US Bank 2003 Annual Report Download

Download and view the complete annual report

Please find the complete 2003 US Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

2003 ANNUAL REPORT AND FORM 10-K

Table of contents

-

Page 1

2 0 0 3 A N N U A L R E P O R T A N D F O R M 10 - K -

Page 2

... government banking services, mortgage, commercial credit vehicles, and financial and asset management services. Major lines of business provided by U.S. Bancorp through U.S. Bank and other subsidiaries include Consumer Banking Payment Services Private Client, Trust & Asset Management and Wholesale... -

Page 3

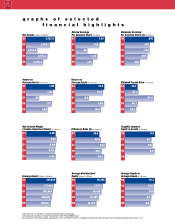

... Summary pg. 3 t a b l e o f c o n t e n t s Letter to Shareholders pg. 4 Corporate Governance pg. 5 Service Excellence pg. 6 Lines of Business pg. 8 Investing in Distribution and Scale pg. 10 Attractive Business Mix pg. 12 High-Value National Businesses pg. 14 Community Partnerships pg. 16... -

Page 4

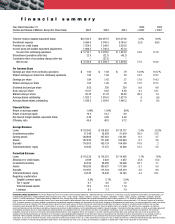

... was not available to compute pre-merger proforma percentage. (a) Dividends per share have not been restated for the 2001 Firstar/USBM merger. (b) Computed as noninterest expense divided by the sum of net interest income on a taxable-equivalent basis and noninterest income excluding securities gains... -

Page 5

...securities market conditions and monetary fluctuations could adversely affect the value or credit quality of our assets, or the availability and terms of funding necessary to meet our liquidity needs; (iv) changes in the extensive laws, regulations and policies governing financial services companies... -

Page 6

...the common stock dividend discussed above, as part of the December 2003 spin-off of Piper Jaffray, U.S. Bancorp distributed common shares of the new Piper Jaffray Companies in the form of a special dividend to eligible U.S. Bancorp shareholders. Also in December 2003, our Board of Directors approved... -

Page 7

... our Board committees on our Internet web site at usbank.com. Management's ownership commitment. We understand clearly that U.S. Bancorp shareholders are the primary beneficiaries of management's actions. All U.S. Bancorp executive officers and directors own shares of company stock, and in order to... -

Page 8

... we fall short in keeping our service guarantees, and our customer tells us they did not get the service they expected and deserved, we pay the customer for the inconvenience. Taking ownership of our business one employee at a time. Each line of business has developed and adapted its own Five Star... -

Page 9

... and rewarded for their outstanding service. Our Pay for Performance compensation program rewards employees financially and personally for their achievements in meeting service and sales goals and for their contributions to company earnings. Customized line of business incentive programs drive... -

Page 10

...cash management solution; provides a single point of access to information reporting, plus the initiation of wire transfers, ACH, book transfers, stop payments and data export functions. • Expanded U.S. Bank FIRSTLook Now, a new wholesale lockbox image service that offers same-day, online customer... -

Page 11

... for bank partners, and improve cash flow and point-of-sale operations for merchant customers. • Entered the health care payment segment through the MedAssist Advantage Plan (MAP), offering a new solution for patient financing. KEY BUSINESS UNITS Private Client, Trust & Asset Management meets... -

Page 12

... banking offices in 24 states, 4,425 U.S. Bank ATMs, 24-hour call center service, U.S. Bank Internet Banking and specialized trust, brokerage and home mortgage offices - form the foundation of our powerful presence in many of the country's high-growth, diversified markets. Our growing branch network... -

Page 13

... the cash flow management, credit and financing resources that support Millennium Development's business vision. San Francisco Los Angeles San Diego Phoenix Reno Salt Lake City Sacramento Las Vegas Nashville Strategic investments solidify our position in high-growth markets and businesses. In 2003... -

Page 14

... relationship with Mathews-Dickey, a long-time client of the U.S. Bank Private Client Group. We are proud to manage the Endowment Fund for MathewsDickey to support its youth-enrichment programs for years to come. business mix with scale, resulting in competitive advantages, operating economies... -

Page 15

... 5.5% Middle Market Banking 4.9% Mortgage Banking 4.3% Consumer Lending 3.9% Private Client Group 3.4% Commercial Real Estate 2.5% Corporate Trust 2.0% Government Banking 1.9% Asset Management 1.9% Corporate Payment Systems 1.1% Institutional Trust .7% Fund Services Improving business unit trends... -

Page 16

... and services not limited by location, U.S. Bancorp has built a national standing in a number of high-growth businesses. high-value national businesses Lockheed Martin Corporation, the world's premier advanced technology systems integrator, has partnered with U.S. Bank Corporate Payment Systems... -

Page 17

...of new product introductions. National Businesses Asset Management Commercial Real Estate Consumer Lending Corporate Banking Corporate Payment Systems Corporate Trust Elan Financial Services Equipment Financing Fund Services Government Banking Institutional Custody Mortgage Banking NOVA Information... -

Page 18

... economic, educational and cultural development. As an active partner, U.S. Bancorp provides superior, competitive products and services to every customer we serve, while offering customized financial solutions to customers and businesses who need assistance U.S. BANCORP FOUNDATION 2003 CHARITABLE... -

Page 19

... pricing and business development decisions that strengthen both U.S. Bancorp and the community. U.S. Bank gives "Back 2 Schools in Minnesota." U.S. Bank is investing nearly $500,000 in programs that support Minnesota teachers, high schools and students during the 20032004 school year. Designed... -

Page 20

..., or $.02 per diluted share, primarily related to the purchase of a transportation leasing company in 1998 by the equipment leasing business. This charge was taken at the time of adopting new accounting standards related to goodwill and other intangible assets and was recognized as a ''cumulative... -

Page 21

... Period End Balances Loans Allowance for credit losses Investment securities Assets Deposits Long-term debt Total shareholders' equity Regulatory capital ratios Tangible common equity Tier 1 capital Total risk-based capital Leverage * (a) (b) (c) Information was not available to... -

Page 22

... free funds due to lower average interest rates. The 2.0 percent net increase in noninterest income was driven by increases in payment services revenue, trust and investment management fees, deposit service charges, treasury management fees, mortgage banking activity, strong investment product sales... -

Page 23

... transition of business relationships. On November 1, 2002, the Company acquired 57 branches and a related operations facility in northern California from Bay View, a wholly-owned subsidiary of Bay View Capital Corporation, in a cash transaction. The transaction represented total assets acquired of... -

Page 24

...of loans from Stellar Funding Group, Inc. in mid-2003. Despite recent economic growth, the Company anticipates that commercial loan demand will continue to be soft in early 2004 while business customers utilize liquidity in deposit accounts to fund business activities. Average investment securities... -

Page 25

... risk management practices, align charge-off policies and expedite the transition out of a speciï¬c segment of the health care industry not meeting the lower risk appetite of the combined company; a $76.6 million provision for losses related to the sales of high loan-to-value home equity loans and... -

Page 26

...) 2003 2002 2001 2003 v 2002 2002 v 2001 Credit and debit card revenue Corporate payment products revenue ATM processing services Merchant processing services Trust and investment management fees Deposit service charges Treasury management fees Commercial products revenue Mortgage banking... -

Page 27

... 2002 2001 2003 v 2002 2002 v 2001 Compensation Employee beneï¬ts Net occupancy and equipment Professional services Marketing and business development Technology and communications Postage, printing and supplies Goodwill Other intangibles Merger and restructuring-related charges Other... -

Page 28

... further information on funding practices, investment policies and asset allocation strategies. Periodic pension expense (or credits) includes service costs, interest costs based on the assumed discount rate, the expected return on plan assets based on an actuarially derived market-related value and... -

Page 29

... processing platforms and business processes of U.S. Bank National Association and NOVA. In addition, the Company incurred pre-tax merger and restructuring-related expenses in 2003 of $12.7 million primarily for systems conversion costs associated with the Bay View and State Street Corporate Trust... -

Page 30

..., sell credit portfolios or otherwise realign business practices in the new Company. The Company also incurred $190.5 million related to the accelerated vesting of certain stock options and restricted stock, $207.1 million of systems conversion and business integration costs, $48.7 million for lease... -

Page 31

... Capital goods Financial services Commercial services and supplies Agriculture Consumer staples Transportation Property management and development Private investors Health care Paper and forestry products, mining and basic materials Information technology Energy Other Total Loans... -

Page 32

...locations. Commercial Real Estate The Company's portfolio of $7.9 billion at December 31, 2002. The Company also ï¬nances the operations of real estate developers and other entities with operations related to real estate. These loans are not secured directly by real estate and are subject to terms... -

Page 33

... of proceeds from loan sales and declining commercial loan balances due to the continued softness in commercial loan demand and the investment of cash inï¬,ows related to deposit growth. During 2003, the Company sold $15.3 billion of ï¬xed-rate securities as part of an economic hedge of the... -

Page 34

... are presented on a fully-taxable equivalent basis. Yields on available-for-sale and held-to-maturity securities are computed based on historical cost balances. Average yield and maturity calculations exclude equity securities that have no stated yield or maturity. 2003 At December 31 (Dollars in... -

Page 35

... quarter directly related to the upward movement in interest rates experienced since late June, 2003. Government banking deposits declined primarily due to a decision by the federal government to pay fees for cash management services rather than maintain compensating balances. Average noninterest... -

Page 36

... decline in the Company's stock value, customer base or revenue. Credit Risk Management The Company's strategy for credit long-term borrowings to fund growth of earning assets in excess of deposit growth. Short-term borrowings, which include federal funds purchased, securities sold under agreements... -

Page 37

... business activities, it offers a broad array of traditional commercial lending products and specialized products such as asset-based lending, commercial lease ï¬nancing, agricultural credit, warehouse mortgage lending, commercial real estate, health care and correspondent banking. The Company... -

Page 38

... economic growth, businesses with leveraged capital structures may experience insufï¬cient cash ï¬,ows to service their debt. The Company manages leveraged enterprise-value ï¬nancings by maintaining well-deï¬ned underwriting standards, portfolio diversiï¬cation and actively managing the customer... -

Page 39

...lower prices. Certain health care facilities providers continue to experience operational stress leading to some deterioration in credit quality within that sector. Also, given the recent slowdown in reï¬nancing activities and housing starts, the mortgage banking and real estate development sectors... -

Page 40

...% .59% .74 .99 .62 .68% nonperforming commercial and commercial real estate assets was principally due to the Company's exposure to certain communications, cable, manufacturing and highly leveraged enterprise-value ï¬nancings. Nonperforming loans in the capital goods sector also increased in 2002... -

Page 41

... and development Total commercial real estate Residential mortgages Retail Credit card Retail leasing Home equity and second mortgages Other retail Total retail Total loans (a (a) In accordance with guidance provided in the Interagency Guidance on Certain Loans Held for Sale, loans held... -

Page 42

...ï¬nance division specializes in serving channelspeciï¬c and alternative lending markets in residential mortgages, home equity and installment loan ï¬nancing. The consumer ï¬nance division manages loans originated through a broker network, correspondent relationships and U.S. Bank branch ofï¬ces... -

Page 43

...1.16 .35 Commercial real estate Commercial mortgages Construction and development Total commercial real estate Residential mortgages Retail Credit card Retail leasing Home equity and second mortgages ******** Other retail Total retail Total allocated allowance Available for other factors... -

Page 44

... of $263.0 million was related to uncertainty in the economy from lagging unemployment rates, concentration risk, including risks associated with the sluggish airline industry and highly leveraged enterprise-value credits, and other qualitative factors. Although the Company determines the amount of... -

Page 45

... development Total commercial real estate Residential mortgages Retail Credit card Retail leasing Home equity and second mortgages Other retail Total retail Total net charge-offs Provision for credit losses Losses from loan sales/transfers (a Acquisitions and other changes Balance at end... -

Page 46

... existed at December 31, 2003. In 2003, reduced airline travel and higher fuel costs adversely impacted aircraft and transportation equipment lease residual values. Operational Risk Management Operational risk represents the risk of loss resulting from the Company's operations, including, but not... -

Page 47

... of internal controls to executive management and the Audit Committee of the Board of Directors. Customer-related business conditions may also increase operational risk or the level of operational losses in certain transaction processing business units, including merchant processing activities... -

Page 48

... commitments to sell mortgage loans related to ï¬xed-rate mortgage loans held for sale and ï¬xed-rate mortgage loan commitments. The Company also acts as a seller and buyer of interest rate contracts and foreign exchange rate contracts on behalf of customers. The Company minimizes its market and... -

Page 49

...to interest rate risk during the period between issuing a loan commitment and the sale of the loan into the secondary market. Related to its mortgage banking operations, the Company held $1.0 billion of forward commitments to sell mortgage loans and $1.0 billion of unfunded mortgage loan commitments... -

Page 50

...various Federal Home Loan Banks (''FHLB'') that provide a source of funding through FHLB advances. The Company maintains a Grand Cayman branch for issuing eurodollar time deposits. The Company also establishes relationships with dealers to issue national market retail and institutional savings certi... -

Page 51

... debt Preferred stock Commercial paper Aa3 A1 A2 P-1 P-1 Aa2 Aa2/P-1 Aa3 A+ A A- A-1 A-1+ AA- AA-/A-1+ A+ F1 A+ A A F1 F1+ AA- A+/F1+ A U.S. Bank National Association Short-term time deposits Long-term time deposits Bank notes Subordinated debt both Moody's Investors Services and... -

Page 52

...on off-balance sheet arrangements for liquidity or capital resources. The Company sponsors an off-balance sheet conduit to which it transferred high-grade investment securities, funded by the issuance of commercial paper. The conduit held assets of $7.3 billion at December 31, 2003, and $9.5 billion... -

Page 53

... the result of corporate earnings, offset primarily by the payment of dividends, including the special dividend of $685 million related to the spin-off of Piper Jaffray, and the repurchase of common stock. On December 16, 2003, the Company increased its dividend rate per common share by 17.1 percent... -

Page 54

...) in average earning assets, primarily due to increases in investment securities, residential mortgages and retail loans, partially offset by a decline in commercial loans and loans held for sale related to mortgage banking activities. The net interest margin for the fourth quarter of 2003 was 4.42... -

Page 55

... from net free funds due to lower average interest rates. In addition, the net interest margin declined year-over-year as a result of consolidating high credit quality, low margin loans from the Stellar commercial loan conduit onto the Company's balance sheet during the third quarter of 2003. Fourth... -

Page 56

... by major lines of business, which include Wholesale Banking, Consumer Banking, Private Client, Trust and Asset Management, Payment Services, and Treasury and Corporate Support. These operating segments are components of the Company about which ï¬nancial information is available and is evaluated... -

Page 57

... increase in cash management-related fees was driven by growth in product sales, pricing enhancements and lower earnings credit rates to customers. The growth was also driven by a change in the Federal government's payment methodology for treasury management services from compensating balances, re... -

Page 58

... securities gains was $1,460.1 million in 2003, $42.4 million (3.0 percent) higher compared with 2002. This growth was driven by mortgage banking revenue, deposit service charges, investment products fees and commissions and acquisitions, partially offset by higher end-of-term lease residual... -

Page 59

...and Asset Management 2003 2002 Percent Change 2003 Payment Services 2002 Percent Change information on factors impacting the credit quality of the loan portfolios. Private Client, Trust and Asset Management provides trust, private banking, ï¬nancial advisory, investment management and mutual fund... -

Page 60

..., risk management and the sale of two co-branded credit card portfolios during late 2002. Treasury and Corporate Support includes the Company's cards, corporate and purchasing card services, consumer lines of credit, ATM processing, merchant processing and debit cards. Payment Services contributed... -

Page 61

... for credit losses. ACCOUNTING CHANGES alternative accounting methods may be utilized under generally accepted accounting principles. Management has discussed the development and the selection of critical accounting policies with the Company's Audit Committee. Signiï¬cant accounting policies are... -

Page 62

...comparison of fair value to the carrying value. The determination of fair value can be highly subjective, especially for assets that are not actively traded or when market-based prices are not available. The Company estimates fair value based on the present value of estimated future cash ï¬,ows. The... -

Page 63

...the end of the period covered by this report, the Company's disclosure controls and procedures were effective to ensure that information required to be disclosed by the Company in reports that it ï¬les or submits under the Exchange Act is recorded, processed, summarized and reported within the time... -

Page 64

... Consolidated Balance Sheet At December 31 (Dollars in Millions) 2003 2002 Assets Cash and due from banks Investment securities Held-to-maturity (fair value $161 and $240, respectively Available-for-sale Loans held for sale Loans Commercial Commercial real estate Residential mortgages... -

Page 65

... Noninterest Income Credit and debit card revenue Corporate payment products revenue ATM processing services Merchant processing services Trust and investment management fees Deposit service charges Treasury management fees Commercial products revenue Mortgage banking revenue Investment... -

Page 66

... income Cash dividends declared on common stock **** Special dividend-Piper Jaffray spin-off ********* Issuance of common stock and treasury shares ** Purchase of treasury stock Stock option grants and restricted stock amortization Shares reserved to meet deferred compensation obligations... -

Page 67

... Gain) loss on sales of securities and other assets, net Mortgage loans originated for sale in the secondary market, net of repayments ********** Proceeds from sales of mortgage loans Stock-based compensation Other, net Net cash provided by (used in) operating activities 3,732.6 1,254.0 275... -

Page 68

... market and small businesses through banking ofï¬ces, telemarketing, on-line services, direct mail and automated teller machines (''ATMs''). Private Client, Trust and Asset Management provides trust, private banking, ï¬nancial advisory, investment management and mutual fund processing services... -

Page 69

... with mortgage banking activities are considered derivatives and recorded on the balance sheet at fair value with changes in fair value recorded in income. All other unfunded loan commitments are generally related to providing credit facilities to customers of the bank and are not actively traded... -

Page 70

...ability to meet the revised payment schedule is not reasonably assured, the loan remains classiï¬ed as a nonaccrual loan. Leases The Company engages in both direct and leveraged transferred to LHFS to be marked-to-market (''MTM'') at the time of transfer. MTM losses related to the sale/transfer of... -

Page 71

...payments of high quality corporate bonds available in the market place to projected cash ï¬,ows as of the measurement date for future beneï¬t payments. Periodic pension expense (or credits) includes service costs, interest costs based on the assumed discount rate, the expected return on plan assets... -

Page 72

... reporting cash Derivative Instruments and Hedging Activities In April ï¬,ows, cash and cash equivalents include cash and money market investments, deï¬ned as interest-bearing amounts due from banks, federal funds sold and securities purchased under agreements to resell. Stock-Based Compensation... -

Page 73

...the commercial paper funding of Stellar Funding Group, Inc., the commercial loan conduit. This action caused the conduit to lose its status as a qualifying special purpose entity. As a result, the Company recorded all of Stellar's assets and liabilities at fair value and the results of operations in... -

Page 74

... original acquiring company: (Dollars and Shares in Millions) Date Assets (a) Deposits Goodwill and Other Intangibles Cash Paid / (Received) Shares Issued Accounting Method Corporate Trust business of State Street Bank and Trust Company ***** Bay View Bank branches The Leader Mortgage Company, LLC... -

Page 75

...: 2003 2002 Assets Cash and cash equivalents Trading securities Loans Goodwill Other assets (a Total assets Liabilities Deposits Short-term borrowings Long-term debt Other liabilities (b Total liabilities (a) Includes customer margin account receivables, due from brokers/dealers and... -

Page 76

... and employee-related Stock-based compensation Systems conversions and integration Asset write-downs and lease terminations Charitable contributions Balance sheet restructurings Branch sale gain Branch consolidations Other merger-related items Total 2001 Provision for credit losses... -

Page 77

... the acquisition cost at the applicable closing date. Balance sheet restructurings primarily represent gains or losses incurred by the Company related to the disposal of certain businesses, products, or customer and business relationships that no longer align with the long-term strategy of... -

Page 78

... provided for in the Company's severance plans. In 2003, the integration of merchant processing platforms and business processes of U.S. Bank National Association and NOVA, as well as systems conversions for the acquisitions of the State Street Corporate Trust business and Bay View were completed... -

Page 79

... represent 43 trust preferred securities from 13 bank issuers. All principal and interest payments are expected to be collected given the high credit quality of the bank holding company issuers and the Company's ability and intent to hold the investments until such time as the value recovers or... -

Page 80

...Home Loan Bank. Loans of $12.1 billion at December 31, 2003, and $12.7 billion at December 31, 2002, were pledged at the Federal Reserve Bank. The Company primarily lends to borrowers in the 24 states in which it has banking ofï¬ces. Collateral for commercial loans may include marketable securities... -

Page 81

... 31, 2003, the allowance for credit losses includes an estimated $133.6 million credit loss liability related to the Company's $58.3 billion of commercial off-balance sheet loan commitments and letters of credit. Note 9 Accounting for Transfers and Servicing of Financial Assets and Extinguishments... -

Page 82

...'s balance sheet at fair value. The indirect automobile securitization held $156.1 million in assets at December 31, 2002. During the third quarter of 2003, the Company elected not to reissue more than 90 percent of the commercial paper funding of Stellar Funding Group, Inc., the commercial loan... -

Page 83

... Indirect Automobile Loans Unsecured Small Business Receivables (a) Commercial Loans Investment Securities 2003 Proceeds from New sales and securitizations Collections used by trust to purchase new receivables in revolving securitizations Servicing and other fees received and cash ï¬,ows on... -

Page 84

... rate changes. The Company also, from time to time, purchases principal-only securities that act as a partial economic hedge. The Company is able to recognize reparations from increases in fair value of servicing rights when impairment reserves are released. The fair value of mortgage servicing... -

Page 85

...of the Company's mortgage servicing rights and related characteristics by portfolio as of December 31, 2003, is as follows: (Dollars in Millions) Leader Mortgage U.S. Bank Home Mortgage Conventional Government Total Servicing portfolio Fair market value Value (bps Weighted-average servicing fees... -

Page 86

...the changes in the carrying value of goodwill for the years ended December 31, 2002 and 2003: Wholesale Banking Consumer Banking Private Client, Trust and Asset Management Payment Services Capital Markets (a) Consolidated Company (Dollars in Millions) Balance at December 31, 2001 ******** Goodwill... -

Page 87

...: 2003 (Dollars in Millions) Amount Rate Amount 2002 Rate Amount 2001 Rate At year-end Federal funds purchased Securities sold under agreements to repurchase ******** Commercial paper Treasury, tax and loan notes Other short-term borrowings Total Average for the year Federal funds purchased... -

Page 88

... Company) Fixed-rate subordinated notes 7.00% due 2003 6.625% due 2003 7.25% due 2003 8.00% due 2004 7.625% due 2005 6.75% due 2005 6.875% due 2007 7.30% due 2007 7.50% due 2026 Senior contingent convertible debt 1.50% due 2021 Medium-term notes Capitalized lease obligations, mortgage... -

Page 89

... in 2006 and 2007 in the amounts of $2.3 billion and $300 million, respectively. The Trust Preferred Securities qualify as Tier I capital of the Company for regulatory capital purposes. The Company used the proceeds from the sales of the Debentures for general corporate purposes. U.S. Bancorp 87 -

Page 90

... 31, 2003, the Company had 208.0 million shares of common stock reserved for future issuances, primarily under stock option plans. The Company has a preferred share purchase rights plan intended to preserve the long-term value of the Company by discouraging a hostile takeover of the Company. Under... -

Page 91

... affecting Other Comprehensive Income included in shareholders' equity for the years ended December 31, is as follows: Transactions (Dollars in Millions) Pre-tax Tax-effect Net-of-tax Balance Net-of-tax 2003 Unrealized loss on securities available-for-sale Unrealized loss on derivatives Realized... -

Page 92

...discount rate and the long-term rate of return (''LTROR''). At least annually, an independent consultant is engaged to assist U.S. Bancorp's Compensation Committee in evaluating plan objectives, funding policies and plan investment policies considering its long-term investment time horizon and asset... -

Page 93

...existing practices, the independent pension consultant utilized by the Company updated the analysis of expected rates of return and evaluated peer group data, market conditions and other factors relevant to determining the LTROR assumptions for pension costs for 2003 and 2004. The analysis performed... -

Page 94

... in the qualiï¬ed pension plan associated with the Piper Jaffray Companies are included in the pension plans beneï¬t obligation. (c) At December 31, 2003 and 2002, the Company's qualiï¬ed pension plans held 799,803 shares of U.S. Bancorp common stock, with a fair value of $23.8 million and... -

Page 95

... medical plan actuarial computations Expected long-term return on plan assets Discount rate in determining beneï¬t obligations Health care cost trend rate (d) Prior to age 65 After age 65 Effect of one percent increase in health care cost trend rate Service and interest costs Accumulated... -

Page 96

... merger agreements. The historical stock award information presented below reï¬,ects awards originally granted under acquired companies' plans. At December 31, 2003, there were 41.8 million shares (subject to adjustment for forfeitures) available for grant under our current stock incentive plan... -

Page 97

... of fair value adjustments on securities available-for-sale, derivative instruments in cash ï¬,ow hedges and certain tax beneï¬ts related to stock options are recorded directly to shareholders' equity as part of other comprehensive income. In preparing its tax returns, the Company is required... -

Page 98

... Consolidated Financial Statements for a discussion of the Company's accounting policies for derivative instruments. For information related to derivative positions held for asset 96 U.S. Bancorp and liability management purposes and customer-related derivative positions, see Table 17 ''Derivative... -

Page 99

...million, related to the Company's mortgage loans held for sale and its 2003 production volume of $29.9 billion. Other Asset and Liability Management Derivative Positions amounts due from banks, federal funds sold and securities purchased under resale agreements was assumed to approximate fair value... -

Page 100

...-end. The fair value of ï¬xed-rate certiï¬cates of deposit was estimated by discounting the contractual cash ï¬,ow using the discount rates implied by the high-grade corporate bond yield curve. Short-term Borrowings Federal funds purchased, securities subordinated debentures of the parent company... -

Page 101

... guarantees frequently support public and private borrowing arrangements, including commercial paper issuances, bond financings and other similar transactions. The Company issues commercial letters of credit on behalf of customers to ensure payment or collection in connection with trade transactions... -

Page 102

... accounting principles. The guaranteed operating lease payments are also included in the disclosed minimum lease obligations. Commitments from Securities Lending The Company participates in securities lending activities by acting as the customer's agent involving the loan or sale of securities... -

Page 103

... processing contracts consider the potential risk of default. At December 31, 2003, the value of future delivery airline tickets purchased was approximately $1.4 billion, and the Company held collateral of $188.7 million in escrow deposits and lines of credit related to airline customer transactions... -

Page 104

...U.S. Bancorp (Parent Company) Condensed Balance Sheet December 31 (Dollars in Millions) 2003 2002 Assets Deposits with subsidiary banks, principally interest-bearing Available-for-sale securities Investments in Bank and bank holding company subsidiaries Nonbank subsidiaries (a Advances to Bank... -

Page 105

... activities Change in cash and cash equivalents Cash and cash equivalents at beginning of year Cash and cash equivalents at end of year Transfer of funds (dividends, loans or advances) from bank subsidiaries to the Company is restricted. Federal law prohibits loans unless they are secured... -

Page 106

...: (Dollars in Millions) 2003 2002 Interest-bearing deposits Federal funds sold Securities purchased under agreements to resell Total money market investments $ 4 109 39 $102 61 271 $434 $152 Regulatory Capital The measures used to assess capital Net Gains on the Sale of Loans Included in... -

Page 107

... in 2003 the Company changed its method of accounting for stock-based employee compensation. Report of Independent Accountants To the Shareholders and Board of Directors of U.S. Bancorp: In our opinion, the accompanying consolidated balance sheet as of December 31, 2002 and the related consolidated... -

Page 108

...Bancorp Consolidated Balance Sheet - Five-Year Summary December 31 (Dollars in Millions) 2003 2002 2001 2000 1999 % Change 2003 v 2002 Assets Cash and due from banks Held-to-maturity securities Available-for-sale securities Loans held for sale Loans Less allowance for credit losses Net loans... -

Page 109

... services Credit card and payment processing revenue Trust and investment management fees Deposit service charges Treasury management fees Commercial products revenue Mortgage banking revenue Investment products fees and commissions Securities gains, net Merger and restructuring-related... -

Page 110

...Noninterest Income Credit and debit card revenue Corporate payment products revenue ********* ATM processing services Merchant processing services Trust and investment management fees ******* Deposit service charges Treasury management fees Commercial products revenue Mortgage banking revenue... -

Page 111

... ï¬led on Form 10-Q with the Securities and Exchange Commission have been retroactively restated to give effect to the spinoff of Piper Jaffray Companies on December 31, 2003, and the adoption of the fair value method of accounting for stock-based compensation. The accounting change was adopted... -

Page 112

... Daily Average Balance Sheet and Related Yields Year Ended December 31 Average Balances 2003 Yields and Rates Average Balances 2002 Yields and Rates (Dollars in Millions) Interest Interest Assets Taxable securities Non-taxable securities Loans held for sale Loans (b) Commercial Commercial... -

Page 113

and Rates (a) 2001 Average Balances Yields and Rates Average Balances 2000 Yields and Rates Average Balances 1999 Yields and Rates 2003 v 2002 % Change Average Balances Interest Interest Interest $ 20,....3 9.1% 7.67% 3.21 4.46 4.43% 8.63% 4.25 4.38 4.32% 7.99% 3.56 4.43 4.36% U.S. Bancorp 111 -

Page 114

... 20549 Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the ï¬scal year ended December 31, 2003 Commission File Number 1-6880 U.S. Bancorp Incorporated in the State of Delaware IRS Employer Identiï¬cation #41-0255900 Address: 800 Nicollet Mall Minneapolis... -

Page 115

... purchasing card services and corporate trust services in the United States. A wholly-owned subsidiary, NOVA Information Systems, Inc., provides merchant processing services directly to merchants and through a network of banking afï¬liations. On a full-time equivalent basis, employment during 2003... -

Page 116

... securities, payment of dividends, establishment of branches and other aspects of operations. Properties U.S. Bancorp and its signiï¬cant subsidiaries occupy headquarter ofï¬ces under a long-term lease in Minneapolis, Minnesota. The Company also leases eight effect as of December 31, 2003. Number... -

Page 117

... and Exchange Commission. Guidelines, Code of Ethics and Business Conduct and Board of Directors committee charters are available free of charge on our web site at usbank.com, by clicking on ''About U.S. Bancorp,'' then ''Investor/Shareholder Information.'' Shareholders may request a free printed... -

Page 118

...fair value'' method of accounting for stock-based compensation; and ) Form 8-K dated January 20, 2004, relating to fourth quarter 2003 earnings. The following Exhibit Index lists the Exhibits to the Annual Report on Form 10-K. (1) (1)(2) 10.4 Summary of U.S. Bancorp 1991 Executive Stock Incentive... -

Page 119

...Bancorp Outside Directors Deferred Compensation Plan. (2) (1)(2) 10.20 Form of Change in Control Agreement, effective November 16, 2001, between U.S. Bancorp and certain executive ofï¬cers of U.S. Bancorp. Filed as Exhibit 10.12 to Form 10-K for the year ended December 31, 2001. 10.21 Employment... -

Page 120

... by the undersigned, thereunto duly authorized. U.S. Bancorp By: Jerry A. Grundhofer Chairman, President and Chief Executive Ofï¬cer Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below on February 27, 2004, by the following persons on behalf of the... -

Page 121

...SECURITIES EXCHANGE ACT OF 1934 I, Jerry A. Grundhofer, Chief Executive Ofï¬cer of U.S. Bancorp, a Delaware corporation, certify that: (1) I have reviewed this annual report on Form 10-K of U.S. Bancorp; (2) Based on my knowledge, this report does not contain any untrue statement of a material fact... -

Page 122

... SECURITIES EXCHANGE ACT OF 1934 I, David M. Moffett, Chief Financial Ofï¬cer of U.S. Bancorp, a Delaware corporation, certify that: (1) I have reviewed this annual report on Form 10-K of U.S. Bancorp; (2) Based on my knowledge, this report does not contain any untrue statement of a material fact... -

Page 123

...cer of U.S. Bancorp, a Delaware corporation (the ''Company''), do hereby certify that: (1) The Annual Report on Form 10-K for the year ended December 31, 2003 (the ''Form 10-K'') of the Company fully complies with the requirements of section 13(a) or 15(d) of the Securities Exchange Act of 1934; and... -

Page 124

... Consumer Banking, including Retail Payment Solutions (card services). Mr. Davis assumed additional responsibility for Commercial Banking in 2003. Previously, he had been Vice Chairman of Consumer Banking of Firstar Corporation from 1998 until 2001 and Executive Vice President, Consumer Banking of... -

Page 125

... National Financial Services, Inc. Cincinnati, Ohio O'dell M. Owens, M.D., M.P.H.4,6 Healthcare Consultant Cincinnati, Ohio 1. 2. 3. 4. 5. 6. Executive Committee Compensation Committee Audit Committee Community Outreach and Fair Lending Committee Governance Committee Credit and Finance Committee... -

Page 126

..., news releases, quarterly financial data reported on Form 10-Q and additional copies of our annual reports. Please contact: U.S. Bancorp Investor Relations 800 Nicollet Mall Minneapolis, MN 55402 [email protected] Phone: 612-303-0799 or 866-775-9668 Common Stock Transfer Agent and... -

Page 127

U.S. Bancorp 800 Nicollet Mall Minneapolis, MN 55402 usbank.com