Ingram Micro 2008 Annual Report Download - page 3

Download and view the complete annual report

Please find page 3 of the 2008 Ingram Micro annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

AND YOU

Dear Fellow Shareholders:

2008 will be remembered as the start of a recession that severely impacted many companies around the world.

It also will be remembered as the year that unveiled Ingram Micro’s fighting spirit.

We stood firmly on the bedrock

of our financial position, taking

decisive actions to improve the

business in an unstable environ-

ment. The ongoing support we

received from you — our share-

holders, associates, customers,

suppliers and other stakeholders —

helped us deliver results that make us proud. Here are

some of the year’s highlights:

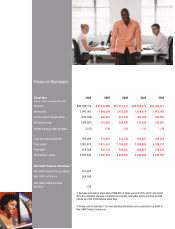

• Sales topped $34 billion, the second-highest level in

our history

• Gross margins were at the highest level in 10 years

• Excellent management of working capital helped

generate operating cash flow of more than $550 million

for the year

• Year-end cash balance peaked to

a record amount of $763 million,

even after repurchasing $222

million in company stock during

the year.

Although I’m pleased with our

achievements in 2008, we are far

from claiming victory. As we move

through 2009, worldwide market weakness continues to

dampen sales. Aligning our cost structure with the pace

of decline will remain a challenge, but a top priority for the

management team. As 2008 so aptly illustrated, a small

drop in sales in a growth industry can exert tremendous

pressure on profits and return on invested capital — even

when cost adjustment measures are

instituted early in the cycle.

Decisive Actions, Steady Results

Starting April 2008, we began to take

concrete actions in North America

and Europe. In Europe, we down-

sized our regional headquarters,

while in North America, we re-engi-

neered certain back-office functions. We also focused on

traditional belt-tightening efforts — significantly lowering

travel costs, reducing hiring and taking steps to improve

processes for the long term. By the

end of the year, the benefit of these

actions reached a run-rate of more

than $20 million in annual savings.

While Asia-Pacific and Latin Amer-

ican economies were relatively unaf-

fected during the first half of 2008,

those regional management teams

proactively implemented cost-containment programs of

their own. This forethought proved to be extremely benefi-

cial when their economies worsened later in the year.

As growth rates continued to decline globally, improving

our profitability became paramount. We shed certain

less-profitable and low-return business relationships

worldwide, recognizing that top-line revenues would be

impacted through these moves.

While almost all customer segments

and product lines were scrutinized,

the majority of our actions were

directed at retail throughout Europe

and in China. Our decision to

consciously walk away from those

business opportunities that did not

meet our profitability thresholds

made a positive impact on our gross margin performance

for the year.

Pruning our business was only part of the gross margin

story. Our data capture/point-of-sale (DC/POS), network-

ing, enterprise solutions and North American logistics

businesses — all strong gross margin contributors —

grew significantly above the

company’s average sales growth.

Following the mid-year spike in fuel

prices, we introduced incremental

freight charges to offset transporta-

tion costs. Our industry was one of

the few to continue to bear the

burden of freight costs, and we

felt it was time to change that

practice for the long-term benefit of IT distribution.

Many of our peers soon followed suit, validating our

leadership stance.

12

YEARS PUBLIC

108

DISTRIBUTION CENTERS

14,500

EMPLOYEES