0

Total

53.6

58.0

63.5

68