Aviva 2005 Annual Report Download

Download and view the complete annual report

Please find the complete 2005 Aviva annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

Aviva plc

Annual Report and Accounts 2005

Table of contents

-

Page 1

Aviva plc Annual Report and Accounts 2005 -

Page 2

... 24 Long-term savings and fund management 32 General insurance, health and related services Other corporate information 38 Group capital structure 39 Group capital strength and solvency 42 Corporate social responsibility 44 Employees 46 Financial reporting 47 Risk and risk management Governance 52... -

Page 3

... customers, partners and the communities in which we operate. Financial highlights Aviva plc 2005 Overview £2,528m £2,904m 15.0% IFRS proï¬t before tax attributable to shareholders* EEV operating proï¬t** Return on capital employed†£35.0bn 27 .27p Worldwide sales‡ Full year dividend... -

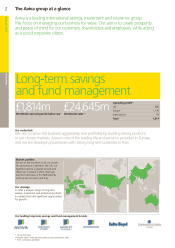

Page 4

...a good corporate citizen. Long-term savings and fund management £1 ,814m Our credentials Worldwide operating proï¬t before tax* Worldwide sales** £24,645m Operating proï¬t* UK Europe International Total 585 1,130 99 1,814 We aim to grow this business aggressively and proï¬tably by building... -

Page 5

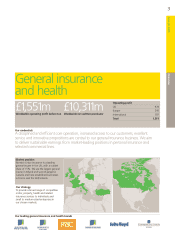

... £10,31 1m Worldwide net written premiums†Operating proï¬t UK Europe International Total 974 390 187 1,551 A disciplined and efï¬cient core operation, increased access to our customers, excellent service and innovative propositions are central to our general insurance business. We aim to... -

Page 6

4 Aviva plc 2005 Overview Chairman's statement Group performance Our business is increasingly multinational. During 2005, for the ï¬rst time, our long-term savings new business premiums from continental Europe exceeded 50% of the group total. We have announced a major bancassurance deal in Ireland... -

Page 7

.... Commercial Union Poland was named life insurance company of the decade by Home & Market magazine, reï¬,ecting the consistently high quality of our products and services. Further success was achieved by Morley Fund Management, named as property manager of the year at the UK Pensions Awards, and... -

Page 8

... return on capital employed was 15%* (2004: 13.7%). Worldwide long-term savings new business sales were £24.6 billion (2004: £22.3 billion), reï¬,ecting strong international sales growth and continued success in the bancassurance channel. Pre-tax life operating return on a European embedded value... -

Page 9

... of distribution, products and geography. Our business model provides capital to fund new business growth and acquisitions, and to support dividend growth. Our international long-term savings operations continue to grow strongly, and we have a positive outlook on our competitive position in the UK... -

Page 10

... ï¬rst international insurer to open an ofï¬ce in some of these cities. China is an important long-term market for Aviva, and we are pleased to be able to continue our expansion. Overview £24.6bn Present value of new business premiums (PVNBP)* +10% Growth in PVNBP* Long-term savings and fund... -

Page 11

... Bond. The bond uses derivatives to generate higher income for customers than could normally be expected from a standard investment portfolio. Aviva plc 2005 Poland: life company of the decade We received a golden parasol award from Home & Market magazine for being Poland's life insurance company... -

Page 12

..., direct from customers, what they see as key elements of good service. Customer call centre image to come We are a leading online insurer Norwich Union Direct celebrated its 10th anniversary as one of the UK's leading direct insurers, with almost four million policies now in force. The business... -

Page 13

... and cost-saving beneï¬ts. Leveraging group knowledge Knowledge gained from HPI, digital ï¬,ood mapping and our Pay As You Driveâ„¢ scheme has allowed us to improve our pricing decisions. Our Canadian business is now serviced by more than 150 staff in India, beneï¬ting from cost and service... -

Page 14

... all new pensions policies under a single scheme thereby enabling customers to move seamlessly between products and tailor their retirement planning to their own needs. Further details of our CSR programme can be found on pages 42 to 44. Alternatively a printed summary copy of our annual CSR report... -

Page 15

...issues. In our corporate ofï¬ce, staff have a quarterly opportunity to nominate a colleague or a team who have exempliï¬ed one or more of the Aviva values. Providing the tools to help employees make a difference and measuring progress is very important. Financial reward schemes now recognise those... -

Page 16

We're helping to create prosperity and for millions of people peace around the world -

Page 17

Aviva plc 2005 of mind Business review Group overview 16 17 18 Basis of preparation Strategy and values Financial position and performance Business review -

Page 18

...position on an management remuneration. International Financial Reporting Standards basis, we also use European Embedded Value (EEV) as an alternative performance measure. Details of the accounting basis of preparation are set out in the 'ï¬nancial reporting' section of this business review on page... -

Page 19

... insurance group and the largest insurance services provider in the UK. We are one of the leading providers of life and pension products in Europe and are actively growing long-term savings businesses in Asian markets, Australia and the USA. Our main activities are long-term savings, fund management... -

Page 20

...ï¬,ecting strong operation performance and strong equity market performance. EEV basis IFRS basis * Return on capital employed is calculated using after-tax return and opening equity capital, based on operating proï¬t, including long-term savings proï¬t on an European Embedded Value basis before... -

Page 21

...ï¬t before tax 2,128 1,669 2,904 2,224 *The proportion of the results of the group's UK and French asset management operation, the results of Norwich Union Equity Release and the proportion of the results of Norwich Union Life Services operation that arise from the provision of fund management and... -

Page 22

... impairment of acquired value of in-force business Amortisation and impairment of intangibles Financial Services Compensation Scheme and other levies Short term ï¬,uctuation in return on investments backing general insurance and health business Variation from longer-term investment return Effect of... -

Page 23

... to both the Norwich Union and RAC pension schemes of £700 million over the next two years. It is expected that 12% of the payments to the Norwich Union scheme will be made from the UK with-proï¬t funds, and the remainder will be paid from the Group's internal resources. In anticipation that... -

Page 24

millions of ret -

Page 25

Aviva plc 2005 Business review Business segment performance 24 32 Long-term savings and fund management General insurance, health and related services Business review irements across Europe safeguarding We're -

Page 26

...review continued Business segment performance: Long-term savings and fund management Long-term savings 2005 IFRS proï¬t before tax £m IFRS operating proï¬t £m EEV operating proï¬t £m New business PVNBP* contribution £m £m New business margin % UK Our UK business, operating as Norwich Union... -

Page 27

... to a cost effective form of distribution for insurance products. We have expertise in product design, insurance risk management, service delivery and the sales process for insurance products. Particularly important for our success is our knowledge and experience of making bancassurance partnerships... -

Page 28

26 Aviva plc 2005 Business review Business review continued Business segment performance: Long-term savings and fund management continued France Aviva France is one of the top 10 long-term savings businesses in France with a market share of 5%. It focuses on higher-margin unit-linked products in ... -

Page 29

... of the banks customer bases and cross-selling in all of our major relationships. Business review Our life EEV operating return rose to £214 million (2004: £180 million) due to higher new business contribution as a result of a beneï¬cial change in product mix. Total sales were £2,013... -

Page 30

...including bancassurance. Single premium pension sales were boosted by transfers from existing life policies ahead of an October 2006 regulatory deadline. Our other European operations are seeking to achieve strong organic growth with unit-linked savings products focused on high-net-worth individuals... -

Page 31

...with distribution through independent agents and banks. During 2005, six new products were launched, including two ï¬xed-indexed annuities and a deferred annuity tailored for the bank channel. During 2006, we expect sales growth through our existing lines of business supported by the recent ratings... -

Page 32

...the UK, we sell retail Isas, unit trusts, open-ended investment companies (Oeics) and During 2005, we launched a number of new institutional and retail structured products under the Norwich Union and The Royal Bank funds, sold under the Morley and Norwich Union brand names in of Scotland Group (RBSG... -

Page 33

... in product offerings and customer service. Singapore reported signiï¬cantly higher sales of £90 million (2004: £13 million) reï¬,ecting strong distribution relationships with key brokers and an increased fund choice. Investing in property Morley's property business Morley Property is... -

Page 34

... homeowner rates (2004: 6%). Commercial rates are holding up well and proï¬tability remains strong. Our total UK result also includes Norwich Union Healthcare, a leading UK health insurer providing private medical insurance We acquired RAC in May 2005 and have made signiï¬cant progress and income... -

Page 35

... high quality healthcare services. The Autograph motor insurance product, providing pay-as-you-drive cover, has been successfully piloted. Signiï¬cant investment in supply chain initiatives and development of our offshore operations in India will allow us to improve customer and broker satisfaction... -

Page 36

... review continued Business segment performance: General insurance, health and related services continued Ireland Hibernian is the largest general insurer in Ireland, with a market share of 21%. Around 65% of our business is via brokers, with the remainder being split between direct and corporate... -

Page 37

...ï¬,ecting rating increases in commercial and health lines. commercial insurance through networks of agents and brokers. The longer-term investment return was higher at £56 million We also have a healthcare business in Asia. (2004: £49 million). Our general insurance business reported an unchanged... -

Page 38

to -

Page 39

trusted protect 17% of the UK's homeowners Business review Other corporate information 38 39 42 44 46 47 Group capital structure Group capital strength and solvency Corporate social responsibility Employees Financial reporting Risk and risk management We're Aviva plc 2005 Business review -

Page 40

...proï¬t was 9.6 times (2004: 8.7 times). Long-term savings General insurance and health Other business Corporate Total capital employed Financed by Equity shareholders' funds and minority interests Direct capital instrument Preference shares Subordinated debt External debt Net internal debt 15,598... -

Page 41

... and the capital raised as part of the acquisition of RAC in May. Accordingly, our net asset value per ordinary share, based on equity shareholders' funds, was higher at 622 pence per share. Regulatory bases - EU group's directive 2005 2004 Insurance Groups Directive (IGD) Cover (times) £3.5bn... -

Page 42

...be paid to in-force policyholders at the valuation date in respect of smoothing costs and guarantees. Realistic balance sheet information is shown below for the three UK with-proï¬t funds, CGNU Life (CGNUL), Commercial Union Life Assurance Company (CULAC) and Norwich Union Life and Pensions Having... -

Page 43

... minimum margin) was £5.4 billion (31 December 2004: £5.7 billion) after covering the minimum capital base of £4.3 billion (31 December 2004: £4.1 billion). Economic bases We use a number of measures of risk based capital to assess the capital requirements for our general insurance businesses... -

Page 44

...: our long-term savings, fund management and general insurance businesses in the UK. Long-term savings 2005 saw Norwich Union create a three-year vision, which focuses on building the trust and conï¬dence of our customers. Our aim is to provide a high level of trust, value and support to customers... -

Page 45

... with the largest companies in Europe to encourage higher standards of corporate social responsibility. Business review General insurance Norwich Union Insurance has embarked on a journey to be recognised by customers and non-customers as a great service provider. Since 2002, all employees have been... -

Page 46

... products and services that provide a positive link between climate change and premium paid, for example Norwich Union's Pay As You Driveâ„¢ product. We also use the investment inï¬,uence of our fund management subsidiaries to encourage environmentally responsible behaviour. Employee numbers... -

Page 47

...in the annual bonus awards for senior managers from 2006 onwards. We continue to deliver value to our customers through lower cost, 24-hour claims processing and sales facilities in India and Sri Lanka. More than 4,300 people are now servicing Aviva general and life insurance customers in the UK and... -

Page 48

... by the European Union (EU) methodology to align the equity and property rates used in the requiring all European listed companies to prepare consolidated calculation with the rates used under EEV principles. We have also ï¬nancial statements using standards issued by the International changed the... -

Page 49

... to manage group-wide risk exposures. We have exposure to the full range of life insurance risks, including a signiï¬cant exposure to annuity business and the associated longevity risk. Longevity statistics are monitored in detail and the results are used to inform the reserving for, and pricing of... -

Page 50

..., long-term debt and ï¬xed income securities are exposed to ï¬,uctuations in interest rates. Exposure to interest rate risk is monitored through several measures, including Value-at-Risk analysis, position limits, scenario testing, stress testing and asset and liability matching using measures... -

Page 51

...information security, human resources, project management, outsourcing, tax, legal, fraud and compliance. In accordance with group-wide policies, line management in business units has primary responsibility for the effective identiï¬cation, management, monitoring and reporting of operational risks... -

Page 52

for commitment to socially respected investment We're respo -

Page 53

Aviva plc 2005 nsible Governance 52 54 57 62 64 65 75 Board of directors Directors' report Corporate governance Audit committee report Nomination committee report Directors' remuneration report Independent auditors' report Governance -

Page 54

... nomination and corporate social group in 1989, holding a number of senior positions responsibility committees. before joining the board of Norwich Union in 1999. Currently responsible for the group's United Kingdom businesses namely Norwich Union Insurance, Norwich Union Life and RAC. A member of... -

Page 55

... member of the audit committee. Governance Appointed to the board in May 2004. Currently a non-executive director of the Warnaco Group Inc (clothing), Federal Home Loan Mortgage Corporation (Freddie Mac) (ï¬nancial services), New Germany Fund (investment trust) and a director of The London School... -

Page 56

... under the Group's employee share and incentive 2005 companies will be required to produce a business review as plans and the Aviva Scrip Dividend Scheme. At 31 December 2005 part of their directors' report in respect of ï¬nancial years beginning the issued ordinary share capital totalled 2,395... -

Page 57

..., interest rates, equity and property prices. Details of the objectives and management of these instruments are contained in the Business Review on pages 16 to 49 and an indication of the exposure of the Group companies to such risks is contained in note 51 to the accounts on page 188. Health and... -

Page 58

... business Meeting and a description of the business to be conducted thereat. unit intranets), Aviva radio, which can be accessed via mobile phone or computer, and poster campaigns. Employees have opportunities By order of the Board. to voice their opinions and ask questions through intranet sites... -

Page 59

...ï¬ed limit regarding the number effectively controlled. The speciï¬c duties of the Board are clearly set of terms a director may serve. All directors are required to be out in terms of reference which address a wide range of corporate elected by shareholders at the Annual General Meeting following... -

Page 60

... is the executive director responsible for the Group's international businesses and Morley, the United Kingdom fund management business. Patrick Snowball is the executive director responsible for the Group's UK businesses namely Norwich Union Insurance, Norwich Union Life and RAC. Carole Piwnica is... -

Page 61

... international ï¬nancial reporting standards and the assessment of the Group's capital requirements. Further tailored training sessions have been built into the Board's work plan for 2006. The Board made two site visits during the year to gain a closer understanding of the Group's businesses... -

Page 62

... against the plan is subsequently monitored and reported to the Board each time it meets. This report also includes reports on risk, audit, compliance, solvency and liquidity. Performance is also reported through the half-yearly publication of Group results based on accounting policies that are... -

Page 63

...Company's website. All material information reported to the regulatory news services is simultaneously published on the Company's website affording all shareholders full access to Company announcements. The Company's Annual General Meeting provides a valuable opportunity for the Board to communicate... -

Page 64

... is satisï¬ed that all these directors have recent and relevant ï¬nancial experience. The Committee follows an agreed annual work plan. It reviews, with members of management and the internal and external auditors, the Company's ï¬nancial announcements including the annual report and accounts to... -

Page 65

..., reporting on internal controls, and corporate governance matters, and due diligence work were £3.1 million giving a total fee to Ernst & Young LLP of £13.1 million (2004: £14.9 million). Further details are provided in note 11 on page 124. During the year, the Committee performed its annual... -

Page 66

... also reviews those directors retiring by rotation in accordance with the Company's articles of association with a view to making recommendations to the Board regarding their re-election. The Committee monitors the skill requirements of the Board and the knowledge, experience, length of service and... -

Page 67

... to the Company's performance. It is designed to provide an appropriate balance between the delivery of the annual business plan and the long-term proï¬table growth of the Company. Under this broad policy, the Committee sets the content of the senior executives' total remuneration by reference to... -

Page 68

... elements: - A basic salary; - An annual bonus; - A long-term incentive plan; - A pension provision; - Other beneï¬ts comprising a car allowance and private medical insurance. Basic salaries In determining the level of basic salaries, the Committee gathers data from a number of independent sources... -

Page 69

... 03 Dec 04 Dec 05 Governance comparator group median Dilution Awards granted under the Aviva Annual Bonus Plan 2005 and the Aviva Long-Term Incentive Plan 2005 are met by the issue of new shares at the time that the awards vest. The Committee monitors the number of shares issued under its various... -

Page 70

... car allowance and private cost the Company more than its current arrangements; medical insurance. - The Company would not pay or compensate managers in The Company operates a number of HMRC approved all-employee respect of any increased tax liability arising from pensions share plans in the United... -

Page 71

... will retire on or Service contracts issued since November 2003 meet recommended corporate governance practice, including a speciï¬c requirement for employees to mitigate their losses and the phasing of termination payments over the notice period. During the current year, the Company proposes... -

Page 72

... replacing the Deferred Bonus Plan which operated in 2004. The disclosure of the awards made under these plans differs. Under the Deferred Bonus Plan participants were encouraged to defer their cash bonuses (35% of salary for "Target" performance) into shares by the Company providing matching shares... -

Page 73

... Aviva Staff Pension Scheme, the Group's pension scheme for its United Kingdom employees. For Mr Harvey and Mr Moss, who are subject to the earnings cap, any beneï¬ts that cannot be provided through the Scheme are provided via an Unfunded Unapproved Retirement Beneï¬t (UURB). Executive directors... -

Page 74

... price 31 December at date awards at date awards 2005 granted vested Number p p Vesting date Richard Harvey Aviva Long-Term Incentive Plan - 2000 - 2002 - 2003 - 2004 Aviva Long-Term Incentive Plan 2005 - 2005 Aviva Deferred Bonus Plan - 2002 - 2003 - 2004 - 2005 Andrew Moss Aviva Share Plan Aviva... -

Page 75

... Number Awards lapsing during year Number At Market price Market price 31 December at date awards at date awards 2005 granted vested Number p p Vesting date Philip Scott Aviva Long-Term Incentive Plan - 2000 - 2002 - 2003 - 2004 Aviva Long-Term Incentive Plan 2005 - 2005 Aviva Deferred Bonus Plan... -

Page 76

... Company's various all-employee and executive share schemes. Details of the options and long-term incentive awards are shown on pages 72 to 73 and the Aviva Share Plan is described above. Shares1 1 January 2005 31 December 2005 Bonus Plan Awards2 1 January 2005 31 December 2005 Long-Term Incentive... -

Page 77

...of the International Accounting Standards Board. Financial Services Authority, and we report if it does not. We are not required to consider whether the board's statements on internal In our opinion the group ï¬nancial statements give a true and fair control cover all risks and controls, or form an... -

Page 78

hea the su -

Page 79

...nancial statements Financial statements of the Company Independent auditors' report to the directors of Aviva plc on the alternative method of reporting long-term business proï¬ts 200 Alternative method of reporting long-term business 222 Aviva Group of companies 223 Shareholder services pporting... -

Page 80

... statements Accounting policies Aviva plc (the "Company"), a public limited company incorporated and domiciled in the United Kingdom (UK), together with its subsidiaries (collectively, the "Group" or "Aviva") transacts life assurance and long-term savings business, fund management, and most classes... -

Page 81

..., the Group does in certain businesses, the accounting policies have been changed, as not recognise further losses unless it has incurred obligations or permitted by IFRS 4, to remeasure designated insurance liabilities to made payments on behalf of the entity. reï¬,ect current market interest rates... -

Page 82

... and any part of the general administrative costs directly attributable to the claims function. Long-term business provisions Under current IFRS requirements, insurance and participating investment contract liabilities are measured using accounting policies consistent with those adopted previously... -

Page 83

... used to account for these policies. Financial statements Gains or losses on buying retroactive reinsurance are recognised in the income statement immediately at the date of purchase and are (iii) Liability adequacy At each reporting date, the Group reviews not amortised. Premiums ceded and claims... -

Page 84

... of the Group in Acquired value of in-force business (AVIF) overseas operations. Changes in fair values are recorded in the The present value of future proï¬ts on a portfolio of long-term income statement within net investment income. insurance and investment contracts, acquired either directly or... -

Page 85

... securities are initially recorded at their fair value which is item being hedged. Fair values are obtained from quoted market taken to be amortised cost, with amortisation credited or charged prices or, if these are not available, by using valuation techniques to the income statement. Investments... -

Page 86

...interest rate and other terms that will become a reference point in are deferred and amortised over the life of the loan as an determining, in concert with an agreed notional principal amount, adjustment to loan yield using the effective interest rate method. a net payment to be made by one party to... -

Page 87

... trustee-administered funds. The pension plans are generally funded by payments from employees and by the relevant Group companies, taking account of the recommendations of qualiï¬ed actuaries. For deï¬ned beneï¬t plans, the pension costs are assessed using the projected unit credit method... -

Page 88

... the Group's life share capital or obtains rights to purchase its share capital, the businesses in the UK, Ireland and Australia pay tax on policyholders' consideration paid (including any attributable transaction costs net investment returns ("policyholder tax") on certain products. of income taxes... -

Page 89

... written net of reinsurance Net change in provision for unearned premiums Net premiums earned Fee and commission income Net investment income Share of proï¬t after tax of joint ventures and associates Proï¬t on the disposal of subsidiaries and associates Expenses Claims and beneï¬ts paid, net of... -

Page 90

... of acquired value of in-force business - long-term business subsidiaries - long-term business associates Amortisation and impairment of intangibles Financial Services Compensation Scheme and other levies Short-term ï¬,uctuation in return on investments backing general insurance and health business... -

Page 91

...197 2,708 (8) (136) (436) 2,128 Year ended 31 December 2004 Long-term business £m Fund management £m General insurance and health £m Total £m United Kingdom France Netherlands Other Europe International Other operations Corporate costs Unallocated interest charges 353 213 214 237 99 1,116... -

Page 92

...operations classiï¬ed as held for sale Total assets Equity Capital Ordinary share capital Preference share capital Capital reserves Share premium Merger reserve Shares held by employee trusts Other reserves Retained earnings Equity attributable to shareholders of Aviva plc Direct capital instrument... -

Page 93

... of fair value changes in joint ventures and associates taken to equity Actuarial (losses) on pension schemes Foreign exchange rate movements Reserves credit for equity compensation plans Aggregate tax effect - policyholder tax Aggregate tax effect - shareholder tax Net income recognised directly in... -

Page 94

...ï¬,ows from both policyholder and shareholder activities. Long-term business operations 2005 £m Non-longterm business operations 2005 £m Total 2005 £m Total 2004 £m Note Cash ï¬,ows from operating activities Cash generated from operations Tax paid Net cash from operating activities Cash ï¬,ows... -

Page 95

...provisions of IFRS 2, Share-based Payment, to options and awards granted on or before 7 November 2002 which had not vested by 1 January 2005. Employee beneï¬ts All cumulative actuarial gains and losses on the Group's deï¬ned beneï¬t pension schemes have been recognised in equity at the transition... -

Page 96

... FRS 27, Life Assurance, and of changing the methodology for the Group's longer term investment return. (i) Summarised consolidated balance sheet at date of transition to IFRS - 1 January 2004 UK GAAP as published £m Adjustments £m IFRS £m Assets Goodwill Acquired value of in-force business and... -

Page 97

... (note 1) £m Insurance changes (note 2) £m Employee beneï¬ts (note 3) £m Goodwill (note 4) £m Dividend recognition (note 5) £m Deferred tax (note 6) £m Borrowings/ cash (note 7) £m Other items (note 9) £m Total adjustments £m Assets Goodwill Acquired value of in-force business and... -

Page 98

... of International Financial Reporting Standards continued (ii) Summarised consolidated balance sheet at 31 December 2004 UK GAAP as published £m Adjustments £m IFRS £m Assets Goodwill Acquired value of in-force business and intangible assets Investments in joint ventures and associates Property... -

Page 99

... (note 1) £m Insurance changes (note 2) £m Employee beneï¬ts (note 3) £m Goodwill (note 4) £m Dividend recognition (note 5) £m Deferred tax (note 6) £m Borrowings/ cash (note 7) £m FRS 27 (note 8) £m Other items (note 9) £m Total £m Assets Goodwill Acquired value of in-force business and... -

Page 100

... securities Under UK GAAP, equity securities and unit trusts are carried at current value. Debt and other ï¬xed income securities are carried at current value, with the exception of many non-linked long-term business debt securities and ï¬xed income securities, which are carried at amortised cost... -

Page 101

... and have been valued at fair value. For unit-linked contracts, the fair value liability is deemed to equal the current unit fund value, plus positive non-unit reserves if required on a fair value basis. This replaces the reserve held under UK GAAP which equals the unit fund value plus any positive... -

Page 102

...insurance policies issued by Group companies Total IAS 19 obligations to staff pension schemes Adjustments to other provisions arising under IFRS Provisions as stated under IFRS 336 (78) 838 715 1,553 111 1,922 340 (63) 893 813 1,706 142 2,125 b) Equity compensation plans Under UK GAAP, the costs... -

Page 103

... Group's assets and liabilities under IFRS and presentational changes to disclosure of tax assets and liabilities. The main net increases in deferred tax that reduce shareholders' funds are: 1 January 2004 £m 31 December 2004 £m Financial statements Reversal of discounting (the total discounting... -

Page 104

.... (8) FRS 27 Life Assurance In December 2004, the UK's Accounting Standards Board (ASB) issued Financial Reporting Standard 27, Life Assurance (FRS 27). In accordance with the Memorandum of Understanding (MoU) signed by the Group along with other major insurance companies, the Association of British... -

Page 105

... additional value of in-force long-term business and intangibles Financial Services Compensation Scheme and other levies Short-term ï¬,uctuation in return on investments Change in the equalisation provision Net loss on the disposal of subsidiaries and associates Exceptional costs for termination of... -

Page 106

... increase in the Group's shareholders' funds, and the year-on-year movement in respect of those investments classiï¬ed as "at fair value through proï¬t and loss account" is reported as an increased proï¬t in the 2004 income statement. In addition, changes to investment accounting have resulted in... -

Page 107

... of higher IFRS basis proï¬ts of the in-force book of business. Until mid-2003, unit-linked bond business sold by Norwich Union in the UK contained a guaranteed minimum death beneï¬t, and hence contained signiï¬cant insurance risk, and accordingly, as permitted by IFRS Phase 1, the UK GAAP... -

Page 108

... statements of the Group with effect from 4 May 2005, and contributed £15 million to the consolidated proï¬t before tax. £m Purchase cost Cash paid Fair value of 88 million shares issued, based on their published price at date of exchange (average of £6.03 per share) Costs attributable Total... -

Page 109

... of integration costs for the restructuring of the combined Norwich Union Insurance and RAC businesses has been included in the results to 31 December 2005. (ii) Gresham Insurance Company Limited On 31 March 2005, the Group acquired 100% of the share capital of Gresham Insurance Company Limited. The... -

Page 110

... Life funds by Hibernian Investment Managers Limited, part of the Group's fund management business. A further deferred cash payment of up to a10 million is payable, subject to the fulï¬lment of certain performance criteria. AIB calculate embedded value on a different basis to that used by the Group... -

Page 111

... change to the ï¬nal proï¬t on sale. The total pre-tax proï¬t on sale was £165 million (£122 million after tax) and is summarised below: 2005 £m Financial statements Net assets as at 31 December 2003 Post-tax operating proï¬t to disposal Dividends paid Foreign exchange rate movements on net... -

Page 112

...continued Aviva plc 2005 Financial statements 3 - Subsidiaries continued (ii) Other In July 2005, the Group completed the sale of the business and certain operational assets and liabilities of Hyundai Cars (UK), which was acquired as part of the RAC group, to Hyundai Motor UK Limited for a total of... -

Page 113

...-term health and accident insurance, savings, pensions and annuity business written by our life insurance subsidiaries, including managed pension fund business and our share of the other life and related business written in our associates and joint ventures, as well as the equity release business... -

Page 114

... information continued (ii) Segmental results - business segments Long-term business £m Fund management £m General insurance and health £m Other £m Total £m For the year ended 31 December 2005 Gross written premiums Premiums ceded to reinsurers Net written premiums Change in unearned premium... -

Page 115

... of acquired value of in-force business Amortisation and impairment of intangibles Short-term ï¬,uctuation in return on investments backing general insurance and health business (Proï¬t)/loss on the disposal of subsidiaries and associates Integration costs Unallocated interest Corporate costs... -

Page 116

... continued Aviva plc 2005 Financial statements 4 - Segmental information continued Long-term business £m Fund management £m General insurance and health £m Other £m Total £m For the year ended 31 December 2004 Gross written premiums Premiums ceded to reinsurers Net written premiums Change in... -

Page 117

...ts Long-term business £m Fund management £m General insurance and health £m Other £m Total £m For the year ended 31 December 2004 Segment result before tax Finance costs on central borrowings Adjusted for the following items Impairment of goodwill Amortisation and impairment of acquired value... -

Page 118

... consolidated ï¬nancial statements continued Aviva plc 2005 Financial statements 4 - Segmental information continued Long-term business £m Fund management £m General insurance and health £m Other £m Total £m As at 31 December 2004 Goodwill Acquired value of in-force business and intangible... -

Page 119

... £m 32 Other Europe £m 23 International £m 258 Total £m Year ended 31 December 2004 Gross written premiums Premiums ceded to reinsurers Internal reinsurance revenue Net written premiums Fee and commission income Segment revenue Segment result before tax Segment assets Segment liabilities... -

Page 120

... statements 4 - Segmental information continued (iii) Life and pensions and investment sales - new business and total income For the purpose of recording life and pensions new business premiums, the Group's policy is to include life insurance, long-term health and accident insurance, savings... -

Page 121

... income Note 2005 £m 2004 £m Gross written premiums Long-term: Insurance contracts Participating investment contracts General insurance and health Less: premiums ceded to reinsurers Gross change in provision for unearned premiums Reinsurers' share of change in provision for unearned premiums Net... -

Page 122

... Notes to the consolidated ï¬nancial statements continued Aviva plc 2005 Financial statements 6 - Details of expenses Note 2005 £m 2004 £m Claims and beneï¬ts paid Claims and beneï¬ts paid to policyholders on long-term business Insurance contracts Participating investment contracts Non... -

Page 123

...£m 2004 £m Other operating expenses Staff costs and other employee-related expenditure Global ï¬nance transformation programme Other corporate costs Depreciation Impairment losses on property and equipment Impairment of goodwill on subsidiaries Amortisation of acquired value of in-force business... -

Page 124

... to long-term business. On grounds of materiality, their effective interest rate has not been calculated. 8 - Longer term investment return (a) The longer-term investment return, net of expenses, attributable to the general insurance and health business result was £1,046 million (2004: £988... -

Page 125

... tax to changes in the longer term rates of return: Movement in investment return for By Change in 2005 £m 2004 £m Equities Properties 1% higher/lower 1% higher/lower Group operating proï¬t Group operating proï¬t 29 4 25 3 Financial statements 9 - Employee information The average number... -

Page 126

... differences Changes in tax rates or tax laws Write down of deferred tax assets Total deferred tax Total tax charged to income statement (note 12c) 799 (212) 587 881 (5) 89 965 1,552 475 (92) 383 272 (1) - 271 654 (ii) The Group, as a proxy for policyholders in the UK, Ireland and Australia, is... -

Page 127

... tax on the Group's proï¬t before tax differs from the theoretical amount that would arise using the tax rate of the home country of the Company as follows: 2005 £m 2004 £m Proï¬t before tax Tax calculated at standard UK corporation tax rate of 30% (2004: 30%) Different basis of tax for UK life... -

Page 128

... impairment of acquired additional value of in-force business (note 16 & 18) - Amortisation and net impairment of intangibles (note 16) - Financial Services Compensation Scheme and other levies - Short-term ï¬,uctuation in return on investments backing general insurance and health business (note 8b... -

Page 129

... as an appropriation of retained proï¬ts and, accordingly, it is accounted for when paid. Tax relief is obtained at a rate of 30%. Irish shareholders who are due to be paid a dividend denominated in euros will receive a payment at the exchange rate prevailing on 1 March 2006. Financial statements -

Page 130

.... Spain United Kingdom (Long-term business) (General insurance and health) 2005 £m 2004 £m 2005 £m 2004 £m RAC (non-insurance operations) 2005 £m 2004 £m 2005 £m Other 2004 £m 2005 £m Total 2004 £m Carrying amount of goodwill Carrying amount of intangibles with indeï¬nite useful lives... -

Page 131

... the European Embedded Value (EEV) principles. The embedded value is the total of the net worth of the life business and the value of the in-force business. The underlying methodology and assumptions have been reviewed by a ï¬rm of actuarial consultants and by the Group's auditors; - New business... -

Page 132

... consolidated ï¬nancial statements continued Aviva plc 2005 Financial statements 16 - Acquired value of in-force business (AVIF) and intangible assets AVIF £m Intangible assets £m Total £m Gross amount At 1 January 2004 Additions Acquisition of subsidiaries Foreign exchange rate movements At... -

Page 133

...the UK and certain European long-term business policyholder funds have invested in a number of property limited partnerships (PLPs), either directly or via property unit trusts (PUTs), through a mix of capital and loans. The PLPs are managed by general partners (GPs), in which the long-term business... -

Page 134

... continued (c) Other The Group also has a 50% holding in AVIVA-COFCO Life Insurance Company Limited, a life assurance company incorporated and operating in China. These shares are held by the Company, with a share of net assets of £10 million (2004: £14 million) and a fair value of £22 million... -

Page 135

... Company Type of business Class of share Proportion held Country of incorporation and operation Aviva Life Insurance Company India Pvt. Limited ProCapital S.A. RBSG Collective Investments Limited RBS Life Investments Limited The British Aviation Insurance Company Limited Insurance Online brokerage... -

Page 136

...assets £m Total £m Cost or valuation At 1 January 2004 Additions Capitalised expenditure on existing assets Acquisitions of subsidiaries Disposal of subsidiaries Disposals Transfers to investment property Fair value gains (see note 32) Foreign exchange rate movements At 31 December 2004 Additions... -

Page 137

... external valuers or by local qualiï¬ed staff of the Group in overseas operations, all with recent relevant experience. Values are calculated using a discounted cash ï¬,ow approach and are based on current rental income plus anticipated uplifts at the next rent review, assuming no future growth in... -

Page 138

.... Details of the relevant transactions are as follows: (a) United Kingdom In a United Kingdom long-term business subsidiary (NUER), the beneï¬cial interest in certain portfolios of lifetime mortgages has been transferred to ï¬ve special purpose securitisation companies, Equity Release Funding... -

Page 139

...companies in the Aviva Group. 23 - Financial investments (a) Financial investments comprise: 2005 At fair value through proï¬t or loss Trading £m Other than trading £m Available for sale* £m Total £m Debt securities UK government Non-UK government Corporate - UK Corporate - Non-UK Other Equity... -

Page 140

... Aviva plc 2005 Financial statements 23 - Financial investments continued 2004 At fair value through proï¬t or loss Trading £m Other than trading £m Available for sale* £m Total £m Debt securities UK Government Non - UK government Corporate - UK Corporate - Non-UK Other Equity securities... -

Page 141

... 2004 Cost/ amortised cost £m Unrealised gains £m Unrealised losses £m Fair value £m Debt securities Equity securities Other investments Unit trusts Derivative ï¬nancial instruments Deposits with credit institutions Specialised investment companies Minority holdings in property management... -

Page 142

...base. No further credit risk provision is therefore required in excess of the normal provision for doubtful receivables. 25 - Deferred acquisition costs and other assets (a) The carrying amount comprises: Long-term business £m General insurance and health £m Total 2005 £m Total 2004 £m Deferred... -

Page 143

...(b) During 2005, a total of 113,308,488 ordinary shares of 25 pence each were allotted and issued by the Company as follows: Number of shares Share capital £m Share premium £m At 1 January Shares issued under the Group's employee and executive share option schemes Shares issued in connection with... -

Page 144

.... (iii) Deferred bonus plan options These are options granted in 1999 and 2000 under the CGU Deferred Bonus Plan. Participants who deferred their annual cash bonus in exchange for an award of shares of equal value also received a matching award over an equal number of share options. The exercise of... -

Page 145

...26 March 2007 Number of shares 24 March 2008 Vesting date 13,462 31 December 2006 The vesting of awards under the Aviva Long-Term Incentive Plan is subject to the attainment of performance conditions as described in the Directors' remuneration report on page 67. Shares which do not vest, lapse. -

Page 146

.... (i) Share options The fair value of the options was estimated on the date of grant, based on the following weighted average assumptions: Weighted average assumption 2005 2004 Share price Exercise price Expected volatility Expected life Expected dividend yield Risk free interest rate 618p 538p... -

Page 147

.... The risk-free interest rate was based on the yields available of UK government bonds as at the date of grant. The bonds chosen were those with a similar remaining term to the expected life of the options. 29 - Shares held by employee trusts Movements in the cost of shares held by employee trusts... -

Page 148

... right to choose whether or not to pay any dividend on the new shares, and any such dividend payment will be non-cumulative. The Company has the option to defer coupon payments on the DCIs on any relevant payment date. Deferred coupons shall be satisï¬ed only in the following circumstances, all of... -

Page 149

... disposals Reserves credit for equity compensation plans (note 28d) Foreign exchange rate movements Aggregate tax effect - shareholder tax Balance at 31 December 2004 Arising in the year: Fair value gains/(losses) Fair value (gains)/losses transferred to proï¬t Share of fair value changes in joint... -

Page 150

... £m Long-term business £m General insurance and health £m 2004 Total £m Total £m Long-term business provisions Participating Unit-linked non-participating Other non-participating Outstanding claims provisions Provision for claims incurred but not reported Provision for unearned premiums... -

Page 151

... (i) Business description The Group underwrites long-term business in a number of countries as follows: - In the United Kingdom mainly in • "with-proï¬t" funds of CGNU Life Assurance, Commercial Union Life Assurance, and the With Proï¬t and Provident Mutual funds of Norwich Union Life & Pensions... -

Page 152

...-up rates of guaranteed annuity options are assumed to increase. The principal assumptions underlying the cost of future policy related liabilities are as follows: Future investment return A "risk-free" rate equal to the spot yield on gilts, plus a margin of 0.1% is used. The rates vary, according... -

Page 153

... the yields for equities and properties with reference to a margin over long-term interest rates or by making an explicit deduction from the yields on corporate bonds, mortgages and deposits, based on historical default experience of each asset class. A further margin for risk is then deducted... -

Page 154

...and deferred annuities before vesting General annuity business after vesting Pensions business after vesting Annuities in payment General annuity business Pensions business (b) France The majority of provisions arise from a single premium savings product and are based on the accumulated fund value... -

Page 155

... yet reported and associated LAE. Outstanding claims provisions are based on undiscounted estimates of future claim payments, except for the following classes of business for which discounted provisions are held: Rate Country Class 2005 2004 Mean term of liabilities 2005 2004 Financial statements... -

Page 156

... to maintain strong reserves, the Group transfers much of this release to current accident year (2005) reserves where the development of claims is less mature and there is much greater uncertainty attaching to the ultimate cost of claims. The release from prior accident year reserves during 2005 is... -

Page 157

155 Aviva plc 2005 35 - Insurance liabilities continued Before the effect of reinsurance, the loss development table is: Accident Year All prior years £m 2001 £m 2002 £m 2003 £m 2004 £m 2005 £m Total £m Gross cumulative claim payments At end of accident year One year later Two years later ... -

Page 158

... Reinsurance assets £m 2004 Net £m Long-term business provisions Long-term insurance contracts Participating investment contracts Non-participating investment contracts Outstanding claims provisions Provisions for claims incurred but not reported Provision for unearned premiums Provision arising... -

Page 159

... insurance and health 5,878 183 (128) 257 (1,178) 159 177 (530) - (78) - (564) 4,706 4,285 397 (109) 175 140 70 145 818 313 32 417 13 5,878 2005 £m 2004 £m Carrying amount at 1 January Impact of changes in assumptions Reinsurers' share of claim losses and expenses incurred in current year... -

Page 160

...participating contracts at fair value Non-participating contracts at amortised cost Total 47,258 29,304 747 30,051 77,309 43,974 24,903 678 25,581 69,555 (b) Long-term business investment liabilities Investment contracts are those that do not transfer signiï¬cant insurance risk from the contract... -

Page 161

..., various Group companies have given guarantees and options, including investment return guarantees, in respect of certain long-term insurance and fund management products. (a) UK Life with-proï¬ts business In the UK, life insurers are required to comply with the FSA's realistic reporting regime... -

Page 162

... For non-AFER business, the accounting income return exceeded guaranteed bonus rates in 2005. Guaranteed death and maturity beneï¬ts In France, the Group has also sold unit-linked policies where the death and/or maturity beneï¬t is guaranteed to be at least equal to the premiums paid. The reserve... -

Page 163

...UK, have been sold in Ireland. These guarantees are currently out-of-the-money by £84 million (2004: £79 million). This has been calculated on a deterministic basis as the excess of the current policy surrender value over the discounted value (excluding terminal bonus) of the guarantees. The value... -

Page 164

... General insurance and health business Change in loss ratio assumptions Change in expense ratio assumptions Total (1,078) (12) 3 25 (39) (3) (11) (6) (2) 2 4 (1,117) The impact of interest rates for long-term business relates primarily to the UK and the Netherlands. This results from the use of... -

Page 165

...Carrying amounts 2005 £m 2004 £m Deï¬cits in the staff pension schemes (note 42) Other obligations to staff pension schemes - insurance policies issued by Group companies (note 35a) Total IAS 19 obligations to staff pension schemes Restructuring provisions Other provisions Total 1,471 875 2,346... -

Page 166

... 2005 were 29% of employees' pensionable salaries together with the cost of redundancies during the year and an additional payment of £51 million. As this section of the scheme is closed to new entrants and the contribution rate is determined using the projected unit method, it is expected that... -

Page 167

... 2004 2005 Ireland 2004 Date of most recent actuarial valuation The main ï¬nancial assumptions used to calculate scheme liabilities under IAS 19 are: Inï¬,ation rate General salary increases Pension increases Deferred pension increases Discount rate *Age-related scale increases plus 1.4% (2004... -

Page 168

...schemes comprises: 2005 £m Total 2004 £m Current service cost Past service (credit)/cost Gain/(loss) on curtailments Charge to net operating expenses Expected return on scheme assets Interest charge on scheme liabilities Credit to investment income Total charge to income Expected return on scheme... -

Page 169

167 Aviva plc 2005 42 - Pension obligations continued Plan assets include investments in Group-managed funds in the consolidated balance sheet of £578 million (2004: £2,405 million) in the UK scheme, and insurance policies of £143 million and £732 million (2004: £117 million and £696 million)... -

Page 170

...subordinated notes Debenture loans 9.5% guaranteed bonds 2016 2.5% subordinated perpetual loan notes Other loans Amounts owed to credit institutions Bank loans Commercial paper Total commercial paper Securitised mortgage loan notes UK lifetime mortgage business Dutch domestic mortgage business Total... -

Page 171

... guaranteed bonds 2016 £ 8.625% guaranteed bonds 2005 £ 2.5% subordinated perpetual loan notes a Other loans Various Amounts owed to credit institutions Bank loans Commercial paper Commercial paper Securitised mortgage loan notes UK lifetime mortgage business Dutch domestic mortgage business Total... -

Page 172

...In September 2004, one of the Group's UK long-term business subsidiaries, Norwich Union Life & Pensions Limited (NULAP), entered into a securitisation arrangement with The Royal Bank of Scotland Group plc (RBS), to provide funding to cover initial new business acquisition and administration costs in... -

Page 173

...stock repurchase arrangements entered into in the United Kingdom and the Netherlands. 45 - Other liabilities 2005 £m 2004 £m Deferred income Reinsurers' share of deferred acquisition costs Accruals Other liabilities Less: Amounts classiï¬ed as held for sale Expected to be settled within one year... -

Page 174

... on long-term savings products Note 38 gives details of guarantees and options given by various Group companies as a normal part of their operating activities, in respect of certain long-term insurance and fund management products. In the United Kingdom, in common with other pension and life policy... -

Page 175

... In addition, in line with standard business practice, various Group companies have been given guarantees, indemnities and warranties in connection with disposals in recent years of subsidiaries and associates to parties outside the Aviva Group. In the opinion of the directors, no material loss will... -

Page 176

... Aviva plc 2005 Financial statements 48 - Cash ï¬,ow statement (a) The reconciliation of proï¬t/(loss) before tax to the net cash inï¬,ow from operating activities is: 2005 £m 2004 £m Proï¬t before tax Adjustments for: Share of (proï¬ts) losses of joint ventures and associates Dividends... -

Page 177

...327 (19) 308 2005 £m 2004 £m Cash at bank and in hand Cash equivalents Bank overdrafts 3,530 10,227 13,757 (690) 13,067 1,631 11,148 12,779 (653) 12,126 Of the total cash and cash equivalents shown above, £25 million has been classiï¬ed as held for sale (see note 3c). Financial statements -

Page 178

... capital to meet risks and regulatory requirements. The capital statement also provides a reconciliation of shareholders' funds to regulatory capital. The analysis below sets out the Group's available capital resources. Available capital resources CGNU withproï¬t fund £m CULAC NUL&P Total UK life... -

Page 179

... meet risks and regulatory requirements set by reference to local guidance and EU directives. After effecting the year-end transfer to shareholders', the UK with-proï¬t funds' available capital of £5.2 billion (2004: £4.5 billion) can only be used to provide support for UK with-proï¬ts business... -

Page 180

... requirements of the fund. Any transfer of the surplus may give rise to a tax charge subject to availability of tax relief elsewhere in the Group. (v) Overseas life operations - the capital requirements and corresponding regulatory capital held by overseas businesses are calculated using the locally... -

Page 181

..., and other management reporting. 2. Risk management The Group has developed a life insurance risk policy and guidelines on the practical application of this policy. Individual life insurance risks are managed at a business unit level. The Life Insurance Risk committee monitors the risk framework... -

Page 182

... business units. Examples of each type of embedded derivative affecting the Group are: Options: call, put, surrender and maturity options, guaranteed annuity options, option to cease premium payment, options for withdrawals free of market value adjustment, annuity option, guaranteed insurability... -

Page 183

... the Group as a whole, is exposed to, quantifying their impact and calculating appropriate capital requirements. Increasingly risk-based capital models are being used to support the quantiï¬cation of risk under the ICA framework. All general insurance business units undertake a quarterly review of... -

Page 184

..., long-term debt and ï¬xed income securities are exposed to ï¬,uctuations in interest rates. Exposure to interest rate risk is monitored through several measures that include Value-at-Risk analysis, position limits, scenario testing, stress testing and asset and liability matching using measures... -

Page 185

.... Interest rate risk Interest rate risk arises primarily from the Group's investments, long-term debt and ï¬xed income securities. Interest rate risk also exists in policies that carry investment guarantees on early surrender or at maturity, where claim values can become higher than the value of... -

Page 186

...indirect impact from changes in the value of equities held in policyholders funds from which management charges or a share of performance are taken and from its interest in the free estate of long-term funds. At business unit level, equity price risk is actively managed through the use of derivative... -

Page 187

...information security, human resources, project management, outsourcing, tax, legal, fraud and compliance risks. Financial statements In accordance with Group policies, business unit management has primary responsibility for the effective identiï¬cation, management, monitoring and reporting of risks... -

Page 188

... connection with the in-force policies for each business unit. Assumptions are best estimates based on historic and expected experience of the business. A number of the key assumptions for the Group's central scenario are disclosed elsewhere in these statements. General insurance and health business... -

Page 189

...selling investments, changing investment portfolio allocation, adjusting bonuses credited to policyholders, and taking other protective action. A number of the business units use passive assumptions to calculate their long-term business liabilities. Consequently, the actual impact of a change in the... -

Page 190

... statements 51 - Derivative ï¬nancial instruments The Group uses cash ï¬,ow, fair value and net investment hedges to mitigate risk, as detailed below. (a) Cash ï¬,ow hedges As explained in note 3(b), the Group hedged the foreign exchange risk that it expected to assume as a result of the sale... -

Page 191

...total Group assets under management are: 2005 £m 2004 £m Total assets included in the consolidated balance sheet Additional value of internally-generated in-force long-term business Third party funds under management Unit trusts, OEICs, Peps and Isas Segregated funds Total assets under management... -

Page 192

... continued Financial statements of the Company Income statement For the year ended 31 December 2005 Aviva plc 2005 Financial statements Where applicable, the accounting policies of the Company are the same as those of the Group on pages 78 to 86. The notes (identiï¬ed alphabetically on pages... -

Page 193

... tax assets Current assets Loans owed by subsidiaries Other assets Cash and cash equivalents Total assets Equity Ordinary share capital Preference share capital Called up capital Share premium account Merger reserve Investment valuation reserve Equity compensation reserve Retained earnings Direct... -

Page 194

... in the Group ï¬nancial statements, reference is made to the notes (identiï¬ed numerically) on pages 93 to 189. Note 2005 £m 2004 £m Fair value gains on investments in subsidiaries Aggregate tax effect Reserves credit for equity compensation plans Net income recognised directly in equity Pro... -

Page 195

... items pass through the Company's own bank accounts. 2005 £m 2004 £m Cash ï¬,ows from ï¬nancing activities Funding provided by subsidiaries Net drawdown/(repayment) of borrowings Preference dividends paid Ordinary dividends paid Interest paid on borrowings Net cash (used in) / from ï¬nancing... -

Page 196

... 31 December 2004 £m Equity as reported under UK GAAP Adjusted for: Dividend recognition (see (1) below) Revaluation of investments in subsidiaries (see (2) below) Pensions (see (3) below) Equity compensation plans (see (4) below) Direct Capital Instrument interest Other items Deferred tax impact... -

Page 197

... 2004 £m Financial statements Staff costs and other employee-related expenditure Other operating costs Net foreign exchange (gains)/losses 62 120 (22) 160 55 84 29 168 (ii) Pension costs The Company is one of a number of UK companies being charged for its employees participating in the Aviva... -

Page 198

...) before tax Tax calculated at standard UK corporation tax rate of 30% (2004: 30%) Adjustment to tax charge in respect of prior years Non-assessable dividends Disallowable expenses Disallowed deferred tax asset Other Total tax credited/(charged) to income statement (iii) The net deferred tax asset... -

Page 199

... at 31 December 2004 Arising in the year: Proï¬t for the year Fair value gains on investments in subsidiaries Dividends and appropriations Reserves credit for equity compensation plans Shares issued in lieu of dividends Shares issued on acquisition of subsidiary Aggregate tax effect Other movements... -

Page 200

... parties' payables are not secured and no guarantees were received in respect thereof. The payables will be settled in accordance with normal credit terms. The directors and key management of the Company are considered to be the same as for the Group. Information on both the Company and Group key... -

Page 201

... and auditors The directors are responsible for preparing the alternative method of reporting long-term business on the above European Embedded Value basis. Our responsibilities, as independent auditors, in relation to the alternative method of reporting long-term business are established in the UK... -

Page 202

...of acquired value of in-force business and intangibles Financial Services Compensation Scheme and other levies Variation from longer-term investment return Effect of economic assumption changes Proï¬t on the disposal of subsidiaries and associates Integration costs Exceptional costs for termination... -

Page 203

... £m 2004 £m Fair value gains, on AFS securities and owner-occupied properties, net of transfers to the income statement Actuarial losses on pension schemes Foreign exchange rate movements Equity Compensation Reserve charge for the period Aggregate tax effect - shareholder tax Net (expense)/income... -

Page 204

... Aviva plc Preference share capital and direct capital instrument Minority interests Total equity Liabilities Gross insurance liabilities Gross liability for investment contracts Unallocated divisible surplus Net asset value attributable to unitholders Provisions Deferred tax liabilities Current tax... -

Page 205

... pension fund deï¬cit to long-term business3 Long-term business net assets on an EEV basis 15,598 15,113 217 631 (363) 15,598 13,826 13,014 217 595 - 13,826 3. The value of the Aviva Pension Scheme deï¬cit has been notionally allocated between segments, based on current funding and the UK Life... -

Page 206

... Report and Accounts on page 199 of this document. Covered business The EEV calculations cover the following lines of business: life insurance, long-term health and accident insurance, savings, pensions and annuity business written by our life insurance subsidiaries, including managed pension fund... -

Page 207

...returns on certain asset classes (eg. equities) are not achieved. Risk discount rates for our life businesses have been calculated using a risk margin based upon a Group Weighted Average Cost of Capital (WACC). The Group WACC is calculated using a gross risk free interest rate, an equity risk margin... -

Page 208

... for via the updated risk margin calculation. Participating business Future regular bonuses on participating business are projected in a manner consistent with current bonus rates and expected future returns on assets deemed to back the policies. For with-proï¬t funds in the UK and Ireland, for the... -

Page 209

...capital, calculated on the same basis as for in-force covered business. New business sales are expressed on two bases: annual premium equivalent (APE) and the present value of future new business premiums (PVNBP). The PVNBP calculation is equal to total single premium sales received in the year plus... -

Page 210

... capital, tax and minority interest Annual premium equivalent 2005 £m 2004 £m Present value of new business premiums 2005 £m 2004 £m New business contribution1 2005 £m 2004 £m New business margin2 2005 % 2004 % Analysed between: - Bancassurance channels - Other distribution channels Total... -

Page 211

... the movement in embedded value for the life and related businesses for 2005 and 2004. The analysis is shown separately for net worth and the value of in-force covered business, and includes amounts transferred between these categories. The transfer from life and related businesses to other segments... -

Page 212

...method of reporting long-term business continued Aviva plc 2005 Financial statements Analysis of movement in life and related businesses embedded value continued All ï¬gures are shown net of tax. 2005 Net worth £m Value of in-force £m Total £m Embedded value at the beginning of the year - Free... -

Page 213

...for further tax beneï¬ts arising from dividends from subsidiaries. In the Netherlands, they reï¬,ect a variety of changes including increased annual management fees on unit-linked contracts, favourable change in asset mix, and the reduction of future guaranteed returns on group pensions business in... -

Page 214

... method of reporting long-term business continued Aviva plc 2005 Financial statements Segmental analysis of the components of life EEV operating return Year ended 31 December 2004 UK £m France £m Ireland £m Italy £m Netherlands £m Poland £m Spain £m Other Europe £m International £m Total... -

Page 215

... 2005 Segmental analysis of life and related businesses embedded value Net worth Required capital1 £m Free surplus £m Value of in-force covered business Present value of in-force £m Cost of required capital £m Total 31 December 2005 Embedded value £m United Kingdom Continental Europe France... -

Page 216

214 Financial statements continued Alternative method of reporting long-term business continued Aviva plc 2005 Financial statements Time value of options and guarantees The following table sets out the time value of options and guarantees relating to covered business by territory at 31 December ... -

Page 217

... risk free yields in the UK, the Eurozone and other territories. The principal economic assumptions used are as follows: UK 2005 2004 2003 2005 2004 France 2003 Risk discount rate Pre-tax investment returns: Base government ï¬xed interest Ordinary shares Property Future expense inï¬,ation Tax rate... -

Page 218

... and Aviva's medium-term bonus plans. The distribution of proï¬t between policyholders and shareholders within the with-proï¬t funds assumes that the shareholder interest in conventional with-proï¬t business in the UK and Ireland continues at the current rate of one ninth of the cost of bonus... -

Page 219

.... The total annual return on equities is calculated as the return on one-year bonds plus an excess return. The excess return is assumed to have a lognormal distribution. The model also generates property total returns and real yield curves, although these are not signiï¬cant asset classes for Aviva... -

Page 220

... unchanged except where they are directly affected by the revised economic conditions. For example, future bonus rates are automatically adjusted to reï¬,ect sensitivity changes to future investment returns. Embedded value (net of tax) 31 December 2005 As reported on page 213 £m 1% increase in... -

Page 221

... will only impact the value of the in-force covered business, whereas a 10% movement in equity/property values may impact both the net worth and the value of in-force, depending on the allocation of assets. New business contribution before required capital (gross of tax) 2005 As reported on page 207... -

Page 222

... continued Alternative method of reporting long-term business continued Aviva plc 2005 Financial statements Sensitivity analysis - economic assumptions continued New business contribution before required capital (gross of tax) 2005 As reported on page 207 £m 1% increase in equity/ property returns... -

Page 223

... changing non-economic assumptions. In each sensitivity calculation, all other assumptions remain unchanged. Embedded value (net of tax) 31 December 2005 As reported on page 213 £m 10% decrease in maintenance expenses £m 10%/5% 10% decrease in decrease in in mortality/ lapse rates morbidity rates... -

Page 224

..., and transact insurance or Hibernian Investment Managers Limited reinsurance business, fund management or services in connection therewith, Hibernian Life & Pensions Limited unless otherwise stated. RAC School of Motoring Ltd United Kingdom Italy BSM Group plc Aviva Italia Holding SpA and its... -

Page 225

... Private shareholders who currently receive dividends paid directly into their bank or building society account receive one consolidated tax voucher each year instead of a voucher with each dividend payment, unless they inform the Registrar otherwise. Scrip dividend The Aviva Scrip Dividend Scheme... -

Page 226

... ï¬rst quarter long-term savings new business ï¬gures Annual General Meeting Announcement of unaudited six months' interim results Announcement of third quarter long-term savings new business ï¬gures Ordinary Shares Ex-dividend date Record date Scrip dividend price available Dividend payment date... -

Page 227

... each other. Aviva Group UK long-term savings and general insurance Fund management Aviva worldwide internet sites * All 0870 numbers are charged at national rates, and are only available if you are calling from the UK. **To check instructions and maintain high quality service standards, Barclays... -

Page 228

Aviva plc St Helen's, 1 Undershaft London EC3P 3DQ Telephone +44 (0)20 7283 2000 www.aviva.com Registered in England Number 2468686