Fifth Third Bank 2006 Annual Report Download

Download and view the complete annual report

Please find the complete 2006 Fifth Third Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

building an even better

tomorrow.

2006 ANNUAL REPORT

Table of contents

-

Page 1

building an even better tomorrow. 2006 ANNUAL REPORT -

Page 2

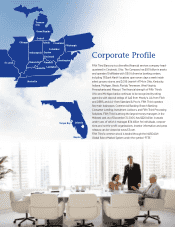

... Corporate Profile Fifth Third Bancorp is a diversified financial services company headquartered in Cincinnati, Ohio. The Company has $101 billion in assets and operates 19 affiliates with 1,150 full-service banking centers, including 111 Bank Mart® locations open seven days a week inside... -

Page 3

... Per Share Earnings Diluted Earnings Cash Dividends Book Value At Year-End Assets Total Loans and Leases Deposits Shareholders' Equity Year-End Market Price Market Capitalization Key Ratios (percent) Return on Average Assets (ROA) Return on Average Equity (ROE) Net Interest Margin Efficiency Ratio... -

Page 4

... tangible assets ratio. The interest rate environment, combined with the loss resulting from our balance sheet actions, took a toll on reported results for the year. Earnings per diluted share for 2006 were $2.13, down from $2.77 in 2005. Return on average assets and return on Dear Shareholders and... -

Page 5

..., we have been experiencing slower economic growth and higher levels of credit losses than banks in other regions for some time. Fifth Third is a lending company, and we are in the risk business. The ebbs and flows of the credit cycle are to be expected and do not change our attitude on that front... -

Page 6

... 10 of this report. Overlaying our affiliate structure are five lines of business: Branch Banking; Commercial Banking; Processing Solutions; Consumer Lending; and Investment Advisors. These lines of business are areas of expertise whose products and services are delivered to customers through the... -

Page 7

... most manual processes remaining in cash management. Customers using this product are able to save time, optimize their working capital and consolidate their banking relationships. We've experienced rapid growth in 2006, particularly the latter half, and are receiving deposits from locations in 35... -

Page 8

...wallet share with our customers. What our customers tell us they need is a trusted advisor for the long haul. To deliver, we must understand our customers' needs tomorrow to properly address the need today that brought them into our banking center or caused them to pick up the phone. In our service... -

Page 9

... and Chief Financial Officer; Malcolm D. Griggs, executive vice president, Enterprise Risk Management. Third row, left to right: Charles Drucker, executive vice president and president, Fifth Third Processing Solutions; Greg D. Carmichael, executive vice president and Chief Operating Officer; Carlos... -

Page 10

... all levels of Fifth Third employees. We also conducted research to understand exactly how the existing brand is perceived today. We learned much from this process, including that our customers don't feel they are spending enough time - or taking the right steps - to address their future needs. And... -

Page 11

... and call center employees. This training and ongoing sales coaching is designed around four key drivers customers find important. They include friendliness, ease of doing business, individualized attention, and the degree of knowledge about the bank's products and services. The goal is to ensure... -

Page 12

... Fifth Third's success. Overlaying the affiliate structure are our lines of business. These are essentially areas of product expertise - Branch Banking, Consumer Lending, Commercial Banking, Processing Solutions and Investment Advisors - whose products and services are delivered to customers through... -

Page 13

... them personally or via any of our automated banking solutions. Our business bankers can provide full solutions to a small business customer including loans, treasury management products, employee savings plans, or employee banking needs. Whether saving for a home, a child's education, planning for... -

Page 14

... loans on the Bank's behalf, otherwise know as indirect lending. Additionally, Consumer Lending provides loan and lease products to individuals including mortgages and home equity loans and lines, as well as federal and private student education loans. Customer Focus Recognizing that personal loans... -

Page 15

... profit-sharing plans, foundations and endowments. Customer Focus Clients receive specialized advice from one or more of our four business lines: Fifth Third Securities, Private Client Group, Fifth Third Institutional Client Group and Fifth Third Asset Management. Fifth Third's Private Client Group... -

Page 16

... offerings, our products and services include cash management, foreign exchange and international trade finance, derivatives and capital markets services, asset-based lending, real estate finance, public finance, commercial leasing and syndicated finance. Customer Focus Fifth Third has over 150... -

Page 17

.... Business Description Fifth Third Processing Solutions provides electronic funds transfer, debit, credit and merchant transaction processing for Fifth Third and Fifth Third customers. Processing Solutions specializes in providing our clients with the highest quality transaction solutions available... -

Page 18

... Academy at West Point Cadet Gospel Choir at the National Underground Railroad Freedom Center in Cincinnati. The event was one part of day-long festivities to honor military veterans. Fifth Third's Community Development Corporation (CDC) invests in low-income housing, historic tax credits and... -

Page 19

2006 ANNUAL REPORT FINANCIAL CONTENTS Management's Discussion and Analysis of Financial Condition and Results of Operations Selected Financial Data Overview Recent Accounting Standards Critical Accounting Policies Risk Factors Statements of Income Analysis Business Segment Review Fourth Quarter ... -

Page 20

...real estate owned Average Balances Loans and leases, including held for sale Total securities and other short-term investments Total assets Transaction deposits Core deposits Wholesale funding Shareholders' equity Regulatory Capital Ratios Tier I capital Total risk-based capital Tier I leverage 2006... -

Page 21

... 31, 2006, the Bancorp had $100.7 billion in assets, operated 19 affiliates with 1,150 full-service Banking Centers including 111 Bank Mart® locations open seven days a week inside select grocery stores and 2,096 Jeanie® ATMs in Ohio, Kentucky, Indiana, Michigan, Illinois, Florida, Tennessee, West... -

Page 22

... as defined by the Board of Governors of the Federal Reserve System ("FRB"). As of December 31, 2006, the Tier I capital ratio was 8.39% and the total risk-based capital ratio was 11.07%. The Bancorp continues to invest in the geographic areas that offer the best growth prospects, as it believes... -

Page 23

... rating or loss rates. Given current processes employed by the Bancorp, management believes the risk grades and inherent loss rates currently assigned are appropriate. The Bancorp's primary market areas for lending are Ohio, Kentucky, Indiana, Michigan, Illinois, Florida, Tennessee, West Virginia... -

Page 24

... Florida. An economic downturn within these markets or the nation as a whole could negatively impact household and corporate incomes. This impact may lead to decreased demand for both loan and deposit products and increase the number of customers who fail to pay interest or principal on their loans... -

Page 25

... and retaining customers for traditional banking services, Fifth Third's competitors also include securities dealers, brokers, mortgage bankers, investment advisors, specialty finance and insurance companies who seek to offer one-stop financial services that may include services that banks have not... -

Page 26

...unfavorable ratings from rating agencies. Fifth Third's ability to access the capital markets is important to its overall funding profile. This access is affected by the ratings assigned by rating agencies to Fifth Third, certain of its affiliates and particular classes of securities they issue. The... -

Page 27

... liabilities, or free funding, such as demand deposits or shareholders' equity. The continued increases in short-term rates during the first half of 2006 and the subsequent inverted interest rate yield curve negatively impacted Fifth Third as well as other financial institutions in 2006. The average... -

Page 28

...consumer loans. Other consumer loans primarily consist of direct and indirect home equity lines and 26 Fifth Third Bancorp loans, direct and indirect auto loans and credit cards. The average consumer loan and lease yield increased 83 bp to 6.52%. Interest income (FTE) from investment securities and... -

Page 29

...13) (10) Other short-term investments 8 7 15 (2) 3 Total change in interest income 196 759 955 342 534 Increase (decrease) in interest expense: Interest checking (41) 125 84 (5) 145 Savings 45 142 187 18 100 Money market 38 83 121 26 75 Other time deposits 71 99 170 68 33 Certificates - $100,000 and... -

Page 30

... in markto-market free-standing derivatives related to the balance sheet actions taken in the fourth quarter. Operating lease revenues in Fifth Third Funds investments are: NOT INSURED BY THE FDIC or any other government agency, are not deposits or obligations of, or guaranteed by, any bank, the... -

Page 31

... loan and lease fees Operating lease income Bank owned life insurance income Insurance income Gain on sales of third-party sourced merchant processing contracts Other Total other noninterest income The Bancorp recognized net securities losses of $364 million in 2006. Securities losses in 2006... -

Page 32

... 2004 was negatively impacted by balance sheet actions, which included debt termination charges and securities losses totaling $404 million pretax. Earnings were positively impacted by a $157 million pretax gain resulting from the sale of certain third-party sourced merchant processing contracts in... -

Page 33

... depository offerings, Commercial Banking products and services include, among others, cash management, foreign exchange and international trade finance, derivatives and capital markets services, asset-based lending, real estate finance, public finance, commercial leasing and syndicated finance. The... -

Page 34

... Banking offers depository and loan products, such as checking and savings accounts, home equity lines of credit, credit cards and loans for automobile and other personal financing needs, as well as products designed to meet the specific needs of small businesses, including cash management services... -

Page 35

... and leases $3,068 Core deposits 4,499 Processing Solutions Fifth Third Processing Solutions provides electronic funds transfer, debit, credit and merchant transaction processing, operates the Jeanie® ATM network and provides other data processing services to affiliated and unaffiliated customers... -

Page 36

... on mortgage servicing rights. Investment advisory revenues increased by four percent over the same quarter last year. The increase was driven by strong growth in private banking and moderate growth in the retail securities and institutional businesses, partially offset by lower mutual fund fees... -

Page 37

...719 Credit card 942 Home equity 12,268 Other consumer loans 9,439 Consumer leases 1,328 Total consumer loans and leases (including held for sale) 33,551 Total loans and leases (including held for sale) $73,493 Total portfolio loans and leases (excluding held for sale) $72,447 Fifth Third Bancorp 35 -

Page 38

...2006, the Bancorp evaluated its overall balance sheet composition and took certain actions with respect to its available-for-sale securities portfolio. The Bancorp's objective was to improve the asset/liability profile of the Bancorp and reduce the size of its available-for-sale securities portfolio... -

Page 39

...-yield transaction accounts to higheryield time deposits. Overall, transaction deposits balances TABLE 23: AVERAGE DEPOSITS As of December 31 ($ in millions) Demand Interest checking Savings Money market Transaction deposits Other time Core deposits Certificates - $100,000 and over Foreign office... -

Page 40

... analytics and Board of Directors and senior management reporting on credit, market and operational risk metrics; and • Investment Advisors Risk Management - responsible for trust compliance, fiduciary risk and trading risk in the Investment Advisors line of business. Designated risk managers have... -

Page 41

... Risk Management division manages the policy and authority delegation process centrally. The Credit Risk Review function, within the Enterprise Risk Management division, provides objective assessments of the quality of underwriting and documentation, the accuracy of risk grades and the charge... -

Page 42

... of outstanding balances and exposures concentrated within the Bancorp's primary market areas of Ohio, Kentucky, Indiana, Michigan, Illinois, Florida, Tennessee, West Virginia, Missouri and Pennsylvania. Exclusive of a national large-ticket leasing business, the commercial portfolio is characterized... -

Page 43

... for loan and lease losses. The Bancorp also considers overall asset quality trends, credit administration and portfolio management practices, risk identification practices, credit policy and underwriting practices, overall portfolio growth, portfolio concentrations and current TABLE 28: CHANGES IN... -

Page 44

.... Residential Mortgage Portfolio Certain mortgage products have contractual features that may increase credit exposure to the Bancorp in the event of a decline in housing prices. These types of mortgage products offered by the Bancorp include high loan-to-value ("LTV") ratios, multiple loans on the... -

Page 45

... rate risk profile, management recommended and the Bancorp's Board of Directors approved a decision on November 20, 2006 to reduce the size of the available-for-sale securities portfolio. This action was undertaken in order to, among other reasons, improve the composition of the Bancorp's balance... -

Page 46

...to meet the terms of their contracts, which the Bancorp minimizes through approvals, limits and monitoring procedures. The notional amount and fair values of these derivatives as of December 31, 2006 are included in Note 8 of the Notes to Consolidated Financial Statements. Foreign Currency Risk The... -

Page 47

... manages availability in response to changing balance sheet needs. As of December 31, 2006, the Moody's senior debt rating for the Bancorp was Aa3, a rating surpassed by only four other U.S. bank holding companies. Table 37 provides Moody's, Standard and Poor's and Fitch's deposit and debt ratings... -

Page 48

... securitizations 97 132 Fees received 35 32 The Bancorp utilizes securitization trusts formed by independent third parties to facilitate the securitization process of residential mortgage loans, certain floating-rate home equity lines of credit, certain auto loans and other consumer loans. The cash... -

Page 49

... general contractors for work related to banking center construction. (f) Includes low-income housing, historic tax and venture capital partnership investments. (g) Represents agreements to purchase goods or services. (h) See Note 12 of the Notes to Consolidated Financial Statements for additional... -

Page 50

... public accounting firm, that audited the Bancorp's consolidated financial statements included in this annual report, has issued an attestation report on our internal control over financial reporting as of December 31, 2006 and Bancorp Management's assessment of the internal control over financial... -

Page 51

... 31, 2006 of the Bancorp and our report dated February 15, 2007 expressed an unqualified opinion on those financial statements. Cincinnati, Ohio February 15, 2007 To the Shareholders and Board of Directors of Fifth Third Bancorp: We have audited the accompanying consolidated balance sheets of Fifth... -

Page 52

... on other short-term investments Total interest income Interest Expense Interest on deposits: Interest checking Savings Money market Other time Certificates - $100,000 and over Foreign office Total interest on deposits Interest on federal funds purchased Interest on short-term bank notes Interest... -

Page 53

...Money market Other time Certificates - $100,000 and over Foreign office Total deposits Federal funds purchased Other short-term borrowings Accrued taxes, interest and expenses Other liabilities Long-term debt Total Liabilities Shareholders' Equity Common stock (a) Preferred stock (b) Capital surplus... -

Page 54

... shares issued Loans repaid related to the exercise of stock-based awards, net Change in corporate tax benefit related to stock-based compensation Other Balance at December 31, 2006 See Notes to Consolidated Financial Statements Common Preferred Stock Stock $1,295 9 Accumulated Other Capital... -

Page 55

... in business combination Net Cash Provided by (Used In) Investing Activities Financing Activities Increase in core deposits Increase (decrease) in certificates - $100,000 and over, including foreign office (Decrease) increase in federal funds purchased (Decrease) increase in short-term bank notes... -

Page 56

... ("Bancorp"), an Ohio corporation, conducts its principal lending, deposit gathering, transaction processing and service advisory activities through its banking and non-banking subsidiaries from banking centers located throughout Ohio, Kentucky, Indiana, Michigan, Illinois, Florida, Tennessee, West... -

Page 57

... allowance for loan and lease losses nor does the Bancorp add to its existing allowance for the acquired loans as part of purchase accounting. The Bancorp's primary market areas for lending are Ohio, Kentucky, Indiana, Michigan, Illinois, Florida, Tennessee, West Virginia, Pennsylvania and Missouri... -

Page 58

... property held by Fifth Third Investment Advisors, a division of the Bancorp's banking subsidiaries, in a fiduciary or agency capacity are not included in the Consolidated Balance Sheets because such items are not assets of the subsidiaries. Investment advisory revenue in the Consolidated Statements... -

Page 59

... information on stock-based compensation see Note 18. In December 2003, the Accounting Standards Executive Committee of the American Institute of Certified Public Accountants issued Statement of Position ("SOP") 03-3, "Accounting for Certain Loans and Debt Securities Acquired in a Transfer." SOP 03... -

Page 60

... fiscal years. The Bancorp is currently in the process of evaluating the impact of adopting this Statement on its Consolidated Financial Statements. In September 2006, the FASB issued SFAS No. 158, "Employer's Accounting for Defined Benefit Pension and Other Postretirement Plans - An Amendment of... -

Page 61

...FHLMC preferred stock holdings, certain mutual fund holdings and equity security holdings. During the fourth quarter of 2006, the Bancorp evaluated its overall balance sheet composition and took certain actions with respect to its available-for-sale securities portfolio. The Bancorp's objective was... -

Page 62

..., were pledged to secure borrowings, public deposits, trust funds and for other purposes as required or permitted by law. Unrealized gains and losses on trading securities held at December 31, 2006 and 2005 were not material to the Consolidated Financial Statements. 60 Fifth Third Bancorp -

Page 63

... leases Residential mortgage Home equity Other consumer loans Total loans held for sale Portfolio loans and leases (a): Commercial: Commercial loans Commercial mortgage Commercial construction Commercial leases Total commercial Consumer: Residential mortgage Residential construction Credit card Home... -

Page 64

... 2005 Acquisition activity Reclassification Balance as of December 31, 2006 Commercial Banking $373 498 871 $871 Branch Banking 254 544 798 (1) 797 Consumer Lending 58 124 182 182 Investment Advisors 103 24 127 11 138 Processing Solutions 191 191 14 205 Total 979 1,190 2,169 13 11 2,193 The Bancorp... -

Page 65

... long-term debt attributable to the risk being hedged. For interest rate swaps that do not qualify for the shortcut method of accounting, the ineffectiveness is reported within interest expense in the Consolidated Statements of Income. For the years ended December 31, 2006 and 2005, changes in the... -

Page 66

... benefit of commercial customers. These derivative contracts are not designated against specific assets or liabilities on the Consolidated Balance Sheets or to forecasted transactions and, therefore, do not qualify for hedge accounting. These instruments include foreign exchange derivative contracts... -

Page 67

... Consolidated Statements of Income relating to free-standing derivative instruments for the years ended December 31 are summarized in the table below: ($ in millions) Foreign exchange contracts Forward contracts related to interest rate lock commitments and mortgage loans held for sale Interest rate... -

Page 68

... in the Consolidated Balance Sheets as of December 31: ($ in millions) Bank owned life insurance Accounts receivable and drafts-in-process Partnership investments Accrued interest receivable Derivative instruments Prepaid pension and other expenses Other real estate owned Other Total 2006 $1,949... -

Page 69

... debt rating to or below BBB, a change in the investor's tax elections or a change to applicable tax law. At December 31, 2006, FHLB advances have rates ranging from 0% to 8.34%, with interest payable monthly. The advances were secured by certain residential mortgage loans and securities totaling... -

Page 70

... and their ability to meet the terms of the contract. The Bancorp controls the credit risk of these transactions through adherence to a derivatives products policy, credit approval policies and monitoring procedures. Collateral, if deemed necessary, is based on management's credit evaluation of the... -

Page 71

... can include commercial real estate, physical plant and property, inventory, receivables, cash and marketable securities. Through December 31, 2006 and 2005, the Bancorp had transferred, subject to credit recourse, certain primarily floatingrate, short-term investment grade commercial loans to an... -

Page 72

... the Bancorp transacts business. The Bancorp maintains a written policy and procedures covering related party transactions. These procedures cover transactions such as employee-stock purchase loans, personal lines of credit, residential secured loans, overdrafts, letters of credit and increases in... -

Page 73

... that its Board of Directors had authorized management to purchase 20 million shares of the Bancorp's common stock through the open market or in any private transaction. The timing of the purchases and the exact number of shares to be purchased depends upon market conditions. The authorization does... -

Page 74

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 18. STOCK-BASED COMPENSATION The Bancorp has historically emphasized employee stock ownership. Based on total stock-based awards outstanding and shares remaining for future grants under the Incentive Compensation Plan, the Bancorp's total overhang is ... -

Page 75

... group. The performance-based awards were granted at a weighted-average grant-date fair value of $39.14 per share. The Bancorp sponsors a Stock Purchase Plan that allows qualifying employees to purchase shares of the Bancorp's common stock with a 15% match. During the years ended December 31, 2006... -

Page 76

... fees Consumer loan and lease fees Operating lease income Bank owned life insurance income Insurance income Gain on sale of third-party sourced merchant processing contracts Other Total Other noninterest expense: Marketing and communications Postal and courier Bankcard Loan and lease Travel... -

Page 77

... to investor's interests and its value is subject to credit, prepayment and interest rate risks on the sold home equity lines of credit. During 2006, pursuant to the terms of the sales and servicing agreement, $39 million in fixed-rate home equity line of credit balances were put back to the Bancorp... -

Page 78

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 21. INCOME TAXES The Bancorp and its subsidiaries file a consolidated Federal income tax return. The following is a summary of applicable income taxes included in the Consolidated Statements of Income at December 31: ($ in millions) Current income taxes: ... -

Page 79

... necessary. The discount rate assumption reflects the yield on a portfolio of high quality fixed-income instruments that have a similar duration to the plan's liabilities. The expected long-term rate of return assumption reflects the average return expected on the assets invested to provide for the... -

Page 80

... of common trust and mutual funds (equities and fixed income) and Bancorp common stock. As of December 31, 2006 and 2005, $156 million and $178 million, respectively, of plan assets were managed by Fifth Third Bank, a subsidiary of the Bancorp, through common trust and mutual funds and included... -

Page 81

...limited credit risk, carrying amounts approximate fair value. Those financial instruments include cash and due from banks, other short-term investments, certain deposits (demand, interest checking, savings and money market), federal funds purchased and other short-term borrowings. Available-for-sale... -

Page 82

... assets (Tier I leverage ratio). Failure to meet the minimum capital requirements can initiate certain actions by regulators that could have a direct material effect on the Consolidated Financial Statements of the Bancorp. Tier I capital consists principally of shareholders' equity including Tier... -

Page 83

... FINANCIAL STATEMENTS Capital and risk-based capital and leverage ratios for the Bancorp and its significant subsidiary banks at December 31: ($ in millions) Total risk-based capital (to risk-weighted assets): Fifth Third Bancorp (Consolidated) Fifth Third Bank (Ohio) Fifth Third Bank (Michigan... -

Page 84

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 28. SEGMENTS The Bancorp's principal activities include Commercial Banking, Branch Banking, Consumer Lending, Investment Advisors and Processing Solutions. During the first quarter of 2006, the Bancorp began reporting its Retail line of business as two ... -

Page 85

... Electronic payment processing revenue Service charges on deposits Mortgage banking net revenue Investment advisory revenue Corporate banking revenue Other noninterest income Securities gains (losses), net Total noninterest income Noninterest expense: Salaries, wages and incentives Employee benefits... -

Page 86

... Director Independence 91 91 Item 14. Principal Accounting Fees and Services PART IV 91-93 Item 15. Exhibits, Financial Statement Schedules 94 SIGNATURES PART I Item 1. AVAILABILITY OF FINANCIAL INFORMATION The Bancorp files reports with the SEC. Those reports include the annual report on Form 10... -

Page 87

... of checking, savings and money market accounts, and credit products such as credit cards, installment loans, mortgage loans and lease. Each of the banking subsidiaries has deposit insurance provided by the Federal Deposit Insurance Corporation ("FDIC") through the Deposit Insurance Fund. Refer... -

Page 88

... practice for bank holding companies to pay dividends unless a bank holding company's net income is sufficient to fund the dividends and the expected rate of earnings retention is consistent with the organization's capital needs, asset quality and overall financial condition. The Bancorp depends in... -

Page 89

...enforcement actions. In addition, as discussed above, each of the Bancorp's subsidiary banks must remain well capitalized for the Bancorp to retain its status as a financial holding company. The minimum risk-based capital requirements adopted by the federal banking agencies follow the Capital Accord... -

Page 90

... Notes to Consolidated Financial Statements. 88 Fifth Third Bancorp ITEM 2. PROPERTIES The Bancorp's executive offices and the main office of Fifth Third Bank are located on Fountain Square Plaza in downtown Cincinnati, Ohio in a 32-story office tower, a five-story office building with an attached... -

Page 91

...the Consolidated Financial Statements. Additionally, as of December 31, 2006, the Bancorp had approximately 57,411 shareholders of record. Issuer Purchases of Equity Securities Maximum Shares Shares that Purchased May Be as Part of Purchased Average Publicly Under the Shares Price Announced Plans or... -

Page 92

... 2002 2003 2004 2005 2006 Fifth Third (FITB) S&P Banks (BIX) ITEM 9A. CONTROLS AND PROCEDURES The Bancorp conducted an evaluation, under the supervision and with the participation of the Bancorp's management, including the Bancorp's Chief Executive Officer and Chief Financial Officer, of the... -

Page 93

... public accounting firm, that audited the Bancorp's consolidated financial statements included in this annual report, has issued an attestation report on our internal control over financial reporting as of December 31, 2006 and Bancorp Management's assessment of the internal control over financial... -

Page 94

... Fifth Third Bancorp, as successor to Old Kent Financial Corporation, and Bankers Trust Company. Incorporated by reference to the Exhibits to Old Kent Financial Corporation's Current Report on Form 8-K filed with the Securities and Exchange Commission on March 5, 1997. Guarantee Agreement, dated as... -

Page 95

...Consolidated Ratios of Earnings to Combined Fixed Charges and Preferred Stock Dividend Requirements. 14 Code of Ethics. Incorporated by reference to Exhibit 14 of the Registrant's Current Report on Form 8-K filed with the Securities and Exchange Commission on January 23, 2007. 21 Fifth Third Bancorp... -

Page 96

... on its behalf by the undersigned, thereunto duly authorized. FIFTH THIRD BANCORP Registrant George A. Schaefer, Jr. Chairman and CEO Principal Executive Officer February 20, 2007 Pursuant to requirements of the Securities Exchange Act of 1934, this report has been signed on February 20, 2007 by the... -

Page 97

...000 140 (184) 5,005 (a) Federal funds sold and interest-bearing deposits in banks are combined in other short-term investments in the Consolidated Financial Statements. (b) Adjusted for stock splits in 2000, 1998 and 1997. Allowance Book Value for Loan and Lease Per Losses Share (b) $18.02 $771 17... -

Page 98

...Sullivan, Jr. N. Beverley Tucker, Jr. Alton C. Wendzel FIFTH THIRD BANCORP OFFICERS George A. Schaefer, Jr. Chairman & CEO Kevin T. Kabat President Greg D. Carmichael Executive Vice President & Chief Operating Officer David J. DeBrunner Senior Vice President & Controller Charles D. Drucker Executive... -

Page 99

... Trading The common stock of Fifth Third Bancorp is traded in the over-the-counter market and is listed under the symbol "FITB" on the NASDAQ® Global Select Market System. Press Releases For copies of current press releases, please visit our Website at www.53.com. 2006 Dividends Paid Per Share... -

Page 100

www.53.com