IHOP 2013 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2013 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

60

Recently Adopted Accounting Standards

In May 2011, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”)

No. 2011-04, Fair Value Measurement - Amendments to Achieve Common Fair Value Measurement and Disclosure

Requirements in U.S. GAAP and IFRSs (“ASU 2011-04”). The amendments in ASU 2011-04 result in common fair value

measurement and disclosure requirements in U.S. GAAP and international financial reporting standards (“IFRS”). ASU

2011-04 also provides for certain changes in current GAAP disclosure requirements. The adoption of ASU 2011-04 did not

have a material impact on our consolidated financial statements.

In May 2011, the FASB issued ASU No. 2011-05, Comprehensive Income - Presentation of Comprehensive Income (“ASU

2011-05”). ASU 2011-05 requires the presentation of the total of comprehensive income, the components of net income, and

the components of other comprehensive income either in a single continuous statement of comprehensive income or in two

separate but consecutive statements. The amendments in this update did not change the items that must be reported in other

comprehensive income. The adoption of ASU 2011-05 did not have a material impact on our consolidated financial statements.

In September 2011, the FASB issued ASU No. 2011-08, Intangibles-Goodwill and Other - Testing Goodwill for

Impairment ("ASU 2011-08"). The amendments in ASU No. 2011-08 are intended to simplify goodwill impairment testing by

adding a qualitative review step to assess whether the required quantitative impairment analysis that exists today is necessary.

Under these amendments, an entity would not be required to calculate the fair value of a reporting unit unless the entity

determines, based on the qualitative assessment, that it is more likely than not that its fair value is less than its carrying amount.

We adopted ASU 2011-08 as of January 1, 2012. The adoption of ASU 2011-08 did not have a material impact on our

consolidated financial statements.

New Accounting Pronouncements

In February 2013, the FASB issued ASU No. 2013-04, Obligations Resulting from Joint and Several Liability

Arrangements for Which the Total Amount of the Obligation Is Fixed at the Reporting Date (“ASU 2013-04”). The

amendments in ASU 2013-04 require an entity to measure obligations resulting from joint and several liability arrangements as

the amount the entity agreed to pay on the basis of the arrangement among its co-obligors plus the amount an entity expects to

pay on behalf of co-obligors. ASU 2013-04 also requires an entity to disclose the nature, amount and other information about

each obligation or group of similar obligations. The adoption of ASU 2013-04 as of January 1, 2014, is not anticipated to have

a material impact on our consolidated financial statements.

In July 2013, the FASB issued ASU No. 2013-11, Income Taxes - Presentation of an Unrecognized Tax Benefit When a Net

Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists (“ASU 2013-11”). ASU 2013-11

provides guidance on the financial statement presentation of an unrecognized tax benefit, as either a reduction of a deferred tax

asset or as a liability, when a net operating loss carryforward, similar tax loss, or a tax credit carryforward exists. ASU 2013-11

may be applied on a retrospective basis, and early adoption is permitted. The adoption of ASU 2013-11 as of January 1, 2014,

is not anticipated to have a material impact on our consolidated financial statements.

We reviewed all other newly issued accounting pronouncements and concluded that they either are not applicable to our

operations or that no material effect is expected on our financial statements as a result of future adoption.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

We are exposed to financial market risk, including interest rates and commodity prices. We address these risks through

controlled risk management that may include the use of derivative financial instruments to economically hedge or reduce these

exposures. We do not enter into financial instruments for trading or speculative purposes.

Interest Rate Risk

Our interest expense and income is sensitive to fluctuations in the London Inter-Bank Offered Rate ("LIBOR") and the

general level of United States interest rates. Changes in LIBOR can affect the interest expense on our Senior Secured Credit

Facility while changes in the United States Treasury-based interest rates affect the interest earned on our cash and cash

equivalents, restricted cash and investments. Our future investment income and interest expense may differ from expectations

due to changes in interest rates.

At December 31, 2013, we had $467.2 million of variable rate debt (the Term Loan under our Credit Agreement). If the

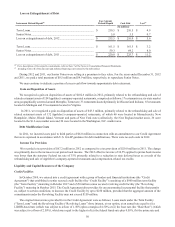

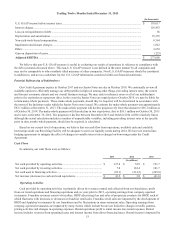

interest rate on the Term Loan were to increase by 1% per annum, annual interest expense would increase by approximately

$4.7 million based on the outstanding Term Loan balance at December 31, 2013. A decrease in interest rates from