American Express 2004 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2004 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

|

|

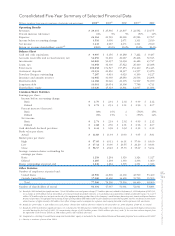

The weighted average assumptions used to determine

net periodic benefit cost were:

2004 2003 2002

Discount rates 5.7% 6.2% 7.0%

Rates of increase in

compensation levels 4.0% 4.0% 4.2%

Expected long-term rates

of return on assets 7.9% 8.1% 9.3%

For 2004, the Company assumed on a weighted aver-

age basis a long-term rate of return on assets of 7.9%.

In developing the 7.9% expected long-term rate

assumption, management evaluated input from an

external consulting firm, including their projection of

asset class return expectations and long-term inflation

assumptions. The Company also considered the his-

torical returns on the plan assets.

The asset allocation for the Company’s pension plans at

September 30, 2004 and 2003, and the target allocation

for 2005, by asset category, are below. Actual alloca-

tions will generally be within 5 percent of these targets.

Target

Allocation

Percentage of

Plan assets at

2005 2004 2003

Equity securities 68% 68% 66%

Debt securities 26% 27% 26%

Other 6% 5% 8%

Total 100% 100% 100%

The Company invests in an aggregate diversified

portfolio to ensure that adverse or unexpected results

from a security class will not have a detrimental impact

on the entire portfolio. The portfolio is diversified by

asset type, performance and risk characteristics and

number of investments. Asset classes and ranges con-

sidered appropriate for investment of the plans assets

are determined by each plan’s investment committee.

The asset classes typically include domestic and for-

eign equities, emerging market equities, domestic and

foreign investment grade and high-yield bonds and

domestic real estate.

The Company’s retirement plans expect to make ben-

efit payments to retirees as follows (millions): 2005,

$132; 2006, $141; 2007, $150; 2008, $160; 2009, $171;

and 2010 – 2014, $1,013. In addition, the Company

expects to contribute $59 million to its pension plans

in 2005.

Defined Contribution Retirement Plans

The Company sponsors defined contribution retire-

ment plans, the principal plan being the Incentive Sav-

ings Plan, a 401(k) savings plan with a profit sharing

and stock bonus plan feature which covers most

employees in the United States. See Note 15 for further

discussion of this feature. The defined contribution

plan expense was $161 million, $145 million and $131

million in 2004, 2003 and 2002, respectively.

Other Postretirement Benefits

The Company sponsors defined postretirement benefit

plans that provide health care and life insurance to cer-

tain retired U.S. employees. Net periodic postretire-

ment benefit expenses were $38 million, $42 million

and $38 million in 2004, 2003 and 2002, respectively.

Effective January 1, 2004, the Company decided to no

longer provide a subsidy for these benefits for employ-

ees who were not at least age 40 with at least 5 years

of service as of that date. See Note 1 for a discussion

of the Company’s election to early adopt FSP FAS 106-2.

The recognized liabilities for the Company’s defined

postretirement benefit plans are as follows:

RECONCILIATION OF ACCRUED BENEFIT COST AND TOTAL

AMOUNT RECOGNIZED

(Millions) 2004 2003

Funded status of the plan $ (397) $ (428)

Unrecognized prior service cost (13) (22)

Unrecognized actuarial loss 162 206

Fourth quarter payments 810

Net amount recognized $ (240) $ (234)

Accumulated benefit obligation

at period end $ (397) $ (428)

Weighted average assumptions to determine benefit

obligations:

2004 2003

Discount rates 5.75% 6%

Health care cost increase rate:

Following year 10.5% 11%

Decreasing to the year 2016 5% 5%

AXP

AR.04

114

Notes to Consolidated Financial Statements