Fifth Third Bank 2006 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2006 Fifth Third Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

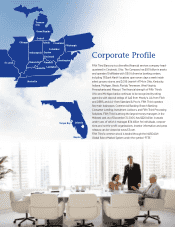

The affiliate model is at the core of Fifth Third and is what

differentiates us from other large financial institutions. We operate

each affiliate with local management. Each affiliate has an

experienced president and senior management team, resident in

each market, driving the business. And each affiliate has a board of

directors comprised of local business and community leaders. This

means that we have local decision-makers, able to view customer

relationships in holistic ways, making local decisions.

This model gives us a tremendous competitive advantage in our

responsiveness to customers; in attracting employees who want to

control the customer relationship locally; and in giving us 19 “mini-

incubators” for new ideas and best practices. Our entrepreneurial

and sales cultures are at the heart of the affiliate model, and

contribute tremendously to Fifth Third’s success.

Maintaining competitive advantage.

Overlaying the affiliate structure are our lines of business. These are

essentially areas of product expertise — Branch Banking, Consumer

Lending, Commercial Banking, Processing Solutions and Investment

Advisors — whose products and services are delivered to customers

through the affiliates in a way that ensures customer relationships

are viewed as a whole.

As an example of the kind of success we can produce with this

model, we have 19 affiliates plus our Pittsburgh and St. Louis

de novo markets. For the year ended June 2006 (most recent FDIC

data), 20 of these 21 markets (including the de novo markets) grew

deposits. Excluding branches with over $1 billion in deposits, all

21 markets grew deposits and 17 of the 21 markets grew deposit

market share (18 of 21 excluding $1 billion branches).

Affiliate Leadership

Chicago Region Terry Zink 312 $17.3B 25%

Chicago Terry Zink

Central Indiana John Pelizzari

Southern Indiana John Daniel

Tennessee Dan Hogan

Western Michigan Region Michelle VanDyke 273 $15.2B 22%

Western Michigan Michelle VanDyke

Eastern Michigan Greg Kosch

Northern Michigan Mark Eckhoff

Tampa Bay Brian Keenan

Cincinnati Region Bob Sullivan 205 $12.6B 18%

Cincinnati Bob Sullivan

Louisville Phil McHugh

Central Kentucky Sam Barnes

Northern Kentucky Tim Rawe

Cleveland Region Todd Clossin 187 $10.9B 16%

Northeastern Ohio Todd Clossin

Northwestern Ohio Robert LaClair

South Florida Tom Quinn

Columbus Region Bob Eversole 173 $ 9.4B 14%

Central Ohio Bob Eversole

Western Ohio Ray Webb

Ohio Valley David Call

Central Florida John Bultema

Affiliate* President Banking Centers Deposits % of Deposits

*Bancorp deposits also include $4 billion in National and non-affiliate deposits.

Affiliate Model

10