Blackberry 2016 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2016 Blackberry annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

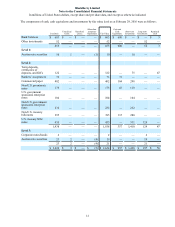

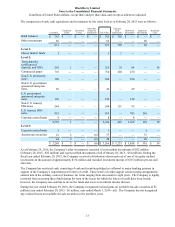

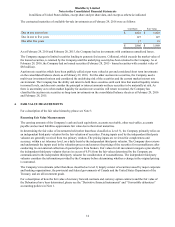

BlackBerry Limited

Notes to the Consolidated Financial Statements

In millions of United States dollars, except share and per share data, and except as otherwise indicated

4

Inventories

Raw materials, work in process and finished goods are stated at the lower of cost or market value. Cost includes the cost

of materials plus direct labour applied to the product and the applicable share of manufacturing overhead. Cost is

determined on a first-in, first-out basis. Market is generally considered to be replacement cost; however, market is not

permitted to exceed the ceiling (net realizable value) or be less than the floor (net realizable value less a normal markup).

Net realizable value is defined as the estimated selling price in the ordinary course of business, less reasonably predictable

costs of completion and disposal.

Property, plant and equipment, net

Property, plant and equipment are stated at cost, less accumulated amortization. No amortization is provided for

construction in progress until the assets are ready for use. Amortization is provided using the following rates and methods:

Buildings, leasehold improvements and other Straight-line over terms between 5 and 40 years

BlackBerry operations and other information technology Straight-line over terms between 3 and 5 years

Manufacturing equipment, research and development

equipment and tooling Straight-line over terms between 1 and 5 years

Furniture and fixtures Declining balance at 20% per annum

Goodwill

Goodwill represents the excess of the acquisition price over the fair value of identifiable net assets acquired. Goodwill is

allocated at the date of the business combination. Goodwill is not amortized, but is tested for impairment annually, during

the fourth quarter, or more frequently if events or changes in circumstances indicate the asset may be impaired. These

events and circumstances may include a significant change in legal factors or in the business climate, a significant decline

in the Company’s share price, an adverse action or assessment by a regulator, unanticipated competition, a loss of key

personnel, significant disposal activity and the testing of recoverability for a significant asset group.

The Company consists of a single reporting unit. The impairment test is carried out in two steps. In the first step, the

carrying amount of the reporting unit including goodwill is compared with its fair value. The estimated fair value is

determined utilizing a market-based approach, based on the quoted market price of the Company’s stock in an active

market, adjusted by an appropriate control premium. When the carrying amount of a reporting unit exceeds its fair value,

goodwill of the reporting unit is considered to be impaired and the second step is necessary. In the second step, the

implied fair value of the reporting unit’s goodwill is compared with its carrying amount to measure the amount of the

impairment loss, if any.

Intangible assets

Intangible assets with definite lives are stated at cost, less accumulated amortization. Amortization is provided on a

straight-line basis over the following terms:

Acquired technology Between 3 and 10 years

Intellectual property Between 1 and 17 years

Other acquired intangibles Between 2 and 10 years

Intellectual property contains patents and agreements with third parties for the use of intellectual property. Other acquired

intangibles include items such as customer relationships and brand. The useful lives of intangible assets are evaluated at

least annually to determine if events or circumstances warrant a revision to their remaining period of amortization. Legal,

regulatory and contractual factors, the effects of obsolescence, demand, competition and other economic factors are

potential indicators that the useful life of an intangible asset may be revised.

Impairment of long-lived assets

The Company reviews long-lived assets (“LLA”) such as property, plant and equipment and intangible assets with finite

useful lives for impairment whenever events or changes in circumstances indicate that the carrying amount of the asset or

asset group may not be recoverable. These events and circumstances may include significant decreases in the market price

of an asset or asset group, significant changes in the extent or manner in which an asset or asset group is being used by the

Company or in its physical condition, a significant change in legal factors or in the business climate, a history or forecast